Sanctity of Contract vs Sovereignty over Natural Resources

Introduction

This column is an adaptation of a presentation I made at an OGGN sponsored activity in New York last July 27. OGGN is a US registered NGO with its membership drawn from the Guyanese Diaspora in North America, Europe and the Caribbean. Dr. Vincent Adams and I were the two presenters. Adams spoke on the environmental implications of intensive fossil fuel production in a concentrated area of 26,000 km2 and of his tenure as head of the (Guyana) Environmental Production Agency from which the PPP/C Administration removed him following the 2020 elections in Guyana. Adams was able to embellish his presentation with anecdotes, incidents and several confrontations he had in the EPA’s oversight of the much discussed and criticised 2016 Petroleum Agreement. That agreement was signed by the APNU+AFC Coalition Government and a consortium of oil companies headed by the American giant ExxonMobil Guyana Inc. a far-removed subsidiary of ExxonMobil Corporation of the USA.

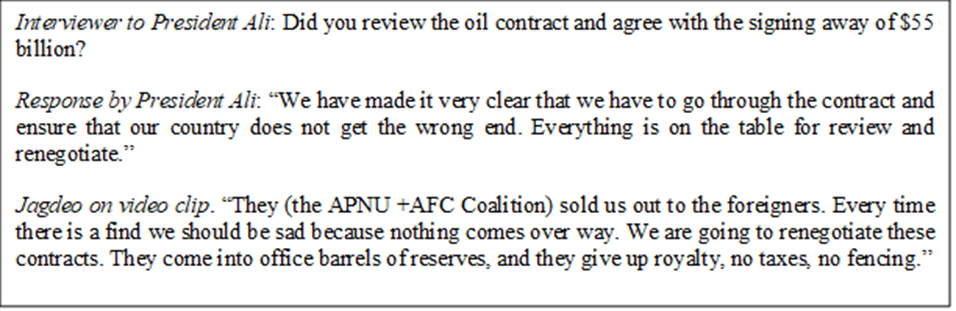

The theme of the activity was Sanctity of Contract versus Sovereignty. Let me begin this presentation by showing two clips that are widely available on social media, one by President Irfaan Ali and the second by Vice President Bharrat Jagdeo.

Having come into Government, both Ali and Jagdeo have left those commitments behind, now repeating the mantra “Sanctity of Contract” . So, for today’s talk, I will look at sanctity and argue that this is not an absolute rule of law but rather is one that is subject to a number of exceptions, anyone of which could cause a contract to be set aside. As I hope to show, the 2016 Petroleum Agreement can be set aside under several of these exceptions.

In this first part of the adaptation, I invite you to look first at the excuse being used by the PPP/C.

Sanctity of Contract

The sanctity of contract is a legal principle which states that agreements, once freely made, should be honored and enforced. It means:

- Contracts are binding.

- Parties must fulfill their promises.

- Courts generally uphold valid contracts.

This principle is important, promoting trust and stability in business relationships. However, when called upon, the courts not only consider the exceptions such as fraud, duress, illegality and unconstitutionality, but may also balance “sanctity” with fairness and the public interest.

First and foremost, my view is that having exhausted an earlier 1999 Agreement between Esso and the Government, Exxon was NOT ENTITLED to a second Agreement. Section 10 of the Petroleum Exploration and Production Act of 1986 conceived of a single Agreement that is phased out after ten years, barring any production licences issued under the Agreement. In essence, section 10 grants the Minister the power to enter into an agreement not inconsistent with the Act with respect to any or all of four specified matters, namely, the granting of a licence, the conditions attaching thereto, the procedure to be followed in exercising any discretion granted to him under the Act and any matter incidental thereto.

Illegality

But this provision was turned on its head under a so-called Bridging Deed conceived by Houston Texas in which one of the recitals states as follows:

“Pursuant to section 10 of the Act, the Minister has entered into this Deed together with the Contractor Parties to set out the process whereby 1999 Licence and the 1999 Petroleum Agreement will be replaced by a new petroleum prospecting licence and petroleum agreement in respect of the Contract Area.”

It is ironic that the Exxon who is now hiding behind “Sanctity of Contract” described at the April 2016 meeting that “the current (1999) agreement with Esso was in several ways out-of-date with what prevails administratively in Guyana and that an approach to Esso in 2010/11 to deal with that was politely declined.” Exxon’s team added that their company was prepared to move to a new “current specimen format for their agreement,” prepared and ready for GGMC to review. Here for all to see is Exxon admitting that it wrote the 2012 Model Petroleum Agreement which was subsequently handed to then Natural Resources Minister and blessed by President Ramotar.

Of particular relevance too, is a report by Clyde & Co., an international law firm based in London, which discloses that Brooke Harris of Exxon was actively engaged in the drafting of the Cabinet Paper on the 2016 Agreement. To be clear, the illegality lies not in the Cabinet Paper but in the granting of a second Agreement and the infamous Bridging Deed. Drafting of the cabinet paper was a sovereignty issue.

Duress

In April 2016, a technical team from the Guyana Geology and Mines Commission visited Exxon in Houston to discuss technical matters relating to a first discovery of oil announced in May 2015. Exxon threatened the Guyana Team with withholding investment until they were granted a new contract. This is how the Head of the GGMC Team reported the threat.

“Esso then confronted with GGMC the matter of their Contract and Licence… For Esso to start spending, the replacement petroleum licence and agreement is needed, along with the undertaking that the Development Plan and permitting would be done in good time.”

Even the Minister whose signature appears on the 2016 Agreement had grave doubts about the Agreement, writing in a book published after he demitted office that he and his Legal Officer “harboured some discomfort about signing”, which he claims, “did not go down well with Exxon top brass”.

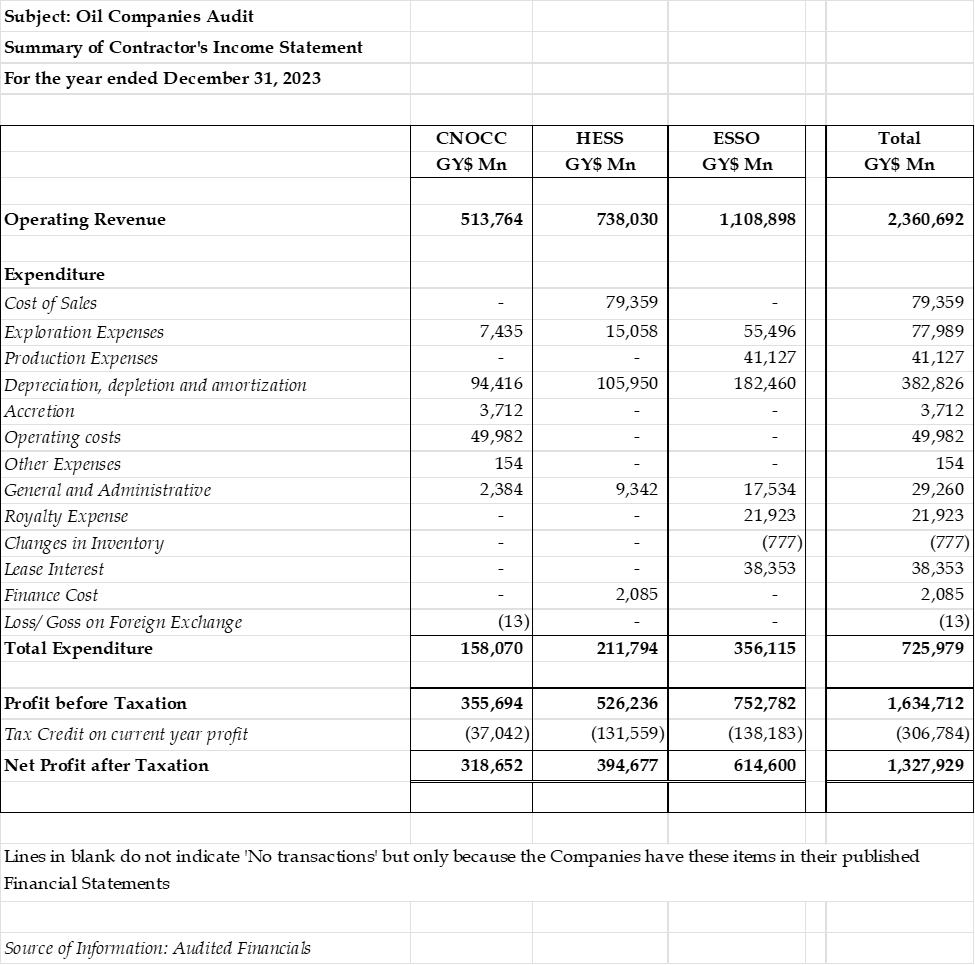

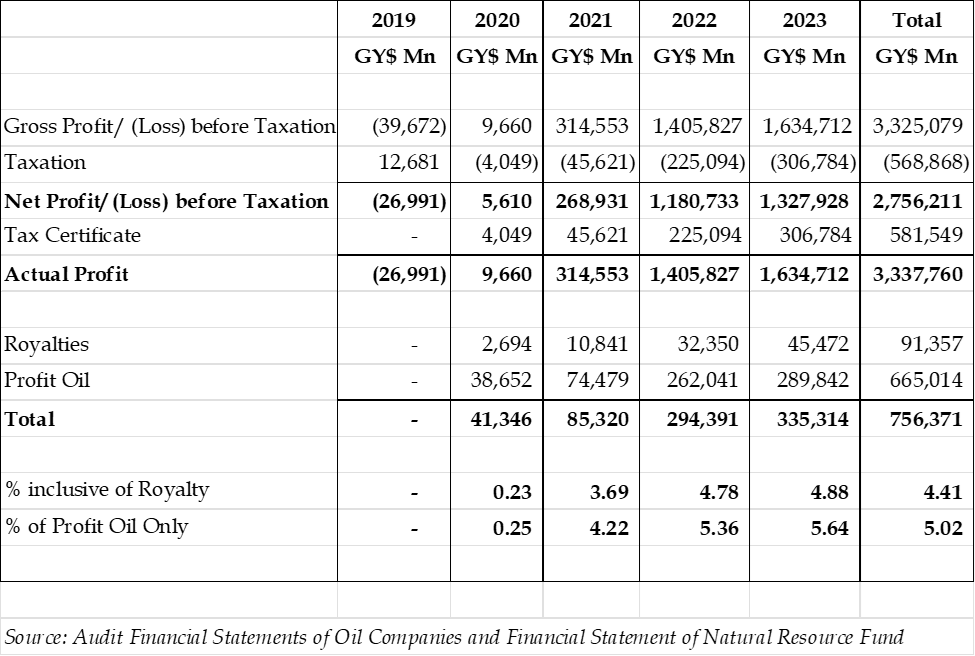

Fairness

On the question of fairness, here is how the 2016 Agreement has worked in terms of distribution of the number of millions of barrels of oil produced. Yes, the oil companies have a right to recover their costs but as the numbers below show, Guyana received 12 % of the total oil produced in the first four years of oil production. Twelve percent must rank as one of the lowest host Government take anywhere in the world. It seems that the 2016 Agreement effectively transferred Guyana’s patrimony and good fortune to Exxon, at the expense of its people.

Compiled by: Ram and McRae

Source of Information: Budget Speech

Next week’s column will discuss unconstitutionality as an element of sovereignty and ask which one the Government thinks ought to prevail.