Beyond Stratospheric – 2025 Returns for Hess

Introduction

Hess Guyana Exploration Limited – a branch of Hess Guyana Exploration Ltd., a Cayman Islands-incorporated company and 30% stakeholder in the Stabroek Block – is once again the first of the three Stabroek oil companies to file its annual returns and audited financial statements. The company was previously a wholly owned subsidiary of Hess Corporation, incorporated in Delaware, USA, until Chevron completed its acquisition of Hess Corporation on July 18, 2025, pursuant to a merger agreement signed on October 22, 2023.

Also filed at the local Registry were annual returns and financial statements for Hess Guyana (Block B) Exploration Limited, a subsidiary of a Bermuda-based company that formerly held a 20% interest in the Kaieteur Block. A note to the financial statements states that in 2023 the branch relinquished its participating interest in that block. It therefore appears that the branch has ceased carrying on business in Guyana, which under the law requires it to give to the Registrar of Companies notice of cessation within 28 days. I hope that there is no sinister motive for this omission.

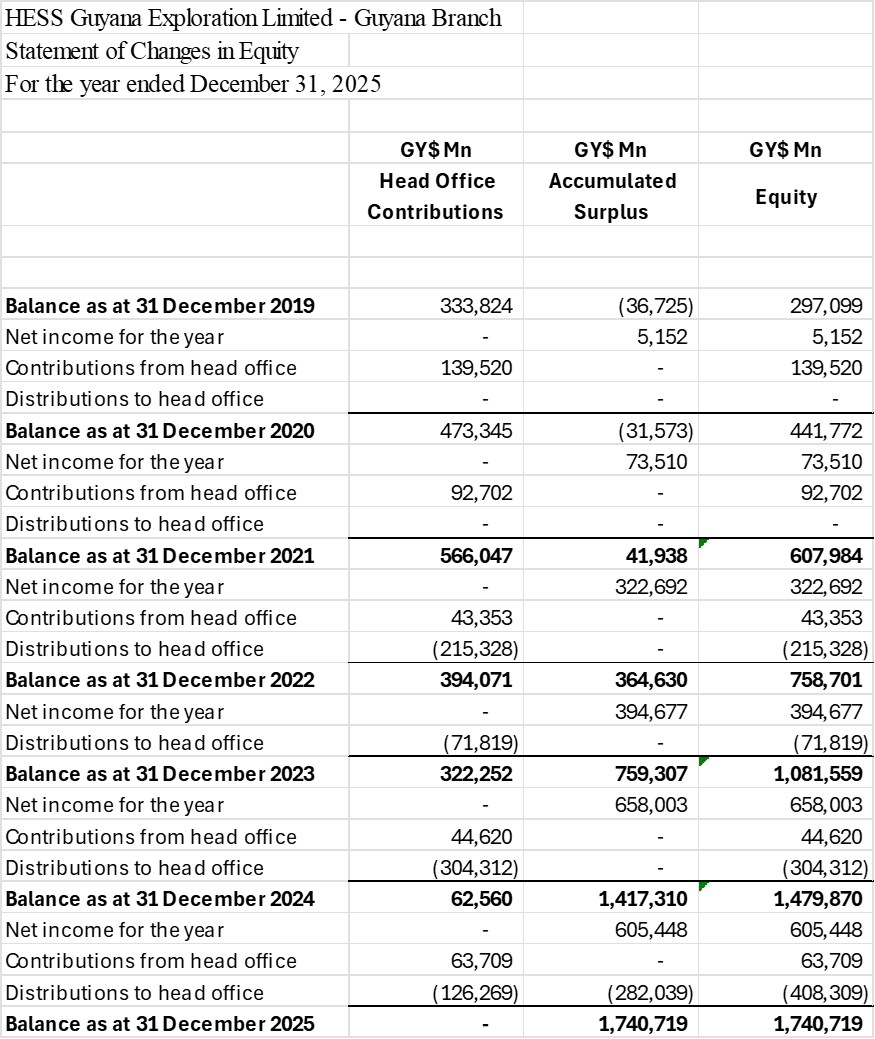

With the formalities out of the way, attention now turns to the financial statements of Hess Guyana Exploration Limited itself. Unlike previous years, the 2025 statements are correctly presented in Guyana dollars. Instead of beginning with the Income Statement or Balance Sheet, this review focuses on the Statement of Changes in Equity – the financial statement that tracks how the owners’ interest in the company changed during the year. The source of the information in this Table is the audited financial statements of the branch.

Source: Audited Financial Statements

Recovery of cost, oil, and plenty of profits

The table shows that over the life of its operations in Guyana, the branch received approximately GY$717.7 billion in Head Office Contributions to finance exploration, development and operational activities. Over time, however, those sums were fully repaid. By 31 December 2025, the balance had fallen to nil, meaning Hess had completely recovered every dollar of its invested capital – not from loans or external financing, but directly from earnings generated in Guyana. And if Exxon’s repeated warnings about force majeure over any Venezuelan threat go unchallenged, companies like Hess could continue extracting wealth – tax free – from Guyana well into the last quarter of this century.

But the recovery of investment capital is only part of the story. After recording net income of GY$605.45 billion in 2025 alone, the branch reports an Accumulated Surplus of GY$1.741 trillion at 31 December 2025, up from GY$1.417 trillion in 2024.

Nor was that surplus simply money left to accumulate in the company. Between 2022 and 2025, Hess made distributions to Head Office totaling approximately GY$999.8 billion. In 2025 alone, distributions amounted to GY$408.3 billion, including approximately GY$282 billion paid directly from accumulated profits. Yet despite these enormous outflows, total equity still surged from GY$297.1 billion in 2019 to GY$1.741 trillion by the end of 2025.

Just to digress. Our Government says it will not order ring-fencing because it wants to encourage the oil companies to re-invest. How little they know!

Every other taxpayer in Guyana is subject to withholding or remittance taxes on profits transferred abroad, including deemed branch profits remitted to overseas parents. Exxon, Hess and CNOOC are exempt under the 2016 Petroleum Agreement. Put a number to it. Had withholding taxes applied to the actual and deemed remittances, Guyana would have collected approximately GY$409 billion. Instead, Guyanese taxpayers are effectively subsidising one of the most profitable oil operations in the world while some of the world’s most successful companies enjoy a virtually tax-free pipeline for exporting billions abroad to the world’s largest economy.

More outrageously still, these companies pay no corporation tax in Guyana, yet receive certificates declaring that taxes were paid on their behalf by the Government of Guyana – certificates they can then present in their home jurisdictions to avoid taxation there as well. It is a legal fiction so absurd that it borders on fraud.

Comparison with Guyana’s Natural Resource Fund

The scale of Hess’ earnings becomes even more startling when compared with Guyana’s Natural Resource Fund (NRF). In 2025, the Fund recorded profit oil inflows of G$451.2 billion, royalties of G$68.9 billion and G$3.1 billion from the signature bonus. Since inception, the NRF has accumulated approximately G$1.579 trillion from profit oil, G$232.9 billion from royalties and G$3.1 billion from the signature bonus, for total inflows of roughly G$1.815 trillion.

This means that Hess Guyana’s accumulated surplus alone – GY$1.741 trillion – is now almost equal to the total petroleum revenues Guyana has received through the NRF since oil production began. Put differently, the retained profits of a single foreign oil company are approaching the entire sum deposited into Guyana’s sovereign wealth fund. The comparison is even more striking because Hess holds only a 30% interest in the Stabroek Block. ExxonMobil holds 45% and CNOOC 25%, meaning the consortium’s combined earnings are vastly larger. Unfortunately, the accounting disclosures, unresolved audit issues and opaque financial reporting surrounding the other companies make any simple extrapolation risky.

A Comparison That Should Enrage Guyanese

And here is another comparison that should make every Guyanese seethe with anger. Guyana’s entire 2026 national budget is $1.558 trillion, yet Hess’s accumulated profits from the Stabroek Block now exceed the State’s total annual budget and are almost four times the Guyana Revenue Authority’s projected tax collections for 2026.

Only months ago, Finance Minister Dr. Ashni Singh boasted about presenting the “largest Budget ever.” Yet the retained profits of a single foreign oil company operating in Guyana now exceed the amount the Government proposes to spend on the entire country in a year. This is the real meaning of President Irfaan Ali’s obsession with “sanctity of contract” – political servitude disguised as policy. While Exxon, Hess and CNOOC reap profits larger than Guyana’s national budget, the President defends a contract so lopsided that no leader genuinely committed to his people could justify it.

The parallels with the first wave of “discovery” are chilling. Then, foreign adventurers arrived with shiny beads, disease, and promises of prosperity, only to carry away gold and wealth while the natives remained poor, dependent or dead, and received trinkets. Today, the caravels have become FPSOs, the crowns have become corporate logos, and the conquest is wrapped in production-sharing agreements instead of royal decrees. But the outcome is hauntingly familiar: Guyana’s wealth flowing outward while its leaders act as overseers for foreign extraction.

The result is a humiliating national reality: one foreign oil company can accumulate more wealth from Guyana’s oil than the Government of Guyana can spend on the entire country in a year – and the President still calls this success.

Part 2 of this column will appear on Tuesday coming.

This column first appeared on chrisram.net and is reproduced with the kind courtesy of the author.