Natural Resource Fund overstated by $274,765 Mn., should be addressed as a matter of urgency.

Among the several challenges facing the Natural Resource Fund (NRF) – also known internationally as a Sovereign Wealth Fund – identified in column 117 published on 22 December, was one which I described simply as “accounting”. Readers will recall that in the concluding sentence I opined that the balance in the NRF is overstated by “tens of billions of Guyana dollars”. To my horror, my research discovered that the overstatement at 30. June 2023 after the payment of 2022 corporation taxes for the oil companies, was $274.8 Bn. ($274,765 Mn.), representing 76% of the Fund balance at that date. The magnitude and significance of the error is evident from the 2022 financial statements of the Fund, which received a clean, unqualified opinion by the Audit Office of Guyana, showing the value of the Fund at that date of G$298 Bn. With taxes payable amounting to $49.7 Bn for the years 2020 and 2021 to be financed out of Guyana’s share of profit oil, the correct value of the Fund at 31st. December 2022 should have been G$248.4 Bn, the difference representing an overstatement of 20%. A similar overstatement for 2023 alone, amounted to a further G$225.1 Bn., hence the cumulative overstatement of $274.8 Bn.

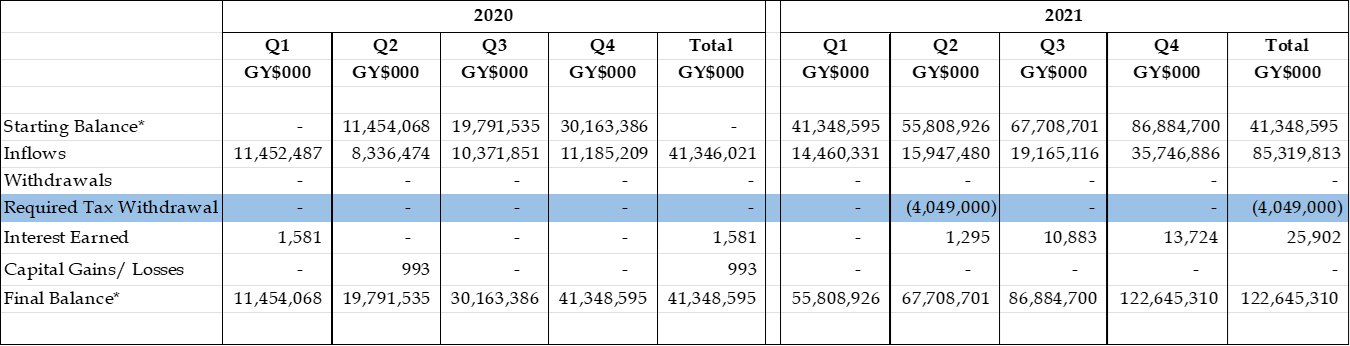

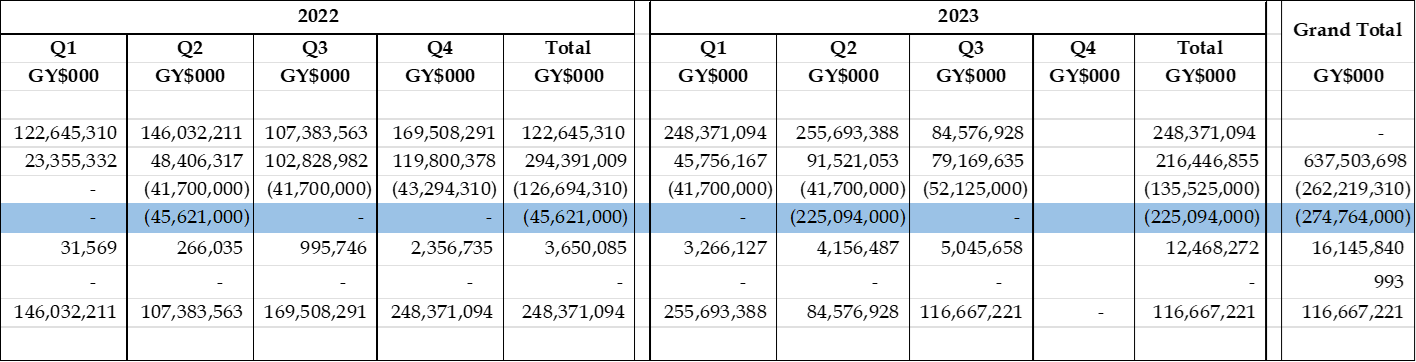

Natural Resource Fund – Summary of Quarterly Reports

Source of Information: Bank of Guyana Quarterly Reports, *described as market value. Highlighted information from companies audited financial statements.

Summary of Contractor’s Income Statement (Exxon, Hess, CNOOC)

Source of Information: Audited Financials

As astonishing as it sounds, if just one of several persons or agencies involved – the Office of the President, the Ministry of Finance, including the Budget Office, the Ministry of Natural Resources, the Bank of Guyana, the Guyana Revenue Authority (GRA), the NRF Board and, I must say, the National Assembly and the Attorney General’s Chambers – had been paying attention to and discharging their respective responsibilities, this fiasco would have not arisen in the first place. What is worse, this situation has existed since at least 2021.

Relationship between NRF and the 2016 Petroleum Agreement

Let us look briefly at the operations of the NRF and its relationship to the 2016 Petroleum Agreement. The NRF receives three sources of income: royalty of 2% of all petroleum produced and sold (less cost of fuel used in production and transportation), the proceeds from the sale of the government’s share of profit oil and any interest received on investments, mainly cash balances held by the Fund. In accounting parlance, these are credits to the Fund account. Debits would represent withdrawals from the Fund, principally for two purposes. The first being transfers to the Consolidated Fund in accordance with sections 16, 19 and 20 of the NRF Act and second, money requested by the Minister of Natural Resources to pay to the Guyana Revenue Authority the taxes payable shown on the Company’s corporation tax returns for which the GRA issues certificates of taxes paid.

NRF Balances

Produced hereunder is a summary extract from the Audited financial statements of the three contracting oil companies for the years 2020 to 2022, highlighting the amount of taxes payable by them for each of those years. Those amount in total to a staggering G$274,765 Mn. If the transactions were accounted for in accordance with the Agreement, Corporation Tax receipts for the three years should have included $4,049 Mn. for 2020, $45,621 Mn. for 2021 and $225,094 Mn. for 2022, with corresponding reductions from the Natural Resource Fund for those years.

I am not asking cynics to believe me. They just need to look at Note 7 of the audited 2022 audited financial statements of Esso Exploration and Production Guyana Limited which states as follows:

“Under Article 15.2 of the petroleum agreement, the Company is subject to the income tax laws of Guyana with respect to filing returns, assessment of tax and keeping of records. (Emphasis mine). Under article 15.4 of the Petroleum Agreement, the sum equivalent to the tax assessed on [the] Company will be paid by the Minister responsible for petroleum to the Commissioner General, Guyana Revenue Authority and is reported as non-customer revenue.”

The observant reader will note the obligations of the three companies do not include the payment of taxes, which is done on their behalf by the Government. The reference to “non-customer revenue” is to comply with Article 15.4 (a) of the Agreement. For the answer to the question of the proper source of the money to pay the Commissioner General, one has to turn to Article 15.4 (b) of the Agreement. This agreement requires the tax to be paid out of the Government’s share of profit oil, the proceeds of which, under the NRF Act, are deposited into the Natural Resource Fund.

Screaming questions

The first question to arise is whether Minister Vickram Bharrat or Vice President Bharrat Jagdeo has ever read the financial statements of the company, which interprets for them the relevant provision of the Petroleum Agreement. Steve Coll’s masterpiece Private Empire ExxonMobil and American Power shows the oil giant at its ruthless and diabolical best when dealing with host countries whose governments are clueless, incompetent, malleable and spineless. They have found both the APNU+AFC and the PPP/C governments ticking all these boxes.

Like the majority of thinking Guyanese, I have always been offended by Article 15 of the Petroleum Agreement which the Granger/Trotman duo has locked us into until 2057, give or take a couple of years. And like the majority of thinking Guyanese, I feel painfully betrayed by the Ali/Jagdeo duo who now defend as sacred and inviolable an Agreement which they committed to “review and renegotiate” as part of their 2020 elections promises.

The next question is whether any, and if so what amount, of any actual tax payments made by Minister Vickram Bharrat to the Guyana Revenue Authority on behalf of the oil companies. That is a question which calls for an investigation in the absence of proper disclosure.

What I can state with a high level of confidence is that nothing emanating from several governmental agencies suggests that the Minister of Natural Resources has paid any actual cash to the Guyana Revenue Authority for which Certificates of Taxes Paid must be issued. These agencies include: the Office of the President, which has constitutional responsibility for the natural resources sector, the Ministry of Natural Resources whose Minister is responsible for the general oversight of petroleum and the mining sector, the Ministry of Finance which has responsibility for the Budget Office and for the annual Budgets, the Bank of Guyana which operationally manages the Natural Resource Fund, the Guyana Revenue Authority which is responsible for the collection of taxes and the Natural Resource Fund Board,

It is sad but not surprising that Minister Bharrat has once again failed in a major duty in his portfolio of responsibilities for which there will be no sanction, or consequence – not even the infamous two weeks salary deduction! If the Minister was familiar with the 2016 Agreement or has been following all the concerns in the press, he would not have been guilty of this grave act of omission. The oil companies of course, would know their entitlement and the procedures to access those entitlement. In other words, they would have had their tax advisers prepare their tax returns and deliver these returns to the Guyana Revenue Authority in accordance with Article 15.5 of the Agreement. The Article is carefully crafted with language like “properly prepare the receipts” and “proper tax certificates … evidencing the payment” by the Guyana Revenue Authority.

Conclusion

It is unquestionable that tax certificates evidencing receipt should have been issued. It is clear that no payment was made from NRF, nor was any such money accounted for in the Estimates of Receipts and Payments and paid into the Consolidated Fund. This omission reflects poorly on the Budget Office. The irrefutable but uncomfortable conclusion is that no money was paid to or received by the Guyana Revenue Authority. This is obviously a matter for the statutory auditors (the Auditor General) and the relevant government agencies, including the Natural Resource Fund Board. This Board needs a better understanding of the funds at its disposal to assure citizens that it is capable of defending and protecting the legitimacy, accuracy and integrity of the Fund.

Finally, having disparaged its predecessor’s Natural Resource Fund Act # 12 of 2019, both before and during the rushed parliamentary debate on its own NRF, the Government MP’s must be hugely embarrassed that not one of them understood the implication of the 2016 Petroleum Agreement on the Natural Resource Act. As a consequence, there is a clear disconnect between the Act and the Petroleum Agreement in that section 16 of the Act dealing with withdrawals does not include the taxes paid on behalf of the oil companies. That Act must therefore be amended urgently, to preserve the so-called sanctity of the 2016 “contract”. In doing so, the draftspersons would also have to address the overstatement of the Natural Resource Fund either by way of a belated cumulative transfer, or by some other legal device. While the parliamentary opposition had walked out the debate in protest about the allocation of speaking time, it appears that it too did not recognise the omission.

The overstatement of the balance in the Natural Resource Fund at the amount and in the current improper form must be addressed and corrected. This is not a “massa cow, massa bull matter”. They fall under separate legislation and the NRF is too important an inter-generational mechanism to this country to allow it to remain tainted.

Next week’s column will expose the myth of the 50/50 Profit Share.