Questions for the confident Alistair Routledge, Exxon Guyana’s President

Introduction

During the recent Oil and Gas conference in Guyana, Mr. Stephen Sakur, renowned BBC journalist, did a brief interview with Exxon Guyana’s President Alistair Routledge about its operations in Guyana. Unfortunately, the limited nature of the engagement did not allow Sakur the high standard which viewers across the world associate with his flagship programme Hard Talk.

Mr. Routledge was his usual self, confident of the obsequious support of Guyana political leaders. While he has consistently demonstrated a preference for foreign journalists, soft questions locally and false billboards, he would do Exxon a world of good and remove some of the more serious suspicions and accusations against them, if he could provide direct responses to the following.

- Shell had paid Exxon for two farms-in in the Stabroek Block, for a total of 50% interest. Can Mr Routledge say how much was paid by Shell and whether the money was credited to the accounts of the Guyana operations?

- Can he also state for the edification of Guyanese, how much Hess and CNOOC paid to Exxon for their 55% share in the Stabroek Block and whether those sums were credited to the accounts of the Guyana operations?

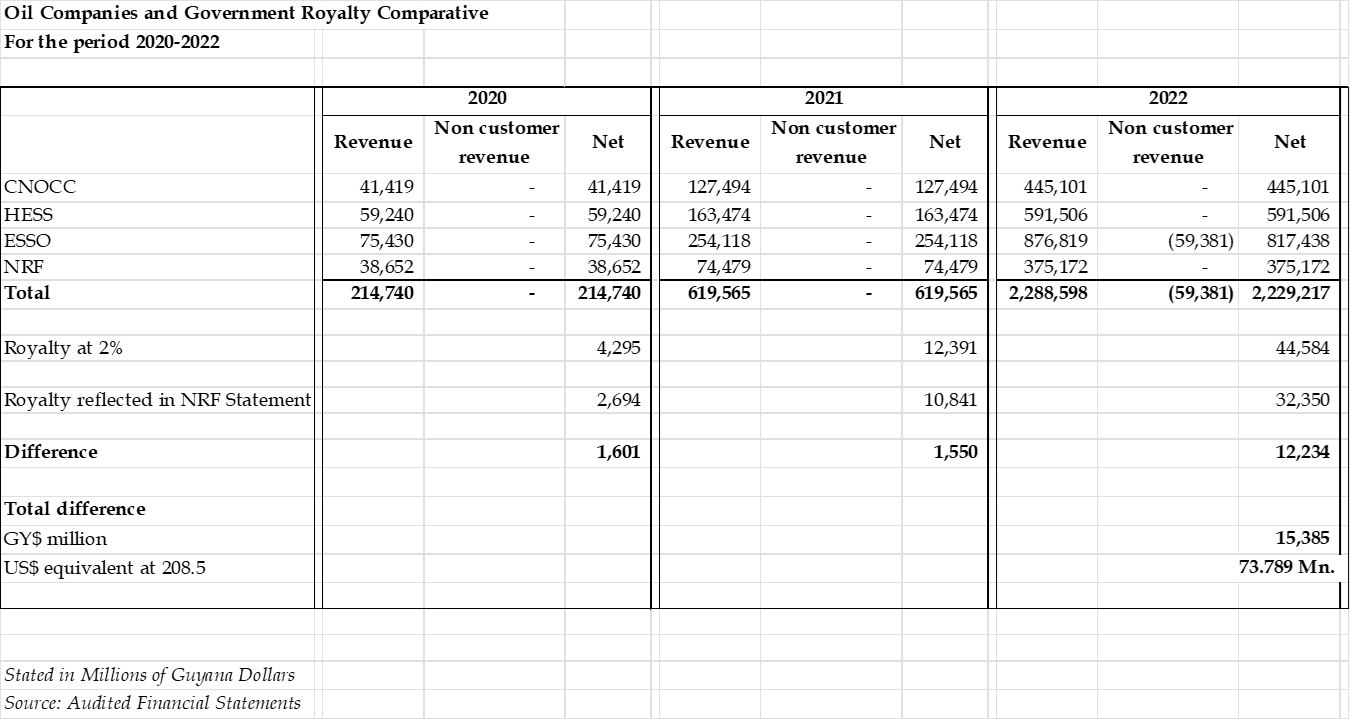

- The audited financial statements of these three oil companies (Exxon, Hess and CNOOC) at 31 December 2015 showed a total expenditure of US$368 million, while the companies claimed US$460 million as pre-contract costs incurred up to that date. Would Mr. Routledge present to the Guyanese public a reconciliation of this difference?

- The Companies Act of Guyana only allows an external company to hold an interest in land with the approval of the President. Would Mr Routledge identify the President who granted that approval to lease land in Ogle?

- Under its lease from the Government of Guyana, Ogle Airport Inc is permitted to sub-lease land only for narrowly defined activities. Can Mr. Routledge identify the government official who authorised the exemption from this requirement to allow for the construction of an Administrative Office, and whatever else?

- Whether Exxon and its partners obtained from the Government approval of their joint operating agreement, the date of such approval and the Minister who granted that approval?

- Whether the purported takeover of Hess by Chevron constitutes an assignment by Hess to Chevron for purposes of Article 25 of the Petroleum Agreement for which approval of the Minister is required?

- Particulars of annual tax credits claimed by Exxon in the USA in respect of its Guyana operations and provide evidence of the GRA certificates of taxes paid, used to claim tax credits.

- Would Mr. Routledge state whether he considers a receipt for taxes not paid by Exxon not only raises legal and ethical questions but violates the OECD/G20 Framework on Base Erosion and Profit Shifting which requires large companies to pay a 15% effective minimum tax rate?

- The Laws of Guyana only allow the petroleum minister to grant to any company a single petroleum agreement. Would Mr Routledge state the statutory basis for a second agreement over the same area even before the first Agreement had expired?

- Can he identify for Guyanese the provision in the Petroleum (Exploration and Production) Act the authority for a Bridging Deed and state the name of the Government official with which Exxon negotiated such a deed?

- Can he state the role of Sir Shridath Ramphal as Escrow Agent under the Bridging Deed and whether he (Sir Shridath) was retained and paid by Exxon or the Government of Guyana, and to meet EITI disclosure requirements, how much he was paid?

- Is it correct that US$15 Mn. of the “signing bonus” of US$18 million was intended to take the legal case against Venezuela to the International Court of Justice, the success of which would be a major benefit to Exxon?

- Would he agree that it is a complete misnomer to describe the US$18 Mn. as a signing bonus?

- There are four types of expenditure provided for under the Petroleum Agreement. Can he provide details of any expenditure under the categories “Costs recoverable only with Approval of the Minister” and Costs “recoverable subject to the approval by Minister” over the past four years?

- Would he provide a statement of the annual costs of petroleum deducted from Gross Revenue for purposes of royalty payment to Guyana under Article 15.6 of the Agreement?

- And further, confirmation that such costs are also not deducted as operating expenses.

- Would he provide an estimate of how much Guyana has lost annually in Profit Oil since 2020 in the absence of ring-fencing?

- Whether Exxon accepts that the Government of Guyana has the power to set conditions on the granting of a Production Licence, including ring-fencing?

- Has the Coalition Government or the current Government formally raised with Exxon the question of ring fencing?

- Former petroleum minister Raphael Trotman wrote in his book Destiny to Prosperity that a named Exxon official was involved in the Cabinet Paper for the 2016 agreement. Would Mr Routledge confirm the name of that person as Mr. Brooke Harris?

- Has Mr. Routledge read the Clyde & Company report into the 2016 Agreement, and does he have any disagreement with the facts set out therein, including the role of Mr. Harris?

- Whether he as the President of Exxon had confirmed that Mr Bobby Gossai had the necessary authority to clear US$211 Mn. of US$214 Mn. not supported by evidence provided to the auditors?

- Has Exxon agreed to pay the Government 50% of the US$214 million which was therefore wrongly claimed, and if not, why not?

- Would Mr. Routledge confirm that the ministerial audit and the Guyana Revenue Authority audit for tax purposes are two separate and distinct audits?

- Can Mr. Mr. Routledge state the quantity of proven petroleum reserves of the Stabroek Block as at the end of February 2024.

- Mr. Routledge must be aware that Mr. Raphael Trotman, former Natural Resources Minister has indicated that he would give evidence in any inquiry into the 2016 Agreement. Would Exxon participate in any Commission of inquiry established by this government to look into the circumstances leading to the 2016 agreement?

- Does Exxon consider that the exploration and production activities in the Stabroek Block harmful to the environment and a breach of the Paris Accord? If yes, what measures are in place to mitigate such effects?

- What is the estimated total cost of the gas-to-shore project and is any cost being charged against Oil Revenue?

- Would the procedures and the valuation of private property compulsorily acquired for the project comparable to how eminent domain operates in the United States of America?

Conclusion

Mr. Routledge is aware that Exxon will be the dominant player in Guyana for the next forty years or more and is no doubt concerned about the negative image associated with the company and its operations. It is in the interest of Guyanese to have answers to burning questions about the 2016 Contract, the company’s operations and the unconscionable situation of a country with a high poverty rate paying the taxes of one of the world’s top companies. He must be aware too that Guyanese have a right to have their questions and concerns addressed, by those who are enjoying the benefits of the people’s patrimony. It cannot be too much to ask a major beneficiary of that patrimony to provide responses that will allay the fears of the people.