January 21, 2022

Businessman and Newspaper Publisher Mr. Glenn Lall has filed an action in the Guyana High Court challenging key provisions of the 2016 Petroleum Agreement between the Government of Guyana and Esso Exploration and Production Guyana Limited, CNOOC Petroleum Guyana Limited and HESS Guyana Exploration Limited. Mr. Lall, who has waged a crusade against the Agreement, and more recently has been campaigning for an increase from 2% to 50% in the royalty paid on production, is asking the Court to declare a number of the provisions of Article 15 (the Taxation Article), including the following, to be unlawful, null, void and of no legal effect:

- Those granting tax concessions to Affiliated Companies of Esso, Hess and CNOOC.

- Those granting tax concessions to Sub-Contractors of Esso, Hess and CNOOC.

- The one granting exemption from personal income tax the income earned by expatriate employees of Contractor, Affiliated Companies or Non-Resident Sub-Contractors who are in Guyana for one hundred eighty-three (183) days or less in any tax year. Lall is also claiming that such exemption violates the Constitution of Guyana and the Prevention of Discrimination Act.

- The provision of the Agreement requiring the Minister responsible for Petroleum to pay the taxes of the oil companies.

- The section 51 of the Petroleum Exploration and Production Act powers to grant the concessions that the Agreement confers.

- The Petroleum Exploration and Production Act is not a tax Act and any tax waivers, concessions and remissions would run afoul of the Financial Administration [and Audit] Act.

Mr. Lall is also asking the Court to declare as unlawful Order 10 of 2016 which sought to ratify the concessions granted under the Petroleum Agreement. Through his lawyer Mr. Mohamed Ali, Lall is arguing alternatively, that even if the Order is valid, it only applies to holders of licences under a Production Sharing Agreement.

The respondent in the matter is the Attorney General although it is likely that the three oil companies will apply to be joined in the action. The current Government of Guyana which inherited the Agreement from its predecessor has publicly defended the Agreement on the grounds of sanctity of contract. That principle is now being challenged by a more fundamental one: legality, and in one issue, constitutionality.

This case is only about the tax provisions in the Agreement – not the Agreement as a whole. The basic structure of the Agreement will not be affected even if the Application is successful. Given the centrality of the tax provisions to the Agreement as a whole however, if the Application succeeds, every player in the Agreement – the Government, the oil companies, the sub-contractors and expatriates – will be affected, although the precise dollar impact is indeterminable and the variables too numerous to identify.

Identified below are some of the direct consequences.

Affiliated Companies and sub-contractors will be directly affected by the following three provisions:

- Payments to them during the exploration phase for contract work will now attract the 10% withholding tax under section 10 B of the Corporation Tax Act. Since the withholding is creditable against the eventual liability for that year, the consequence is temporal.

- Withholding tax under the Income tax which is now exempt will now become payable on interest, dividends, deemed dividends, remittances of actual and deemed profits.

- Income earned during the exploration phase by Affiliated Companies and sub-contractors who are in Guyana for less than 183 days in any tax year which is now exempt from tax will become taxable.

Expatriates

Expatriate employees of the oil companies, their Affiliated Companies and of Non-Resident Sub-Contractors who are physically present in Guyana for one hundred eighty-three (183) days or less in any tax year whose income is now exempt from tax will become taxable.

The Oil Companies

Apart from facing higher costs from Sub-Contractors, the Oil Companies become subject to:

- Withholding tax under the Income Tax Act becomes payable on interest, dividends, deemed dividends, remittances of actual and deemed profits.

- Perhaps most significantly, they will also have to bear the taxes payable by them on their share of Profit Oil.

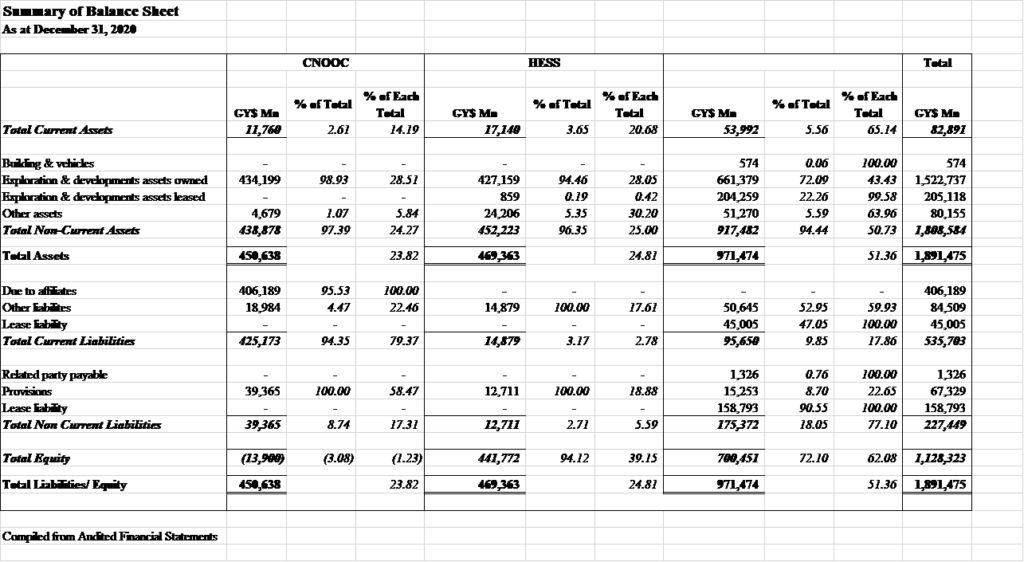

This is hugely consequential both for the oil companies and the Government. In 2020, Esso reported a loss while its two partners Hess and CNOOC reported total profits of $16,175 million. At the standard applicable rate of corporation tax, and without any tax adjustments for timing differences or losses, those two companies alone would have to pay approximately $4,000 million and a further 20% on branch withholding tax on their after-tax profit, less any amount re-invested. To put it another way, if instead of having the Government pay its taxes, the oil companies now have to pay taxes like the average taxpayer, they would be paying tax at the combined rate of as much as 40% of taxable income. Contrast this with the current regime under which the Government pays the taxes for the oil companies but issues to them a certificate that they have paid taxes in Guyana.

Conclusion

Should the Court rule that the tax Article is indeed unlawful, this would have a huge impact on the economics of the Agreement and result in significantly higher revenues to the country. We can expect the oil companies to fight to protect what then Leader of the Opposition Bharrat Jagdeo described in the NCM as a “contract that would harm us for decades into the future”, accusing the APNU+AFC as having “sold our patrimony”. Logically, the Government should see this case as offering some re-balancing of the Agreement in favour of the people. Its response this time would be particularly interesting.

Finally, the granting of the Application would affect the holders of all similar Agreements. They too will be watching carefully.