Dear Editor,

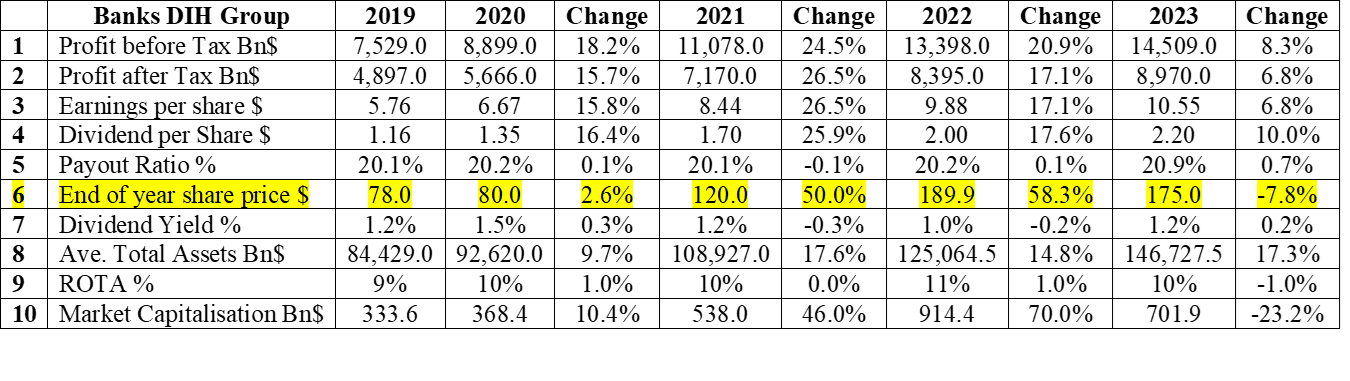

Pension Funds, Institutional and even small shareholders in Banks DIH Limited have been thrown into turmoil as a result of the arrogance and inexcusable insensivity of the directors of the company, the legacy of Guyana’s pioneering entrepreneur Peter D’Aguiar. For months, those shareholders and the public were confused by the decision of the directors to make the food and beverage giant into a private company, away from public scrutiny. To achieve this Machiavellian objective, shareholders of the company were expected to exchange their shares in the company for an equivalent number of shares in a newly established holding company, Banks DIH Holdings Inc.

Then followed a lawsuit brought by the two companies against the Guyana Securities Council – the Regulator of public companies – for its failure or refusal to delist the old operating company and list the new company as the public company. The Court rejected the application and ordered the companies to provide the Council with the information it required within a specified timeline and a deadline for a decision by the Council to respond to the companies.

Earlier reports in the press indicated that the Court ruled that the Securities Council was in its right to demand information on the transaction to enable the Council to make a proper decision. The date set out in the Court’s decision was 8 September 2024. There is no public information that the Council has given the companies its approval.

Yet, in surprise announcements in the national newspapers on Thursday and Friday of this week, the companies published two advertisements: one to shareholders and the other to “To whom it may concern” respectively. While the notices are confusing in their details, what is clear is that the directors have deemed the shares held by every holder of shares in the beverage company to be invalid, i.e., until a shareholder exchanges her/his current shares for new ones, those shares have no value. In other words, shareholders are deprived of their property which they thought the Guyana Constitution protects.

It is true that the views of the minority cannot prevail over a decision by the majority, but Company Law has made gigantic strides in the protection of minority shareholders, including a buyout of dissident shareholders. But I do find it hard to believe that the directors of both companies are so simple-minded to think that an exchange of an equal quantity of shares between companies carries an equivalent value. Think of it: even countries which engage in barter use value as the medium of exchange.

To confirm that frightening situation, the Guyana Stock Exchange, in a publication in the press of August 3 has suspended trading in Banks DIH shares with grave implications for all shareholders. I think it most unfortunate that the Guyana Securities did not respond publicly to the initial advertisement by the company which not only sought to preempt the decision of the Council but also seems to be in contempt of the Court’s ruling in the Council’s favour.

The decision by the two companies is irrational, abhorrent, unlawful, contemptuous and unconstitutional. Our country is replete with instances where persons refuse to act even when their interest is threatened. This is evidently such a case, and shareholders cannot let this pass.

In the more general to whom it may concern notice, emphasis seems to be placed on. She held interest or shares held on lean by institutions, requiring such institutions to return the share certificates to facilitate the issuance of the new shares.

It might have escaped attention that that was effectively backdating a deprivation of property guaranteed by the constitution of Guyana.

To add to the confusion, this Saturday’s edition of the Stabroek news, in addition to the republication of the general notification by the Company concerning shares held in in trust and on lien the Guyana Stock exchange Announced that in the circumstances of Banks DIH holdings Inc. issuing a newspaper notices to the effect that banks GIS Limited shares will no longer be valid effective July 19, 2024, stock exchange has suspended trading in BIH shares. It probably comes as no surprise to everyone, but to the directors and officers of BANKS DIH Limited, that the confusion brought about by the irrational decision whereby the beverage and hospitality giant is converted into private company whose shareholdings are transferred to a new hauling company.