There is a precedent for renegotiating the 2016 Petroleum Agreement. Time for this Government to show some spine

More than three years ago, and even before the first barrel of oil was produced, the 2016 Petroleum Agreement signed by Esso Exploration and Production Guyana limited (Esso) and Hess and CNOOC, its Joint Venture partners, concluded its first renegotiation with the Government of Guyana. The result was a Deed of Amendment (the Deed) signed by the oil companies and President David Granger in his capacity as Minister responsible for petroleum.

Specifically, the Deed amended Section 3.3 of Annex C – Accounting Procedure, to provide expressly that royalty paid by the Contractor under the Agreement would not be recoverable. Those who had argued that royalty was not a recoverable expense must have known of the renegotiation of this provision but never thought it necessary to share that information.

The APNU + AFC Coalition suffered a barrage of criticism for what is often referred to as a lop-sided oil contract. But the Coalition must be given some credit for at least effecting the renegotiation of one element of the Agreement, albeit not a particularly major one. The question inevitably arises why the current Administration keeps repeating the mantra of sanctity of contract, driving fear into Guyanese of the consequence of any attempt at renegotiation. Interestingly, the APNU+AFC’s renegotiation was conducted without a change in circumstances, while the incumbent Administration is adamant that it is powerless to even broach the question with the oil companies.

Putin’s misguided special military operation has dramatically and adversely affected the world economy and has impacted almost every household in the world, including those in Guyana. We now pay substantially more for cooking gas, petroleum, and minibus fares, substantially because of the huge increase in the price of petroleum products. Consequently, the oil companies are making unprecedented profits and are allowed to keep those profits all to themselves and their foreign shareholders. One would expect to see a caring government taking the side of the population, sometimes from two sides – a cap on prices as well as a windfall tax. In Guyana, our Government does the opposite: it takes the side of the oil companies and ignore the plight of the consumers.

But our situation is actually worse than this. The huge spike in fuel prices mean super profits for the oil companies. In theory, the higher profits give rise to higher taxes but under the APNU+AFC contract, it is the taxpayers of the country who are called upon to pay those higher taxes, out of our share of profits from the extraction of our oil. That is almost criminal.

This arrangement, sometimes referred to as “pay on behalf of” is clearly unsustainable. I noted in a recent letter I wrote in the media that the Natural Resources Fund is overstated by tens of billions of dollars. The high profits being earned by Esso and its partners will necessitate an increasing share of our NRF going to pay the taxes of the oil companies. Despite the OECD 15% minimum tax, the American partners under the Agreement will then claim the tax we pay as credits against their home tax obligations.

The apparent reliance on better contract management in place of reasoned renegotiation may sound good but it seems designed to deceive. It is both the PPP/C and the APNU+AFC that have given Guyana this abominable contract. Contrary to what Vice President Jagdeo said a few nights ago on the Glenn Lall Show, the 2016 Agreement was based on the Robert Persaud – Donald Ramotar 2012 Model. How can we better manage a contract when we know not its origin, its content, or its implications? Indeed, it is still my strongly held view, that Esso was not entitled to a second Agreement. We may not be able to reverse the 2016 Agreement, but that should not mean that we have to prostrate ourselves at the feet of Esso, Hess and CNOOC, as our leaders are doing.

Let us take the example of the APNU+AFC and demand renegotiation.

EEPGL ignores tax provisions of 2016 Agreement in its 2021 financial statements

Introduction

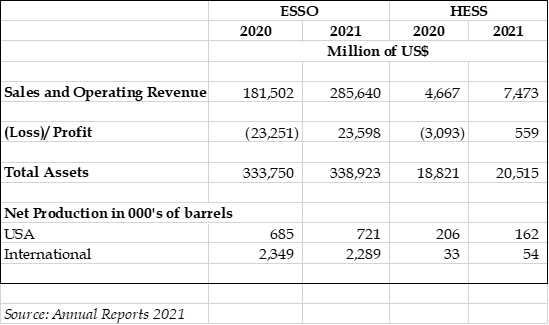

By a strange coincidence, this 100th. column features the 2021 financial statements of Esso Exploration and Production Limited, the designated Operator and holder of a 45% interest in the Stabroek Block under the 2016 Petroleum Agreement. Esso signed its first such agreement in 1999 with the PPP/C Government as a sole Contractor and a second in 2016 with the APNU/AFC Coalition with Hess (30%) and CNOOC (25%) as added Contractors. Esso holds the remaining 45%. These percentages do not, however, reflect the relative size and influence of the ultimate international parents of these branches. It is no accident that Steve Coll, chooses as the title of his seminal book on Exxon, Private Empire: ExxonMobil and American Power. Its vast annual revenues exceed the economic activities of the great majority of countries and, with implications for Guyana, ExxonMobil’s sway over politics and security is often considered greater than that of the United States embassy in that country.

As we did last week in the review of Hess Exploration and Production Guyana Limited for which we did a brief review of its ultimate parent, we will comment briefly on some of the salient features of the annual report of ExxonMobil, the ultimate parent of the local branch operating in Guyana. Exxon is a giant compared with Hess. Here are some performance statistics.

Guyana does feature as prominently in Exxon’s report. But all references are positive. Here are a few:

Guyana contains one of the largest oil plays discovered in the past decade.

Exploration success continued with additional discoveries increasing the estimated recoverable resource in the Stabroek block.

Exxon envisions six projects online by 2027, with the potential for up to 10 projects.

Exxon is probably aware that no legal contortion or high price fiddle will allow them another Petroleum Agreement and that by 2026, the Contractors will have to relinquish all areas other than those covered by Production Licenses issued under the 2016 Production Agreement.

Like Hess, Exxon’s taxes also tell an interesting story. Despite 38% of its revenue being derived from the United States, the US made up only 3.29% of the total federal and non-USA paid by Exxon. And of course, nowhere in the report is there any indication that there are cases where the payment is a paper transaction.

Guyana

Income

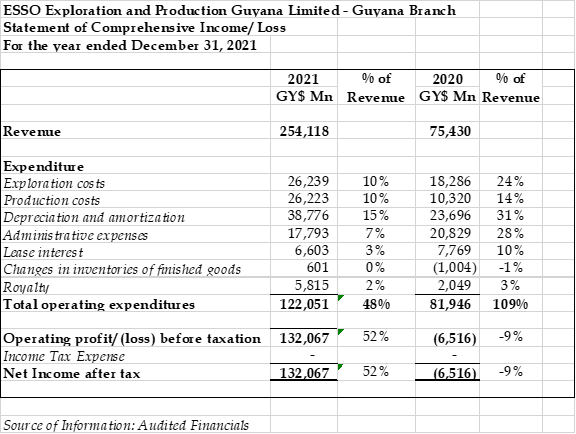

It has been a bumper year for the Guyana branch with revenue of $254,117 million, a growth of 2.4 times from 2020, compared with a growth in revenue of the international parent of 57%. Given the growth in revenue, it is not surprising that all other indicators were substantial improvements over 2020. For example, production cost represents 10% of revenue in 2021 compared with 14% in 2020; depreciation and amortisation has reduced from 31% of revenue in 2021 to 15%; Administrative expenses from 28% to 7%.

Again, we see how our country’s ineptitude allows the oil companies to make a mockery of best practice in petroleum operations as well as in taxation. Here’s the catch: If the GRA was to disallow the exploration costs as not meeting the income tax test of “wholly and exclusively incurred in the production of income”, the taxable profit will actually increase and the amount of tax represented as paid in Guyana will actually increase.

Although not obvious which line item it is charged to, the financial statements carry a note “The amount of restoration obligation includes costs related to petroleum exploration and production activities for decommissioning of floating, production, storage and offloading facility and reclamation of sites.” Some indication is given, however, in the Statement of Cash Flows which show a non-cash charge of $8,754 million as Other long-term obligation provision which is most certainly the de-commissioning provision. If this is in fact a general provision, it should be disallowed for tax purposes, which accrues to the Company’s benefit.

On the question of tax, Esso is in complete denial. The entire report is silent on tax, either as a note, a charge or deferred tax.

Balance Sheet and Cash Flow

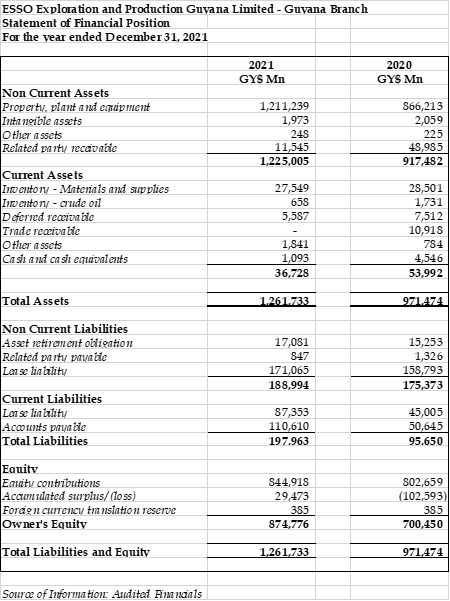

The total assets of the Branch, net of depreciation and write-offs, have moved by $290,259 million to $1,261,733 million. Of this total, Property, Plant and Equipment accounts for $1,211,239 million or 96%. The major additions to this class of assets were $319,678 million in work-in-progress for Wells and facilities and $75,477 million in leased Drill Rig assets. Other significant items of assets are Related party receivable of $11,545 million and Inventory – Materials and Supplies of $27,549 million representing drilling of 2021 exploratory and development wells. There is an amount of $5,587 million of Deferred receivable, representing cash call bookings, net of joint billing costs.

The branch started the year with $4,546 million and ended with $1,092 million, despite a $251,198 million being generated from Operating activities. Lease interest paid amounted to $6,603 million while the principal repayment of lease obligations amounted to $7,236 million.

Committed capital expenditure over the next three years is $235,706 million, compared with $359,941 million stated in the 2020 financial statements. Despite the plans announced in the Parent’s report of several wells, for the next few years, the pattern of expenditure shows capital expenditure commitments as follows:

Next week: a round up and commentary on these financials.

Token GRA tax receipt helps Hess avoid paying taxes in the US

Introduction

In this Part 99, we address our attention to the 2021 audited financial statements of Hess Exploration and Production Guyana Limited (the branch) which despite its name, is in fact a branch of a Cayman Islands incorporated subsidiary of the American oil major Hess Corporation headed by John Hess. Of the heads of the three contractors under the 2016 Petroleum Agreement, Mr. Hess is by far the most open, even garrulous, when it comes to Guyana. But not without reason.

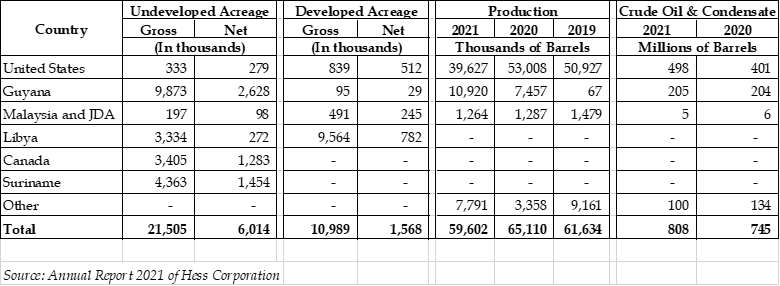

Guyana is the jewel in Hess’ crown, its cash cow, its redemption and its future. From ground zero two years ago, Guyana accounted for more than 25% of the Corporation’s global crude oil production in 2021, even as Hess has seen its North American production decline by more than 20% between 2019 and 2021. And of the Corporation’s gross and net undeveloped acreage, Guyana represents 45.9% and 43.7% respectively while 25% of the proved reserves of crude oil and condensate the Corporation is situate in Guyana.

Malaysia and JDA: Malaysia – Thailand Joint Development Authority.

That elusive tax

The taxation information is at once revealing and a vindication of the fears of commentators. The Statement of Consolidated Income shows a tax charge of US$600 million but that includes the amount of US$113 million “paid” by the Government of Guyana on behalf of the local branch for which Hess gets a token receipt. In a discussion on taxes, the Report informs the reader that the tax charge in 2021 was “primarily due to higher pre-tax income in Libya and Guyana”. The report also shows that income tax attributed to Guyana and Libya accounted for 92% of the taxes shown as a charge in Hess’ report for 2021. It is unclear whether the amount of US$436 million shown as paid in Libya in 2021 was a paper transaction as is the case with Guyana but given Libya’s sensible and logical position with oil companies, it is unlikely that that country’s political leaders would be as shamelessly obsequious to the oil companies as leaders Guyana and its leading politicians have always been.

It would be ironic but not surprising if, in the near future, the lion’s share of taxes payable in the Hess world comes from Guyana! Note 15 to the Report leaves no room for speculation or deduction – Hess paid no taxes in its home country from which it derives two-thirds of its crude oil production! Yet the oil companies are willing to argue in the Guyana courts that if they have to pay tax in Guyana, their business will suffer.

But things are so good for John Hess and the shareholders that in his letter to them he confidently predicted that all four of the Corporation’s production assets would be free cash flow generative in 2022 and is positioned to grow its cash flow at a “compound rate of 25% per year out to 2026”. It only gets better: with Liza Phase 2 beginning production in February 2022, at capacity, Hess is expected to add more than $1 billion of net operating cash flow annually, having repaid the remaining $500 million of its term loan; distributed a 50% increase in quarterly dividend; and committed to return up to 75% of its adjusted free cash flow annually to shareholders by increasing dividends and accelerating share repurchases.

And to think that Hess has less than one-third interest in the Stabroek Block. But Hess, and even more so Exxon, enjoy such confidence and respect of this country’s Government and the Opposition that they are proud to boast of their cooperative relationship with the oil companies and defend the iniquitous contract.

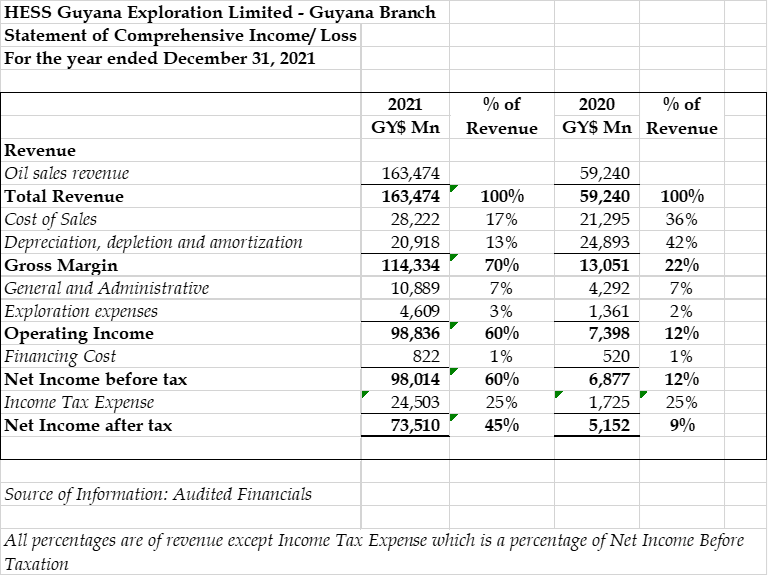

Let us now turn to the financial statements of the Guyana branch in which all figures in Guyana Dollars, unless otherwise stated.

Table of Income Statement

Crude contract, crude share

Using information in the Hess Corporation’s report on average price earned from Guyana crude, the branch sold approximately 11.4 million barrels in 2021, compared with about 6.1 million barrels in 2020. The financial statements of the branch state that it had no related party transactions in 2021, suggesting that those who direct the sale of the branch’s production bypassed the Group’s marketing subsidiary and chose other outlets to sell its share of profit oil and recoverable costs.

From the $163,474 million, deductions are made for Cost of Sales $28,222 million (17% of sales revenue) and Depreciation, depletion and amortisation (DPA) of $20,918 million (13% of sales revenue), leaving a gross margin of $114,334 million or a staggering 70%. A separate note shows that cost of sales is made up of production expenses of $25,635 million, royalty of $$3,923 million and change of inventory of $1,337 million. Royalty as a percentage of sales works out at 2.40%, compared with 2% provided under the Petroleum Agreement. The DPA is made up of $20,874 million in respect of development assets, representing approximately 5% of development assets, and $44 million on Leasehold assets, representing 4% of those assets.

Note 5 states that additions to Property, plant and equipment include the impact of new provisions and revisions for decommissioning obligations.

Deductions are also made for General and Administrative expenses of $10,859 million, up from $4,292 million in 2020, and include pre-development costs of future projects, and Exploration expenses of $4,609 million, up from $1,360 million, suggesting multiple cases of the productive operations carrying the cost of exploration activities. This violation of accounting, taxation and petroleum principles activities would not be tolerated anywhere except Guyana.

The insane Petroleum Agreement

The income statement also shows financing cost of $822 million, up from $520 million in 2020, a sum which also appears in the note on provisioning in the balance sheet. After all these costs are deducted from revenue, the Branch reports net income before taxation of $98,013 million (2020 – $6,877 million), which but for the Petroleum Agreement would be subject to Corporation tax (25%) and to withholding tax (20%) on the deemed distribution branch profit tax (BPT). A deemed distribution is the balance of profit after the Corporation tax less any re-investment of such profits, subject to the approval of the Commissioner General.

The Agreement also states that such tax must be included in the taxable income of the Contractor, meaning that the $98,013 million has to be treated as if it is a post-tax amount, requiring grossing up.

Since the Agreement exempts the oil companies from the BPT, the Branch then deducts the 25% from the profit, or $24,503 million, (2020 – $1,725 million) as though it is an actual sufferance rather than a benefit to be grossed up under Article 15.4 of the Petroleum Agreement. Hess the parent then gets a double benefit by claiming it as overseas tax paid in its US financial statements.

Using its own brand of phoney accounting which treats a benefit as a charge, Hess records a Net Income after tax of 45%, instead of 70%.

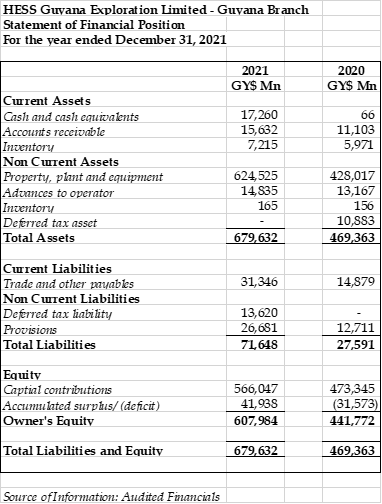

Balance Sheet

The total value of assets of the Branch at yearend was $$679,631 million ($469,363 million) of which Property, plant and equipment accounted for 92%, with the remainder spread fairly evenly over cash, receivables and advances to operator (Esso). At December 31, the amount of such advance was $14,834 million while Trade and other payables of $31,346 million, (2020 – $14,879 million) “mainly relate[d] to amounts owing to [Esso]”.

The Branch’s cash resources stood at $17,260 million, a substantial increase from the $66 million at December 31, 2020, while its commitments for capital expenditure on the Stabroek Block was “approximately $607,000 million (US$2,900 million), up from G$544,000 million (United States Dollars: $2.6 billion), “to be incurred over the next several years”.

Conclusion

As it was in 2020, the financial statements reveal very little by way of disclosure. Readers are no better informed of what makes up exploration, operating costs, and the less significant general and administrative. Even the most ordinary company in Guyana produces financial statements that are more informative, reader-friendly and superior to those of Hess’ Guyana branch. What is particularly noticeable, is that the financial statements of the Hess branch are neither consistent with those of its parent abroad or of any of its joint venture partners locally.

Next week’s column will feature the financial statements of Esso Exploration and Production Guyana Limited.

Last week’s column began a short series on the 2021 financial performance of the three companies – Esso, Hess and CNOOC – which hold 45%, 30%, and 25% respectively of the highly productive Stabroek Block, a find which has placed Guyana on the world’s petroleum map. CNOOC is the newest participant in the arrangement, having paid ExxonMobil in 2014 to acquire a 25% working interest in the Block as a “non-operated joint venture partner”. Why and how CNOOC could pay Exxon rather than the Guyana entity which held the licence is something which no one has yet been able to explain. What this shows is how naïvely reckless Guyana has been in dealings with Esso and why Exxon is seen as dishonest, exploitative, and contemptuous of Third World countries.

CNOOC, like its other two partners, is a branch of a company incorporated outside of Guyana and traces its parent to the People’s Republic of China.

The company reported net income before income taxes of $84,472 million, an increase of 808.5% over 2020 on Net Sales of $127,494 million, which grew by a more modest 207.8%. The Branch reports expenditure on exploration activities of $3,623 million which runs counter to its self-description as a “non-operated joint venture partner”, reflecting the absence of ringfencing in the Agreement and the failure by the government to grant unconditional production licences, at best gross irresponsibility on its part.

Operating costs of $18,570 million was 14.5 % of revenue down from 40.7%, showing the impact of oil price on the performance of oil companies and more so the bonanza which oil companies are reaping.

Then the Statement gets more interesting. Form the net income, the Statement shows a deduction of $21,118 million as Deferred income tax which it does not and will never pay, despite the rather misleading statement in the notes that it is “subject to the Guyana income tax act.” That nonsensical position is further maintained with the statement that at the end of 2021, the company had a deferred tax liability of $16,439 million “as it is probable that future taxable amounts will be paid”!

The giveaway however is in the Cash Flow Statement in which the identical amount deducted in the income statement – $21,118 million – is added back as a non-cash tax benefit! In other words, instead of deducting the $21,118 million, that amount, which represents the tax which the Government will have to pay to the GRA on behalf of CNOOC, that sum should be added to the amount reported by the company, giving a true net profit of $105,590 million.

Turning to the Statement of Financial Position, total assets is made up mainly of Property, Plant and Equipment of $626,531 million, of which $497,995 million is invested in Development Assets, $125,136 million in Exploration and Evaluation Assets and $400 million is in Office Equipment and Others.

Capital Expenditure in 2021 was $191,570 million, an increase of 40% over the amount expended on capital expenditure in 2020. The expenditure incurred in 2021 was considerably less than the amount contracted, but not provided for at December 31, 2020. The company’s balance sheet shows an amount of $53,539 million provision for Decommissioning and restoration, an increase of $14,174 million which again is a strange item given that CNOOC self-describes as “non-operated joint venture partner”.

Unlike its two co-venturers, CNOOC maintains no inventory. It continues to sell its share of the oil lifts to an affiliate in Singapore on a cargo-by-cargo basis. Despite this arrangement the company owes its related parties more than $400,000 million, the terms and conditions of which, including interest, are not stated.

Unlike its co-venturers as well, the company’s financial statements do not disclose any royalty payment to the Government which seems to violate Extractive Industry Transparency Initiative (EITI) requirements.

Conclusion

As it was in 2020, the financial statements reveal very little by way of disclosure. Readers are no better informed of what makes up exploration, operating costs, and the less significant general and administrative. Even the most ordinary company in Guyana produces financial statements that are more informative and reader-friendly that CNOOC’s.

CNOOC, the smallest of the three contractors in the Block recorded a NET profit in 2021, inclusive of the non-cash tax benefit of some $105,590 million before writing off any prior year losses. By contrast, the revenue earned by the Government from its share of profit oil is $74,479 million GROSS.

Next week’s column will feature the financial statements of Hess.

Exxon and partners made more money than God …. er Guyana

It is more than five months since the 96th. column was published on January 22nd. of this year. That column summarised the court action brought by citizen Glenn Lall seeking declarations against the tax provisions contained in the 2016 Petroleum Agreement. The respondent named in the action was the Attorney General. But Exxon, which is the largest investor and the Operator (Co-ordinator) in the Stabroek Block could not leave the matter to be settled between a Guyanese and his Government. It sought the Court’s permission to be joined in the action with the unpleasant consequence that the case is now Esso and the Government of Guyana vs. a citizen of Guyana.

In seeking to convince the Court of its right to be joined in the action, Esso declared that the Petroleum Agreement was “solemnly negotiated with the Guyana Government” and that certain fiscal arrangements made the various Projects “financially feasible and commercially viable.” Solemn for Esso includes bullying GGMC Head Newell Dennison on a trip to the Exxon Campus in Texas which has been repeatedly commented on in my writings on oil and gas, and the arm-twisting of then Natural Resources Trotman’s Ministry into the signing of the 2016 Agreement, so well documented in the Clyde & Company report on the circumstances surrounding the signing of the Agreement.

It is unfortunate that senior members of the current Administration seem unmindful of the experience of Dennison or the damning indictment of the APNU+AFC in the Clyde & Co. report, regardless of the fact that it involved a major heist of the country’s natural resources by Exxon and its partners.

The citizenry had long lamented the damage which Trotman and the Granger Administration had caused Guyana, through one of the most lopsided petroleum agreements of the modern age.

The extent of that damage has manifested itself in the audited results of the performance of the three members of the Consortium – Esso, Hess and CNOOC – in 2021. They not only show exactly what Esso means by “financially feasible and commercially viable” but also that there is neither shame nor limit to the greed of Esso and its partners. To put it in a nutshell, or rather a simplified Table, Esso and its partners made more money in 2021 from the Stabroek Block than all the money raised by the whole of the Government in 2021, including its takings from oil. Not by a few millions but by billions. The following two Tables put it more starkly than any column can.

Oil Companies income

Table of Income Statements

A brief comment on the item Tax Credit in the Table above. Article 15.4 of the Petroleum Agreement requires that the tax liability computed under the Income Tax Act and the Corporation Tax Act to be paid to the GRA on behalf of the oil company and that “such sum will be considered income of the oil company. The income statements of Hess and CNOOC state that they are subject to Corporation Tax without disclosing that the payment is to be made by the Government of Guyana and that the amount of the tax paid by the Government is considered income of the company! Esso’s financials are simply silent on taxation altogether.

Current year profits would attract tax credits of $78,638 Mn. so that the total earned by the oil companies would be $391,191 Mn, or the equivalent of $1,862 Mn US Dollars, reduced by any set-off of losses. There is however, another unknown element: the tax laws require branches of overseas companies to pay income tax withholding tax of 20% of the after-tax income, other than in the reinvestment in fixed assets or short-term securities. I think that that would more than compensate for any adjustments to the tax credit for prior years unrecovered costs or accumulated losses.

It would be interesting but unduly optimistic to learn from the Government the exact amount included in the Certificate of Taxes paid issued to the three oil companies under section 15.4 of the Petroleum Agreement.

Government Revenue

Now let us see what Guyana received in the same year from two sources – the National Budget and the Natural Resource Fund.

As noted in the Table above, the total Government revenue in 2021 was $351,544 Mn. of which 76% came from tax revenues and 24% from oil revenues. Some brief points of analysis.

Inclusive of tax credits, the oil companies netted in 2021 from their Guyana operations, a total of $393,191 Mn. while the Government earned a gross sum of $351,544 Mn.

Exclusive of tax credits, the three oil companies earned $314,553 Mn. from petroleum operations while the Government earned in Profit Share $74,479 Mn., a ratio of 4.22: 1.

The earnings of the three oil companies from petroleum operations were 3.7 times the earnings of the Government from those operations, inclusive of Royalties.

Part of the disparity in points 2 and 3 is attributable to the recovery of previous years expenses which have now been recovered in full. So much for all the talk about risks and the uncertainties associated with extended timelines. Those expenses were always magnified to justify the give away of the patrimony.

The 2016 Petroleum Agreement provides for a 50-50 split of net revenue, between the Government and the Oil Companies. The Consortium is entitled to 50% of Profit Oil and the Government to the remaining 50%. Yet, the Government’s share of Profit Oil is comparable to that of CNOOC which has a 25% interest in the Consortium!

It is unknown in recorded history where three companies of a single country accounted for more revenue than the entire Government of that country in any single year.

Conclusion

President Biden said that Exxon is making more money than God. I am not sure about God but what is true is that locally, Exxon and its two partners have made more money net, than their host country was able to earn gross.

Next week we will start reviewing the financials of each of the three companies. That will allow for a more detailed analysis of the income of each of those companies, including any unrecovered costs.