Introduction

Demerara Distillers Limited, a conglomerate group comprising several local and overseas companies with manufacturing, trading, banking and trust relationships in Guyana, the region, North America and Europe as well as a joint venture in India and associated companies in Guyana and Jamaica, will be holding its annual general meeting this coming Friday, April 27. When the shareholders meet at the company’s Diamond Complex on the East Bank of Demerara, they will consider, among other routine items, an impressive if not entirely informative annual report containing the financial statements of the parent as well as its subsidiaries.

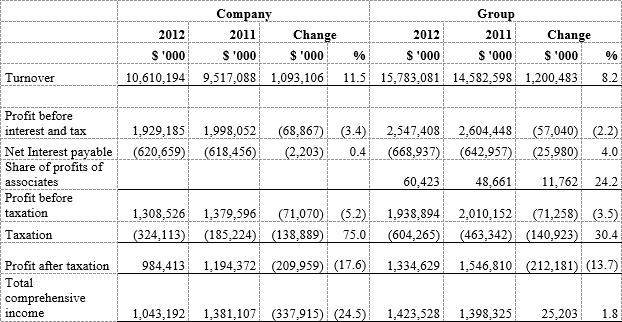

Measured by growth in turnover, it was not such a good year either for the parent (2.2% compared with 11.3% in 2010), or for the group as a whole (a more respectable 6.7% but less than 10.6% in 2010). Sales to subsidiaries represented 75% of total turnover of the company compared to 77% in the prior year.

In terms of after-tax profits, on the face of it the company and the group have done very well; the profits of the company increased by 68.7% while those of the group increased by a still substantial but smaller 35.7%.

Performance over the past nine years is illustrated by the following graph:

Source: Annual reports

No doubt encouraged by these results, the directors of the company are recommending an increase in the dividend per share from $0.45 to $0.48 – it would be good if the company could appreciate, like everyone else, that “cents” are no longer part of the currency of this country –which will cost the company some $23 million more than the $346 million paid out in 2010. Yet, for all of these, the Chairman in his report was less optimistic than usual, for reasons that only became apparent as the reader perused the financial statements and in particular their accompanying notes. Let us turn to some of those numbers.

According to the Chairman, there was an unspecified shortfall in bulk sales which carry a significantly lesser margin for which the higher value, higher margin-branded products should have more than compensated. An outsider looking in would think the company should welcome any situation whereby the higher margin products grow at a faster rate than the lower margin products. The emphasis on the sale of bulk products over branded products evident in year 2010 during which bulk sales increased by 45% while total sales increased by 10% seems quite counter-intuitive, if not illogical.

Domestic operations

While two of the four domestic operations made losses, those that were profitable produced some good results on a considerably smaller asset base. The standout failure is TOPCO, the juice company in which, despite the injection of hundreds of millions of dollars in capital expenditure, has managed to make losses in more years than it has operated profitably. One cannot help but notice too for TOPCO the almost identical language in 2010 being repeated in 2011, suggesting an inadequate level of attention in a competitive business environment. On the other hand, Distribution Services Limited, with a much smaller asset base, is reported to have enjoyed a10% growth in income and a 43% growth in after-tax profits.

Revenue from Guyana customers represents 65.4% of total group turnover compared to 62.5%, possibly reflecting the pressures faced in the international markets.

International operations

Not unlike the domestic operations, the inconsistently presented information for the overseas operations indicates that the international members of the group also had mixed fortunes. Total overseas sales fell by 1.6% despite growth in branded products of 10% reported by the Chairman.

In problem plagued Europe, turnover was down 6% and after-tax profits by 32%. In that region, a single customer generated 44.6% of total turnover from Europe compared to 50.0% in the prior year.

In DDL USA, no sales information is offered but after tax profit is reported to have grown from G$21 million in 2010 to $31.5 million in 2011. The shareholders of the parent company will recall that Demerara Rum Company of Canada was bought two years ago for $76.9 million. The company’s shareholders would certainly have liked to have had some particulars of that transaction as well as the parties behind the acquired company which handled bulk sales in Canada and must have had the confidence of the directors back home.

Interestingly enough, while the Canadian company was able to record an after-tax profit of $23.4 million in ten months, in 2010 it made only $8.9 million in 2011. It would certainly be interesting to learn how this was possible in the home of the company’s VP for International marketing, Mr Komal Samaroo. The company’s joint venture in Jamaica saw profits halved in 2011, but it was the Indian joint venture which ought to have caused the most concern among the company’s directors.

It seems certain that the existing joint venture in Demerara Distillers (Hyderabad) is heading the way of a number of other subsidiaries which the parent acquired and subsequently found unprofitable. Anyone following this column in the early nineties would remember the adventures of the first Indian operation which suddenly and without any explanation or information disappeared in 1993. Well, the directors having promised shareholders in the 2010 annual report that management would “make appropriate decisions to ensure an adequate return on [India] investments in 2011” now say, after another year of losses, that a “decision will be made in 2012 on the way forward.”

BEV Processors Inc

What does all of this mean? Except for an interesting transaction in which the company divested its BEV Processors Inc, the results of the company and the group would have been unimpressive. The profits reported include a non-recurring $288 million in dividends received prior to the sale of the investment, a reminder of a missed and costly lesson for Guyana’s taxpayers on whose behalf privatisation czar Winston Brassington sold the government’s 20% holding in GT&T without getting any of the year’s dividends, let alone accumulated profits.

The BEV transaction was particularly interesting in that the sale took place in early March 2011, but the dividend was not recorded in DDL’s books until the second half of 2011. Moreover, the 2010 annual report referred to the BEV shares sale in March 2011 without any mention of the substantial dividends the company received.

The June 2011 half year report published under the Securities Industry Act was used to help explain the revenue flow over the year. Turnover in the second half of the year represented 53% of the turnover for the entire year but produced exactly 50% of the gross profit and 60% of the profit before tax as a result of other income earned, representing 79% of the year‘s total. For the second half of 2011, finance cost was 52% and profit before and after tax 63% and 66% respectively, of the full year amounts.

But the income statements are interesting for other reasons too. Note 26 Related Parties discloses several transactions with group companies, only some of which I have been able to follow in the financial statements. Here are the major ones:

One might expect these to show up somewhere in the Income Statement; it is unclear where some of these items have been accounted for. In the interest of transparency, the company and its auditors TSD Lal & Co should be asked by some shareholder to explain these substantial transactions, before the GRA does. They should also be asked to provide information on which of the subsidiaries are audited and by whom, and which are not. It does not help shareholders and market confidence to have such uncertainties flowing from the financial statements of a public company, particularly one that is totally controlled by executive management.

Balance Sheet

Ever since this column began reviewing the company’s annual reports about two decades ago, two areas have stood out: inventories and loans. Because of the stable of products offered by the company, it is expected that inventories in the maturing process will be fairly significant while bearing in mind that inventories for accounting purposes must always be valued at the lower cost and market value, regardless of the accretion of the market value. The company had sales of $9.5 billion in 2011, the cost of which was $5.9 billion. In other words, the company has some 327 days of finished inventory on hand compared with 234 days in 2007.

Included in inventories as well is an amount of $1.165 billion of “spares, containers, goods-in-transit and miscellaneous stocks,” a category that always seemed to have been overstocked and out of balance with the finished stocks. It is good to see that that category seems to be falling significantly, both in absolute and relative terms. In 2007 the value of the inventories in that category was $1.8B or approximately 30% of total inventories.

The debt/equity ratio is a healthy 0.87:1 but the share of income before interest and taxes which goes to interest is around 25% and lenders to the company consistently receive a bigger share of the company’s earnings than its shareholders. In 2011 interest paid was $618 million ($371 million after tax assuming the lender is subject to a 40% tax rate) compared with dividends paid of $346 million with lenders investing less than half of shareholders’ equity.

Human resources

DDL has always prided itself as a good corporate citizen and is a major donor to the community through sports and education. In fact, two years ago the company established the DDL Foundation to “make a difference in the lives of deserving young people.” Internally too, the company has supported its employees with training, including the degree programmes at the University of Guyana. As the Chairman said, however, employee retention is a problem, a fact borne out by the turnover at management level in the company.

Of the nine members of the management team identified in the 2006 annual report, only two are still with the company, one of whom has moved up to the main board. Indeed, even at the board level there have been changes – some unavoidable – with only four of the nine directors in 2006 still on the company’s board of directors. Of the eight current directors, four are accountants including three serving in a non-independent executive capacity. The remaining one is a recent addition to the Board and serves as the Chairman of the Audit Committee.

Conclusion

This column has for years commented on the quality of the information provided in the Annual Report including an indication of those subsidiaries which have been audited and by whom. It is also not in keeping with modern trends to have only a Chairman’s report and not a CEO’s report, or a Management Discussion and Analysis which does not depend on the existence of the CEO.

Despite the improved earnings and earnings per share, the company’s share price is trading lower now ($10.7) than it did at the end of the half year ($11.0).