A royal storm

A letter by Professor Kenrick Hunte appearing in the press earlier this week generated a wave of conversation across the society. Essentially, the Professor claimed that Guyana has been receiving Royalty of about a quarter of the 2% to which it is entitled under the 2016 Petroleum Agreement. Rather unusually, Mr. Elson Low of the PNC -R, Dominic Gaskin, former member of the Coalition Cabinet f the AFC and Vice President Jagdeo found common ground in rejecting Hunte. Low grounded his view on official pronouncements from the Ministry of Finance and Bank of Guyana reports, claiming that the number of lifts – the division point for sharing profit oil – being commensurate with a 2% royalty and not 0.5%. Gaskin, who was one of Granger’s Quintet + 1 on oil and gas, was positive that “there’s a perfectly logical explanation for these seemingly contradictory figures”, referring to Hunte’s and the Government’s.

The Vice President was even more expansive. His words are too precious and ordained to invite reported speech, or a summary. This is how he rebutted Hunte. “Royalty is calculated on production minus, so total crude production minus the crude used in the operations for transport and on the FPSOs (Floating Production Storage and Offloading vessels). In Guyana’s case, the FPSOs are operated by gas, so there is no deduction whatsoever, so royalty is calculated on the basis of total production and total sales. There is no deduction whatsoever. Every month, they have to confirm what the average price would be, the weighted average, and the [government] gives approval for that”.

Clearly, he does not know what the government does, if anything in relation to royalty, or indeed to anything else.

It does not appear that the VP has ever bothered to read the 2016 Agreement, let alone its reference to the Petroleum Exploration and Production Act and its definition of “petroleum”. In fact, the very first item in the definition of “petroleum” is this: “any naturally occurring hydrocarbons, whether in a gaseous liquid or solid-state”. Does the country’s petroleum czar not know that billions are charged to operations annually for supplies to the oil companies by at least one oil distributor? His answer was not only completely wrong, but shockingly misinformed, misleading and a total misrepresentation of reality. If this is Jagdeo’s knowledge of the petroleum sector, then President Ali has to step in, lest things get worse than they are.

Now back to Hunte.

His professorial approach with its mathematical formula involving Sugar and Timber Exports and a mystique of equations was probably beyond the level of quite a few Guyanese and may have led to the sensationalizing in some quarters. I took a different route and did find numbers that require real explanations, in the absence of which Hunte’s findings rather than his methodology have to be taken seriously. Here is what the Agreement prescribes about “royalties”.

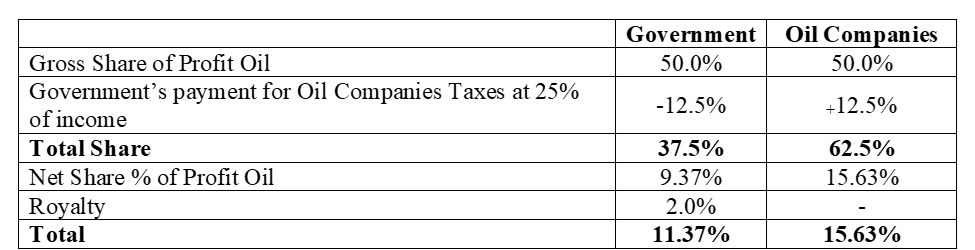

‘The Contractor shall pay, at the Government’s election either in cash based on the value of the relevant Petroleum as calculated pursuant to Article 13 or in kind, a royalty of two percent (2%) of all Petroleum produced and sold, less the quantities of Petroleum used for fuel or transportation in Petroleum Operations, from all production licenses subject to this Agreement.”

Even the most diligent journalist or forensic investigator cannot compute the royalty payable to Government in the absence of the cost of Petroleum used for fuel or transportation in Petroleum Operations. There is no real solace in the fact that the effect on royalty is 2% of that total. The other problem is that we will not know the value of petroleum sold by Exxon, Hess and CNOOC until their 2023 numbers are released in the form of audited financial statements within the next couple of months. To reduce the margin of error therefore, I have used just 2022 data from the financial statements of the three companies, plus the proceeds from sale of Government share of profit oil and apply to that total, a 2% for royalty.

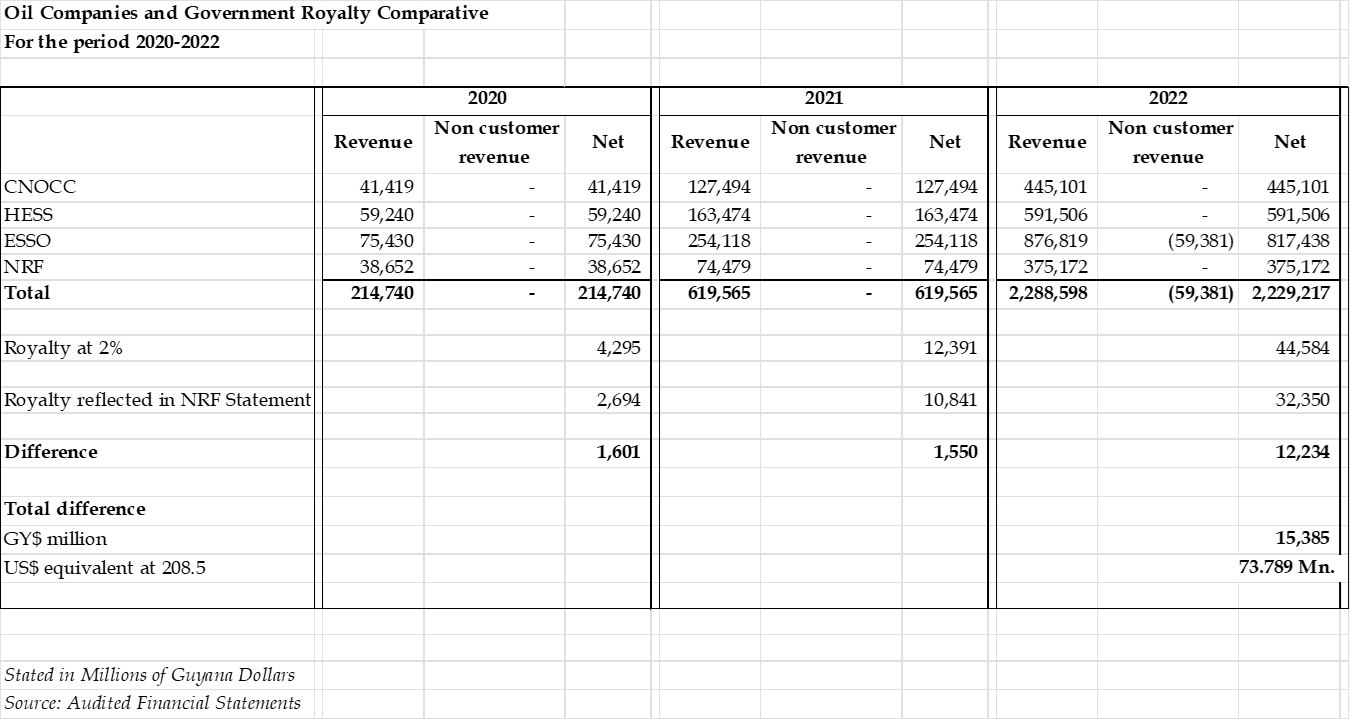

The results of that exercise are represented in the Table below showing the Oil Companies’ Revenue and Royalty due and received by the Government over the three years 2020-2022.

What is apparent is that there is indeed some US$73.8 Mn. of royalties unaccounted for and one can speculate whether this is all to do with the implausible absence of the cost of fuel used in production or transportation, or in the difference in the accounting methodology used – accrual in the case of the oil companies and cash basis in the case of the NRF. Yes, the numbers are lower than Hunte’s, but he extrapolated to the end of 2023 when production, and therefore royalty soared. His numbers ought not to be discounted or dismissed.

Conclusion

I repeat again, unless President Ali puts a Petroleum Commission in place, Guyana’s incompetence in oil and gas will continue to be exploited at the national expense. He has to act in the national interest rather than as if he is afraid of or beholden to Jagdeo. We must not forget as well that hundreds of thousands of US Dollars were spent on an audit. Did their report, which is shrouded in mystery and secrecy, touch on royalty and profit oil? Only a Petroleum Commission can save us from this tragic farce.