Thank you for visiting this blog. Register or Login now to contribute.

Articles, letters and other publications by Christopher Ram

March 22, 2024

Time for a fairer Compulsory Acquisition law

Introduction

As Guyana continues on its extensive infrastructural works to cope with a fast-growing economy, one area of law – compulsory acquisition of land – has been sidestepped and ignored, almost exclusively to the detriment of property owners. While the holding of property is a constitutionally protected right under the Guyana the Constitution, this country, in common with countries around the world, allows the Government, under strict conditions, to acquire private property. Under US jurisprudence, the concept is called “eminent domain.”

The insertion of the term “public purposes” in the name of our law may be designed to take the sting out of the appropriating citizens’ property, while seeming to promote national development and patriotism. In practice, the law invites and paves the way for a very imbalanced relationship between the Government and the citizen with the Government using the coercive force of the law against the timidity of all but the well-heeled in society. In fact, many people whose lands are acquired are sufficiently intimidated by an army of officials and their entourage on being told what they will be paid, they just say yes. This then allows the Government to boast that it has consulted, praising those who are intimidated as patriotic and those who want adequate compensation as anti-progress and anti-development.

Yet, the very essence of how the Act maintains some of the more obnoxious features from ancient times is not only disturbing but would be considered unacceptable and appalling in any open democratic society. For example, the principle of market value which assumes a willing seller is a non-starter since the property owner is at least reluctant, while the so-called buyer is using statutory powers to get a deal. The owner hardly ever wants to sell, while the Government obtains title whether there is agreement or not. All for a sum that the “seller” will soon spend and go broke.

Guyana

The fact is that the Guyana Act is woefully deficient, having come down from more than one hundred years ago, with minimal amendments – some of it for the worse.Ironically, the only amendment for this century was railroaded to facilitate the gas-to-shore project. And let us not believe that this is a West Demerara problem. Land on the East Bank of Demerara is also at risk of being compulsorily acquired under the same project. Because our law firm represents two persons whose land is being taken away under this project and because one of the persons has taken legal action, I am unwilling to say anything much at this stage. What I can say is that it is ironic that a government that boasts about its working-class credentials is prepared to cheat many of its own supporters.

India

About ten years ago, India recognised the weaknesses in their similar legislation and passed a most progressive act – the Land Acquisition, Rehabilitation and Settlement Act. As a model, that Act is hard to beat and if the Guyana Government or the Opposition was truly alert, the Indian Act would be so useful as a model. Containing an extensive preamble as well as a statement of objects and reasons, the Act is designed to ensure a participative, informed and transparent process for land acquisition and appears to be a people-first enactment. Even as India anticipates industrialisation and the development of essential infrastructural facilities, the Act is intended to operate with the least disturbance to the owners of the land and affected families while providing just and fair compensation to affected families. In fact, the preamble regards those persons as partners in development, no worse off after the acquisition than they were before.

To start with, “public purpose” is comprehensively defined, so that government’s scope for intervention in acquisition is limited to defence and certain development projects only. The nonsense of running highways through residential communities as the Government is doing in Prashad Nagar just outside of Georgetown is hardly likely to be permitted under the India legislation.

Elaborate protection

The Act requires that the consent of at least 80% of the project affected families be obtained through a prior inform process while the urgency clause permitted under the Act is limited to projects for national defence, security purposes and rehabilitation and resettlement needs in the event of emergencies or national calamities only. The Act also provides a comprehensive compensation package for owners and affected persons, including a solatium and a scientific method for the calculation of the value of the property.

An important feature of the Act is the requirement for a Social Impact Assessment Study, its public hearing and appraisal by an Expert Group of independent persons. In a nod to the rural and agricultural communities, that value is augmented by a factor of two in rural areas. The Administrative machinery too is quite formidable with consultations and defined roles for the Panchayats, Municipalities and Districts involving the Collector, Administrator, Presiding Officer, Judges and of course the Courts. Despite or because of all these features, India has some of the most interesting cases on the subject that would be most helpful in any review of the law.

The problem for the people is that the Government seems happy with a loose, ancient and unfair framework that works against the people.

A royal storm

A letter by Professor Kenrick Hunte appearing in the press earlier this week generated a wave of conversation across the society. Essentially, the Professor claimed that Guyana has been receiving Royalty of about a quarter of the 2% to which it is entitled under the 2016 Petroleum Agreement. Rather unusually, Mr. Elson Low of the PNC -R, Dominic Gaskin, former member of the Coalition Cabinet f the AFC and Vice President Jagdeo found common ground in rejecting Hunte. Low grounded his view on official pronouncements from the Ministry of Finance and Bank of Guyana reports, claiming that the number of lifts – the division point for sharing profit oil – being commensurate with a 2% royalty and not 0.5%. Gaskin, who was one of Granger’s Quintet + 1 on oil and gas, was positive that “there’s a perfectly logical explanation for these seemingly contradictory figures”, referring to Hunte’s and the Government’s.

The Vice President was even more expansive. His words are too precious and ordained to invite reported speech, or a summary. This is how he rebutted Hunte. “Royalty is calculated on production minus, so total crude production minus the crude used in the operations for transport and on the FPSOs (Floating Production Storage and Offloading vessels). In Guyana’s case, the FPSOs are operated by gas, so there is no deduction whatsoever, so royalty is calculated on the basis of total production and total sales. There is no deduction whatsoever. Every month, they have to confirm what the average price would be, the weighted average, and the [government] gives approval for that”.

Clearly, he does not know what the government does, if anything in relation to royalty, or indeed to anything else.

It does not appear that the VP has ever bothered to read the 2016 Agreement, let alone its reference to the Petroleum Exploration and Production Act and its definition of “petroleum”. In fact, the very first item in the definition of “petroleum” is this: “any naturally occurring hydrocarbons, whether in a gaseous liquid or solid-state”. Does the country’s petroleum czar not know that billions are charged to operations annually for supplies to the oil companies by at least one oil distributor? His answer was not only completely wrong, but shockingly misinformed, misleading and a total misrepresentation of reality. If this is Jagdeo’s knowledge of the petroleum sector, then President Ali has to step in, lest things get worse than they are.

Now back to Hunte.

His professorial approach with its mathematical formula involving Sugar and Timber Exports and a mystique of equations was probably beyond the level of quite a few Guyanese and may have led to the sensationalizing in some quarters. I took a different route and did find numbers that require real explanations, in the absence of which Hunte’s findings rather than his methodology have to be taken seriously. Here is what the Agreement prescribes about “royalties”.

‘The Contractor shall pay, at the Government’s election either in cash based on the value of the relevant Petroleum as calculated pursuant to Article 13 or in kind, a royalty of two percent (2%) of all Petroleum produced and sold, less the quantities of Petroleum used for fuel or transportation in Petroleum Operations, from all production licenses subject to this Agreement.”

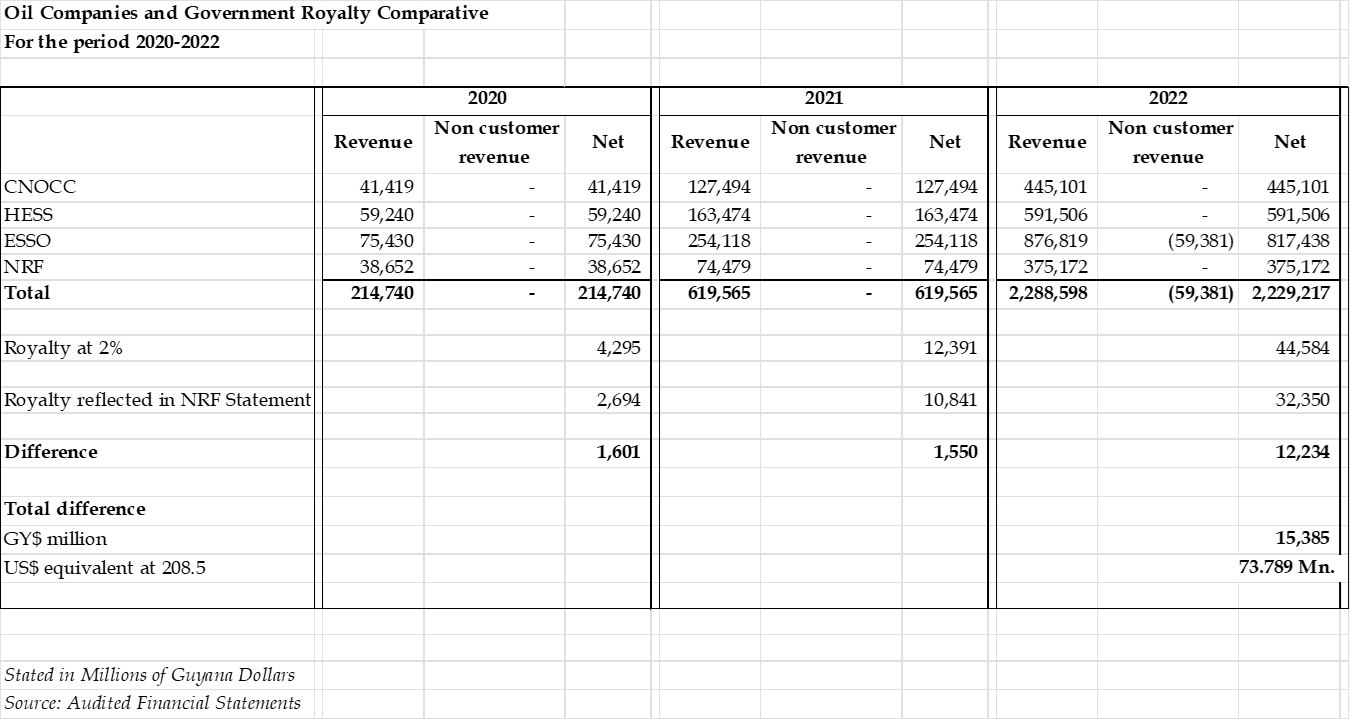

Even the most diligent journalist or forensic investigator cannot compute the royalty payable to Government in the absence of the cost of Petroleum used for fuel or transportation in Petroleum Operations. There is no real solace in the fact that the effect on royalty is 2% of that total. The other problem is that we will not know the value of petroleum sold by Exxon, Hess and CNOOC until their 2023 numbers are released in the form of audited financial statements within the next couple of months. To reduce the margin of error therefore, I have used just 2022 data from the financial statements of the three companies, plus the proceeds from sale of Government share of profit oil and apply to that total, a 2% for royalty.

The results of that exercise are represented in the Table below showing the Oil Companies’ Revenue and Royalty due and received by the Government over the three years 2020-2022.

What is apparent is that there is indeed some US$73.8 Mn. of royalties unaccounted for and one can speculate whether this is all to do with the implausible absence of the cost of fuel used in production or transportation, or in the difference in the accounting methodology used – accrual in the case of the oil companies and cash basis in the case of the NRF. Yes, the numbers are lower than Hunte’s, but he extrapolated to the end of 2023 when production, and therefore royalty soared. His numbers ought not to be discounted or dismissed.

Conclusion

I repeat again, unless President Ali puts a Petroleum Commission in place, Guyana’s incompetence in oil and gas will continue to be exploited at the national expense. He has to act in the national interest rather than as if he is afraid of or beholden to Jagdeo. We must not forget as well that hundreds of thousands of US Dollars were spent on an audit. Did their report, which is shrouded in mystery and secrecy, touch on royalty and profit oil? Only a Petroleum Commission can save us from this tragic farce.

March 8, 2024

A Table of a Chart and a Graph

Introduction

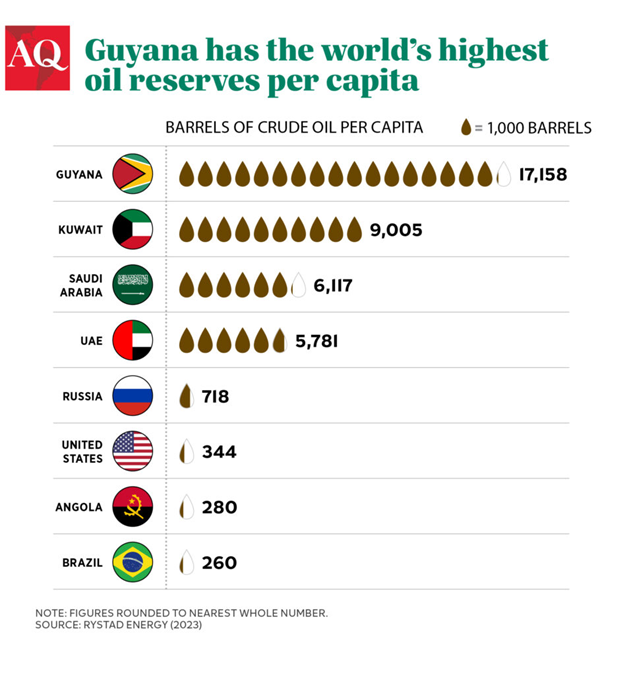

Today I will deliberately use the Chinese aphorism that “a picture is worth a thousand words” with great effect. So, with two pictures, we start with two thousand words which takes me over my word limit. Some weeks ago, the Government announced that two historic cricket grounds and green spaces in Georgetown are being handed over to its Middle Eastern friends from Qatar and their exclusive clientele for the paltry sum of $2 Bn, or less than US$10 Mn! Forget for a moment that the President and Vice President seem incapable of distinguishing between the State and the Government, or that selling in the absence of a robust valuation was their alleged ground for wanting to jail former Finance Minister Winston Jordan.

As dessert, VP Jagdeo, who is no stranger to tax holidays, indicated that the Qataris will have a 10-year tax holiday! We recall that about fifteen years ago, Jagdeo publicly insulted the late Yesu Persaud for being ignorant of the tax laws when the icon asked for equality and equity of tax concessions. Yet, any ignorance was on the part of Mr. Jagdeo who had extended concessions to his friend Dr. Bobby Ramroop, which the law did not allow. Mr Jagdeo showed no embarrassment or contrition over his error but rushed to change the law to accommodate Dr. Ramroop.

The wealthy poor

Let us look at the two charts. The first is by energy consultants Rystad Energy (which is duly acknowledged) showing that Guyana now has the highest per capita petroleum of any country in the world. And by far. Even if we estimate the population to be 800,000, it means that each Guyanese has a claim to 16,250 barrels of oil, the value of which at roughly US$80 per barrel, means that every man, woman and child is worth about US#1.3 Mn! For the moment, let us forget that Exxon and the Government are concealing several additional billions of barrels from Guyanese. Of course, these are gross values from which expenses have to be deducted, as they are for every other country on the chart. By any measure, however, that is a lot of money.

Sadly, these numbers seem to mean nothing to this Administration or to suggest to them that there ought to be a better revenue sharing between Guyana and the oil companies. Nor does It stir them that Guyanese are still queuing for freeness, teachers have to strike for better pay, and the working struggle to make ends meet even as the oil companies take a disproportionate share of the patrimony of the people and their officials live a life that would make the British Raj envious.

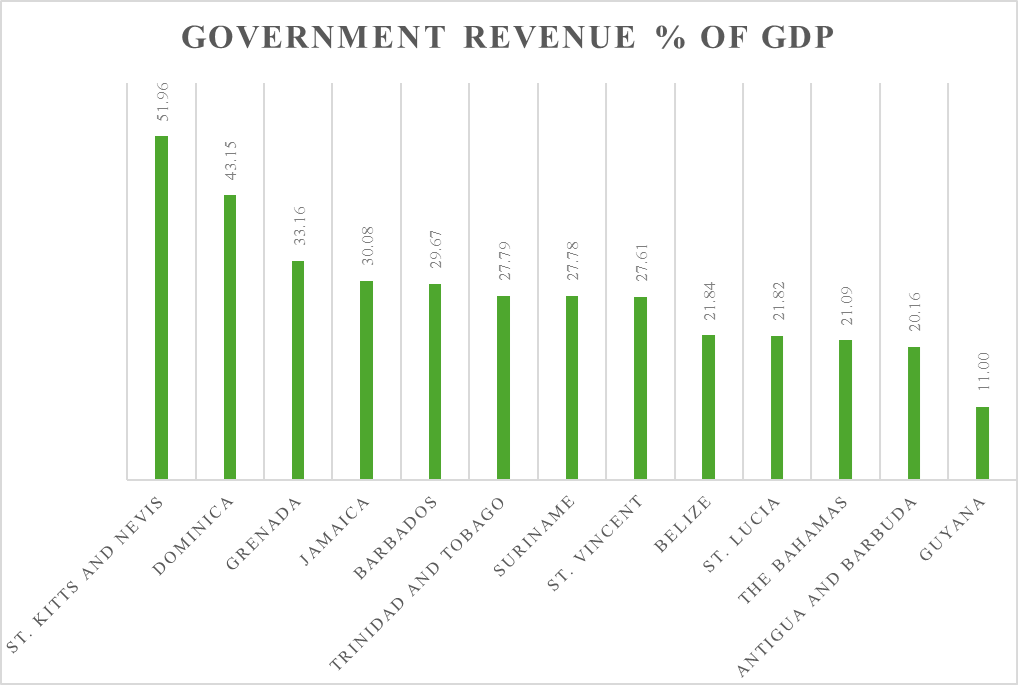

Tax to GDP ratio

Now for the second graph. It shows the tax collected by the central Government relative to the gross domestic product of the country. By this measure, Guyana has the lowest tax to GDP ratio across the entire Commonwealth Caribbean countries. It further tells us is that Guyana collects even less tax as a proportion of GDP than the near-tax free countries of the Caribbean. Guyana’s ratio is about a quarter of Dominica’s, a third of Grenada’s, and about half of Antigua and Barbuda’s, its nearest comparator.

Source: International Monetary Fund Website. All percentages are stated for 2022 except for Guyana which is stated for 2023.

It is difficult to accept that Guyana’s economic managers can believe that oil revenues displace the need for taxation and that we can go handing out tax concessions to any friend or flatterer. That is the President’s chosen role in the economy. He gave away huge tax concessions to the CPL cricket extravaganza – outside of the law – and continues to do so whenever he brings regional artistes to entertain the masses.

But the VP will not be outshone. He has taken it upon himself not only to give away state land without any consideration of its implications for the national interest but also tax holidays to persons who have neither applied for nor are entitled to them. The Income Tax (In Aid of Industry) Act is clear – it must be for “new economic activity of a developmental and risk-bearing nature”. It seems that neither the Vice-President nor the President has any respect for the laws or resources of the country, or the intelligence of its people.

Guyana recently entered into a Double Taxation Treaty with the United Arab Emirates that is all one-sided. That has not even made the news. But now, completely outside of a treaty, the Qataris enjoy exceptionally cheap land, irreplaceable resources, no taxes and the red carpet. This cannot be rational, responsible or reasonable. It is more like recklessness and drunkenness with power. Or is it the resource curse?

Dear Editor,

It is commendable that Banks DIH Limited has responded, in a full-page ad, to my recent commentaries on the company. Unfortunately, the membership, readership and the company’s reputation would have been better served by less obfuscation, diversion, distortion and ad hominem attacks. Let me state categorically that while it might be a fear, it is certainly not a fact that I have ever been an advisor to the Guyana Securities Council. The allegation was mischievous and false.

Let me state again and, hopefully for the last time, that Banks’ Chairman has personal knowledge of blandishments and carrots offered to me some years ago when I challenged the Company’s short notice for an annual general meeting. My response was that a notice is a personal matter, and it was outside the powers of an individual shareholder to waive a statutory right of any other shareholder.

I will now briefly respond to the substantive major points enumerated in the full-page ad.

1. Re-routing transactions through Florida. The ad appears to convey the impression that the court legitimised this extensive series of transactions. The court did no such thing. The sole issue before the court was whether the payment of commissions of $562,123,894 between 2009 and 2016 arose outside of Guyana and therefore not subject to withholding tax. My contention then and now is that it is unnecessary, wasteful and unjustifiable for the ordering of products from the Netherlands to be routed through Florida. Nor is it credible that a supplier of decades standing “does not treat with [Banks DIH Ltd] in relation to financial matters,” as the company sworn in an affidavit. Banks DIH is not a pariah company nor is Guyana an AML-blacklisted country. My concern was evaded in a maze of obfuscation.

2. The new holding company. I questioned the decision to convert Banks DIH Limited into a private company. What the directors do not tell us is that the application for the “arrangement” was made to the Court ex parte, despite the fact that Banks has two regulators directly, and four regulators as a group. Yet, the company did not, from the public records, notify any regulator. Evading responsibility for this simplistic adventure, the ad states that “the decision was made pursuant to advice from BDO, accountants.”

The company boasts that the decision for the conversion had 99.9% support. Yet, shareholders engaged me privately complaining that they do not understand the nature of the transaction. When I suggested questions that could be asked of the directors, the response was “you know this place.”

3. Payment of dividends. My concerns were about the company’s dividend payout ratio which is among the lowest of public companies in Guyana and the Region, and about the transaction cost of paying a dividend of less than a dollar on small shareholdings. Here is an example. Say that the company pays an interim dividend of $0.45 per share to a non-resident person who owns one thousand shares. That is $450 from which withholding tax of 20% has to be deducted, converted to foreign currency, and the net paid over. That leaves the shareholder with less than two US Dollars. Again, evasion and obfuscation.

4. A share re-purchase agreement of December 2016. My question was the reason for paying more than the market price under a share repurchase agreement. That speaks for itself but like the company did then and again now, it evades the real issue and its only recourse is a personal attack and a veiled threat of reporting me to the Institute of Chartered Accountants of Guyana. What an undignified response.

In my Business and Economics Commentary column this coming Friday, I will be publishing an open letter to the Company’s Audit Committee Chairman of my concerns as the holder of 117,000 shares in the Company.

Christopher Ram

Dear Editor,

Two events usually attract misinformation, once known as propaganda. These are wars and strikes. In a war, each side pushes information to show that it is doing better than the enemies – in fatalities, losses and territory. In a strike, the employer understates the support for the strike while the workers’ representatives overstate that support and the moral imperatives of their cause. In similar vein, I have seen numbers cited by some closer to the facts, such as the Chief Education Officer and the leadership of the Teachers’ Union.

In the case and context of the current strike I went to sources I consider most objective, if not always very clear – the 2024 Estimates. From these, I could make some reasonable assumptions and deductions on the affordability of any increase. What I also found is that some of the numbers cited by some non-associated persons like Dr. Tara Singh were off the mark by quite significant margins. My overall finding is that the Government can pay much, much more than the 6.5% it has offered teachers.

I say this even as I concede that the Estimates are not the easiest of documents to read and that the reader has to plow through dozens and dozens of pages and make rough assumptions arising therefrom, including how the averages pan out. Here are some of those numbers. The provision in the 2024 Estimates shows an increase in the allocation for Wages and Salaries for teachers, exclusive of related overhead costs, of 25% over 2023. Of course, the number of teachers is also expected to increase, even after natural attrition. The crude average annual increase in the number of teachers over the past three completed years was approximately 9%. The projection for 2024 is 14% of which we can assume that the significant increase will come at the beginning of the new academic year in September. From this, we can deduce an increase in the effective number of teachers for the school year to be about 5%.

Let us then assume that the Government is unwilling to make this up via savings from part of the total capital budget or by way of supplementary appropriation, the 2024 Budget appears to allow a 20% increase to the teachers for 2024. Except for some related costs that are ad valorem, the other charges are already provided for in the approved Estimates.

The Government can afford this and the teachers deserve nothing less.

Christopher Ram