The Myth of the equal share – Part 1

Introduction

On the occasion of the first column for 2024, I extend best wishes to readers for an informed and productive year and realisation of the hope of a fairer contract. Readers will recall the promise made in last week’s column to address the myth of the 50:50 share of profit oil under the 2016 Petroleum Agreement. For the research minded, please see sub-article 4 of Article 11 – Cost Recovery and Production Sharing of that Agreement.

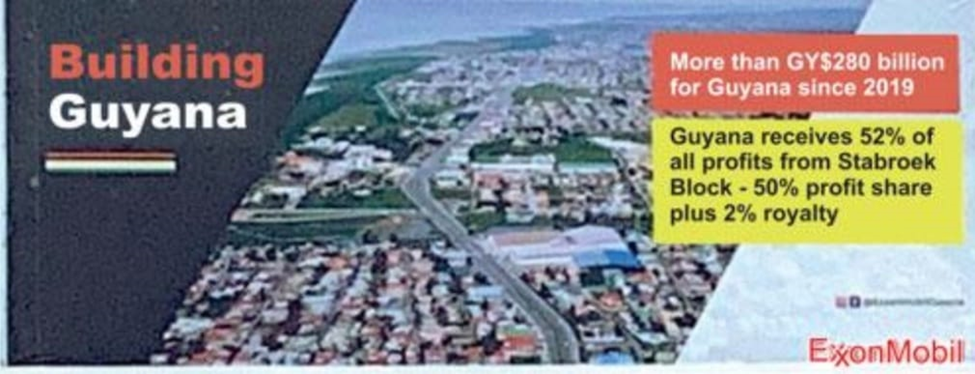

Let us begin with the billboard below sponsored by Exxon and prominently displayed at the Demerara Harbour Bridge. It states that Guyana receives 52% of all profits from Stabroek Block – 50% profit share and 2% royalty. Let us forget for a moment Exxon’s reputation for fuzzy math and creative accounting, now adding two disparate and unrelated numbers – net oil profit and gross royalty – to arrive at Guyana’s share! What the billboard does not tell us is what Exxon and its co-contractors will be receiving from the Stabroek Block.

This two-part column will explore what Exxon and partners walk away with, in profit oil and tax benefits, compared with what the Government receives as net profit oil and royalty. Exxon would not admit, let alone publicise, an account of what it and its partners receive because that would expose the mantra of equal sharing of benefits and the information in its billboard as completely false and dishonest.

Guaranteed profit share

The 2016 Agreement sets a maximum 75% limit on recoverable cost in any year, leaving 25% to be shared 12.5% to the Government and 12.5% to the oil companies as a collective. In other words, for every barrel of profit oil accruing to the Government, the oil companies should receive not a barrel each, but one barrel to be shared among the three of them. However, the structure of the Agreement severely distorts this oversimplification being sold to Guyanese. A significant proportion of the costs expended in any period financed by the oil companies to be recovered from oil revenues. Additionally, the recoverable cost for any period includes unrecovered costs from previous periods.

Let us look at an example. If recoverable cost for any period amounts to say 60%, but there are unrecovered costs from the preceding period amounting to the equivalent of say 35% of revenue, 15% of those costs are recoverable in the current period with the remaining 20% carried forward to the next period.

This may help to explain why Budget Speech 2022 could report 69 lifts from the commencement of production in 2019 to December 2021 of which Guyana received only 9 lifts, or just over one for every seven received by the oil companies. In 2022, that situation remained the same, with the Guyana receiving 13 of 102 lifts. In percentage terms, Guyana received 13.04% in 2020/2021 and 12.74% in 2022. The Minister offered no explanation for these astounding numbers. The man who knows the reasons and who keeps the hard-to-audit books is Exxon’s Alistair Routledge, but his lips are sealed when it comes to facts.

Despite all the cant about transparency and accountability, neither the Ministry of Natural Resources, the financial statements of the oil companies nor the ministerial audits have given the public a running account of unrecovered costs. The public therefore is in the dark about how much of the 75% of recoverable costs in any period is made up of unrecovered costs from earlier periods. What the public has a general idea about is that the unrecovered costs are made up of significant pre-production costs, which this writer believes were fraudulently overstated by the oil companies, the low level of production in the early years (2020 – 2021), and the absence of ringfencing. In a ring-fenced environment, the cost in a single field or on a single project is recovered much faster, allowing for higher profits.

The situation is different when there is no ringfencing since costs will always be more than they should be as income is reduced by exploration expenses incurred on some other field or project. For better or worse, and if there are no further “force majeure” extensions of the relinquishments, exploration activities will cease on the expiration of the current prospecting licence in 2027. After that point, only the balance of unrecovered costs and production expenditure will be charged to oil revenue, resulting in higher levels of profit oil. Once this point is reached, Government revenue will increase but so too will the revenue of the oil companies, together with the unlimited tax benefits they enjoy.

First level benefits

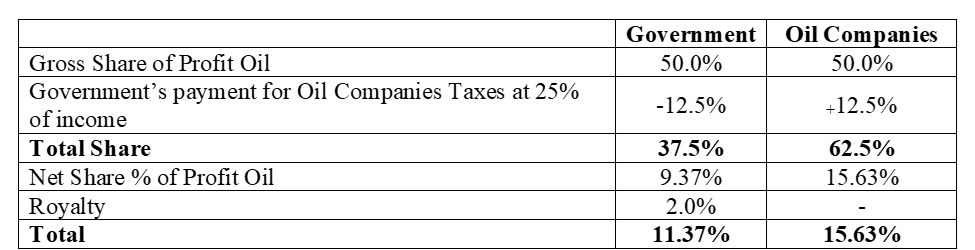

As this column will show, even at the first level at which the Government pays the Corporation Tax liability of the oil companies in accordance with Article 15.4 of the Petroleum Agreement, the Government’s real or net share of oil revenue – what remains or ought to remain in the Natural Resource Fund – is 9.4 % (plus 2% royalty) while the oil companies get 15.6%. The money to pay those taxes comes from the Government share of profit oil, hence the deduction from Government and the addition to the oil companies.

The defenders of Exxon and the Agreement like to think, and go so far as to argue, against common sense, that this is all “massa cow and massa bull” stuff. They forget that like all companies operating in Guyana, the Agreement provides that Exxon and its partners are liable to Corporation Tax in Guyana, or that they do not recognise the difference between the Consolidated Fund and the Natural Resource Fund. Even as the tax is “payable” by the oil companies, the Government pays it on their behalf out of its share of oil revenues, while the GRA is required to issue the receipt in the name of the respective oil company, thus adding to their economic benefits under the Agreement. This constitutes an effective tax holiday until around 2057, that is eight times the standard tax holiday period allowed under the Income Tax (In aid of Industry) Act.

Friday’s column will look at other tax benefits including the tax certificate used to deceive the tax authorities in the home countries of the oil companies.