Comment

Co-incidences are rarely easy to explain. At the time of launching an award for the best Annual Report by any Guyanese company as one of the activities and initiatives for its 25th anniversary observed last year, this column carried a review of the financial statements of the two operating companies of the Banks DIH group: Banks DIH Limited (‘Banks’), the food and beverage giant, Citizens Bank Limited (‘Citizens’), a 51% owned retail bank and Caribanks Shipping Company Ltd, a dormant company.

This coming Tuesday – and regrettably belatedly – Ram & McRae will be announcing the winner of the award for the 2010 annual reports. That is as much as I am permitted to say at this time.

Introduction

Today’s Business Page looks at the financial statements of the two operating companies of the Banks DIH group. The group comprises Banks DIH Limited, the food and beverage giant, Citizens Bank Limited, a 51% owned retail bank, and Caribanks Shipping Company Ltd, a dormant company. Banks and Citizens are both public companies whose shares are traded on the Guyana Stock Exchange. The financial statements of the group also include as an associate company B&B Farms Inc, a Guyana private company, and BCL (Barbados) Limited in which Banks holds a 25% interest.

Both the public companies in the group have as their accounting year-ends September 30 and will be holding their annual general meetings later this week – Citizens on Tuesday 17 and Banks four days later.

The shareholdings in the two companies have changed little over the past year with Banks spreading just over 60% of its shareholdings among a vast network of private individuals while in the case of Citizens, four shareholders own 82% of the shares with the remainder spread among about seventy smaller shareholders. The Boards of Directors of both companies are chaired by Mr Clifford Reis, CCH, who is also the Managing Director of Banks.

In a Corporate Governance Code published last year, the Private Sector Commission boldly called for a clear division of responsibilities at the head of the company. The Code makes it mandatory that the positions of the Chairman and Chief Executive Officer (CEO) be held by separate persons. It also requires that the division of responsibilities between the Chairman and CEO be clearly established, be set out in writing, and be agreed by the Board.

Some observations

Another contrast between the parent and the banking subsidiary is evident in their annual reports; Banks’ high-quality, glossy report is designed and produced by Ross Advertising and printed by Scrip-J of Trinidad and Tobago while Citizens’ is on flatter type paper and produced by KRITI whose address is not stated.

There has been no change in the gender composition of both boards, each remaining steadfastly all-male, despite the constant chorus from progressive women like Stella Ramsaroop and Andaiye for more recognition to be given to women in Guyana. What makes the situation even more remarkable is that both entities have a large number of women staff and in the case of Citizens, six of the seven principal officers are women!

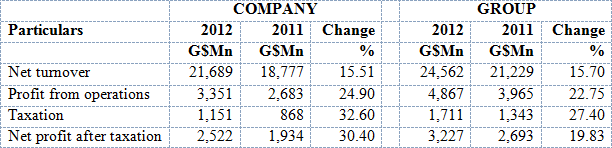

In any case, there can be no doubt that at both entities women make valuable contributions to the “exemplary growth in revenue and profit over that of previous years” reported by Chairman Reis in his report on the group. He had every reason to exude satisfaction: group profits from operations increased by 32% on a turnover increase of 16%. On the other hand, benefiting from the five per cent reduction in tax rates announced in the 2011 Budget, taxation increased by 10%, mainly from the banking subsidiary.

Banks DIH Limited

Source: Annual Report 2011

The company’s turnover (sales) increased by 15% from $16.3 billion to $18.8 billion, and its profit from operations increased by 27% while taxation at $868 million was a mere $4 million increase over 2010. As a result, net profit after taxation increased by 42%. Profit from operations as a percentage of sales which was 13% has increased to 14.3% while taxation as a percentage of net profit before tax decreased from 38.8% in 2010 to 30.9% in 2011.

Chairman Reis attributed the improved results to revenue garnered from the increase in physical sales, efficiencies derived from plant and machinery upgrades and an improved presell and distribution system. The performance was also attributed to capital expenditure of $3,142 million on major plant and machinery for the beverage, alcohol and water plants. The modern soft drinks plant which is expected to be put into use early in 2012 is expected to continue the trend of increasing productivity and profitability.

Growth

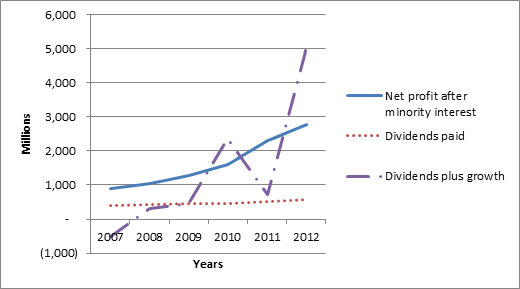

To get a clearer picture of how the profitability has changed one only has to go back to 2007 and 2008 when the profit before operations was 9.7% and 9.9% respectively, while the net tax effective rates in 2007 and in 2008 were 38.9% and 40.1%. Most impressively, two years after the company passed the $1 billion profit-after-tax mark, it is aiming to double that figure. Without taking anything away from the Guyana directors, it is perhaps more than merely coincidental that the company’s growth trajectory has been accelerated following the accidental partnership with Banks Barbados, aimed to repel an attempted take-over by Ansa McAl of Trinidad.

What is also significant is that the entire increase in the revenues of the company came not from exports but from domestic sources. Note 20 to the financial statements which gives a broad geographical breakdown of revenue, shows sales of goods and other services increasing by $2,478 million or 15% while revenue from exports actually declined by 24% to $233 million, down from $305 million.

Whether the company is satisfied with its domestic sales is not clear, but with the reputation of Guyana rum internationally, the company may wish to expand its horizons, a feature of the group since its launch in 1957, and indeed the theme for the 2011 report – the next level.

Source: Annual Report 2011

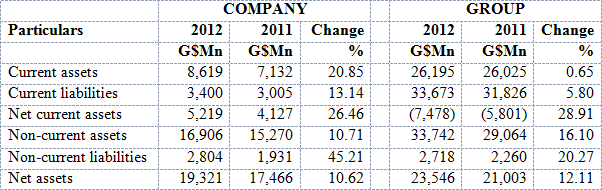

The balance sheet for the company and the group shows net assets increasing by $1,438 million and $2,149 million respectively. Payables and accruals included under current liabilities in the table above have increased from $1,538 million in 2010 to $2,625 million at September 30 last year.

Citizens Bank Limited

After a poor year in 2009 when the Bank had to make an impairment provision of $170 million for investments in Stanford International Bank and Clico Trinidad Limited – the region’s two financial catastrophes for that year – the results for 2010 were encouraging, while for 2011 they are impressive.

Profit after taxation in 2011 increased by 50.5% from $534 million to $804 million. Net Income for the year ended September 30, 2011 was $1,949 million compared to $1,469 million, an increase of 26.7%, double the increase in 2010 over 2009. Profit before Taxation was $1,279 million compared with $887 million in 2010, an increase of 44%.

Interest income increased by 32% and other income by 7.8% while operating expenses increased by 8.8%. Net Customers’ deposits had a significant 30.3% increase while interest expense increased by a more modest 8.5%.

Conclusion

The Banks Chairman was careful not to encourage too high expectations about the future. He avoided any comments about the future in the Banks DIH report while all the CEO of Citizens Bank was prepared to say – unhelpfully – was that 2012 “[would] bring both challenges and opportunities.”

It is my strong view, and indeed that of the Private Sector Commission, that companies need to enhance their communication with their members and the public. I noted a few weeks ago that Demerara Bank Limited had refused to release its 2011 annual report “until after their AGM.” I was met with a similar response when I sought a copy of the Citizens’ Bank Annual report. That is not a practice that should be encouraged by any institution, and certainly not one that has its sights firmly fixed on the next level.