Introduction

Following this column’s review of the 2012 Annual Report on the Demerara Tobacco Company Limited in which I stated that I am a small shareholder (500 shares) in the company, a colleague of mine criticised me for profiting from a company whose product is now known to be a killer. I explained to him that the reason for the shareholding is to ensure that I receive the annual report of the company and have the right to attend company meetings. Similarly, for as long as I can remember I have had shares in DDL and Banks DIH Limited despite the fact that I believe there are personal, economic and social consequences for those who engage in excessive use of rum, which is their principal product. After careful consideration and with some regret at my belated decision, I wrote in my review of DDL’s 2012 Annual Report that I would be disposing of my small shareholding in that company, except for a few to allow me to receive the company’s annual reports. My action stems from my conviction that there is such a concept of ethical investing.

Ethical investing or, as it is sometimes referred to, socially responsible investing, has been gaining popularity as individuals seek to align their investments with their personal views, whether they are based on environmental, religious or political precepts. Essentially it comes down to this: should a vegetarian invest whether directly or indirectly in a company that owns and operates abattoirs, or an anti-alcohol group invest in a rum company or a Cancer Society in a tobacco company?

Original sins

An internet article notes that socially responsible investing used to just be about not investing in tobacco, alcohol and oil sands, but that more recently while ethical and socially responsible investing are still those things it now extends to investment in companies that investors respect and value for their contributions to society and the environment. The same article quotes one writer who has observed that a “growing number of investors want their [investments] to help save the planet, their souls or both.”

The corporate form which allows those with ideas and entrepreneurship to partner those with capital in the form of the limited liability company is regarded as one of the greatest inventions of the human mind. While it has had its bumps on the way with some of the most famous scams perpetrated on innocent individuals the world would not be the same had it not been for the limited liability company. Unfortunately for Guyana there are too few public companies in which the members of the public can invest by buying shares. Indeed since 1992 we have had a contraction in publicly owned companies as ownership contracted whether in state owned companies such as Guyana Telecommunications Limited which was replaced by the ATN of the United States, Guyana Stockfeeds Limited owned by Robert Badal or JP Santos and Co Limited owned by the Fernandes Group. In the case of the latter two, while they remain public companies they have the operating characteristics of a private company.

The options

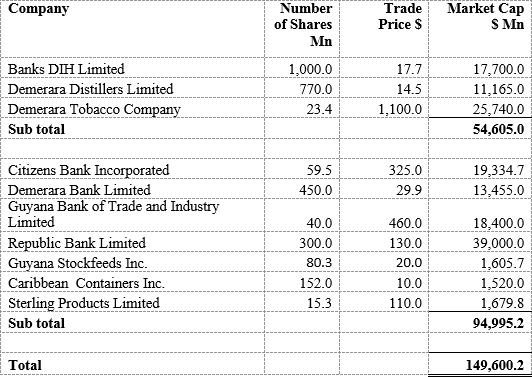

So what then is left for public participation and those who may choose to engage in what is referred to as ethical investing? Here is a table of the market capitalisation of companies traded on the stock exchange.

Source: GASCI

The total value which the stock market places on the principal companies, not all of which actually trade, is some $149.6 billion inclusive of some double value since the shares of Banks DIH will reflect the fact that it holds shares in Citizens Bank Limited, which is also quoted on the stock market. If we break the companies into two groups – those engaged in the ‘sin’ products of alcohol and tobacco, and others, we see that the market value of the former group accounts for $54.6 billion, or 36.5% of the total. Of course investing, like life, is neither pure nor simple, and we are familiar with the very popular non-alcoholic other products and services offered by both Banks DIH and DDL. If one is a puritan, or a serious Muslim, this can be quite a dilemma.

Puritan’s choice

So let us suppose that one is indeed a puritan and decides to exclude from one’s public companies investments all the ‘sin’ product companies. That will leave only the four commercial banks, Guyana Stockfeeds Inc, Caribbean Containers Inc and Sterling Products Limited. These are all controlled public companies and the number of shares that are likely to be available on the market during any year is extremely limited. In every practical sense, Guyana Stockfeeds is a private company with its principal shareholder Mr Robert Badal owning more than 75% of the issued shares. In the case of the four banks there is majority control of 50.97% in RBL; 61% in the case of GBTI; an interesting 85% in the case of CCI; and 58.1% in Sterling Products.

With the world’s penchant for the environment the company with the best socially acceptable operation would be Caribbean Containers Inc, the paper recycling and box-making business. However that company has had a string of failures under much stronger management than now exists, and any investment would have to be based on the company’s potential rather than its current management and capacity. Indeed it will take quite a bold person to invest in a company which is 85% controlled by a single shareholder.

The debate

So with the limited number of shares likely to come to the market, the scope for ethical investing is severely restricted. The alternative is to seek investments outside, but since the purpose of this column is not even remotely to try to offer investment advice I will return to the general nature of the column which is the underlying theory of ethical investment and some of the academic arguments for and against the practice.

One writer against the idea is Pat McKeough of the Toronto Star who in a March 28, 2011 article titled ‘Does ‘ethical’ investing make any sense?’ expressed concern around isolating industries from one’s investment portfolio. One of his principal contentions is that ethical investing does not yield sufficient returns to satisfy investors. Then there is what is called ‘green washing’ where a product is clothed in environmentally friendly garb and promoted with misleading hype but which can be just as damaging to the environment as it its non-green competitors.

A study done a few years back in Australia and addressed in an academic journal provided the opposite argument. The study, based on data for the period 1992-2003, provided evidence on the performance and investment style of retail ethical funds in Australia. The study over the long haul showed no evidence of significant differences in risk-adjusted returns between ethical and conventional funds during 1992–2003. However when the data were disaggregated it was noted that during the period 1992–1996 domestic ethical funds under-performed general funds, but that during the period 1996–2003 ethical funds matched the performance of conventional funds more closely. According to the authors, this suggested that ethical mutual funds underwent a catching up phase, before delivering returns similar to those of conventional mutual funds.

The authors concluded that the Australian data provided corroborative evidence that ethical funds do not under-perform relative to conventional funds and that there was no financial penalty for being an ethical investor in Australia during the 1992–2003 period.

Conclusion

The investor seeking to build any investment portfolio in Guyana has a real difficulty in putting together any basket of shares. The shallow market should drive up share price but corporate performance in Guyana is generally modest and has the opposite effect on price. Indeed the strange phenomenon whereby the shares of a shell company with no assets to talk about has a market value which is 230% that of DDL and 145% that of Banks DIH Limited is an eloquent statement on all three of them, but that is a topic perhaps for another column. With the interest rate paid on deposits by the banks being lower than the rate of inflation, that is not too good an option. The ethical investor has his own ethical dilemma.