Christopher Ram Responds to AG Nandlall’s unsubstantiated allegation

I recently viewed a video of Attorney General Anil Nandlall (AG) responding to a column written by Mr. Ralph Ramkarran, SC, who heads Cameron and Shepherd, arguably Guyana’s oldest law firm. I retained Mr. Kamal Ramkarran, the son of Ralph Ramkarran, as my attorney to challenge Article 160 (2) (a) of Guyana’s Constitution, which I believe permits individuals to contest parliamentary elections in geographical constituencies. Readers might recall that Kamal was also my Counsel — right up to the CCJ – in the case he successfully filed over the 2018 no-confidence motion in the National Assembly.

In the video, the AG made the grave allegation that Mr. Ramkarran Senior’s column was “an attempt by him to distance his law firm from a statement that I (AG) made… from a contention that I (AG) advanced.” The AG went on: “And the contention that I advanced was that based upon the information that I have received, information that I have no reason to doubt, the legal proceedings are being financed by a political presidential aspirant.”

After reviewing the video, I contacted the AG to inform him that his allegation about the financing of the proceedings was false and challenged him to provide us with the information or issue a retraction and apology. The AG subsequently issued what can only be described as a non-statement. Rather than providing evidence or retracting his defamatory claims, he now attempts to justify his conduct by claiming he was merely “sharing information already being publicly peddled” and that such information was “published on social media.”

His feeble justification raises even more serious concerns. If he is basing official statements on unverified social media posts and rumors, this speaks to a fundamental failure in his duties as the nation’s chief legal officer. Social media gossip and speculation do not constitute the reliable information he initially claimed to possess. It is profoundly disappointing that our nation’s chief legal officer would conduct himself in this reckless manner. His refusal to accept accountability when challenged sets a dangerous example that undermines the integrity of his office and erodes public confidence in our legal institutions.

I also take this opportunity to apologise to Ralph and Kamal Ramkarran and their families for the embarrassment and pain that the AG’s wild accusations and his subsequent refusal to retract them would have caused. The best vindication is honour, truth and justice. It will come their way.

The southern American expression “A hit dog will holler” was brought to Guyana in a coordinated response across the controlled media to my letter appearing last week under the caption `Presidency has been diminished by Mr Ali and he ought not to be re-elected’. Featuring media houses closely connected with the State and roleplaying by varying persona large and small, they have cast me in the memorable role of the Brave Little Tailor of “Seven at One Blow” fame, their combined failure allowing me to entertain the thought that Guyana has more unfeathered than feathered parrots, that we are one big soup kitchen. What emerges from their collective effort is not a defence of presidential conduct, but pseudo intellectualism and cowardly attacks from individuals whose supper depends on how often and how they mix up the pot.

Notably, not one respondent addressed the substantive issues I raised concerning President Ali’s conduct: concealing the expenses on Silica City, his vanity project; the documented WhatsApp evidence of a President engaging in communication on taxes; abandoning a public pledge to rebalance a most lopsided contract; the hidden Clyde & Company report; and the systematic undermining of constitutional and statutory bodies. Having documented numerous cases of tax concessions and benefits granted outside of the law, I can attest that such irregular practices are far from isolated incidents.

Most telling is President Ali’s refusal to establish a Commission of Inquiry to examine these matters – the one action that could definitively clear his name. And is there another way to describe a government that goes to court to challenge the award of a meagre pension equivalent to two hundred United States dollars per month to Zainul, a poor but dignified former carpenter while channeling hundreds of millions to friends and supporters than morally bankrupt and devoid of basic human decency?

To the first respondent, who refers to me as a friend, I am reminded of Caesar’s final words: “Et tu, Brute?” There is something particularly damning about betrayal couched in friendship’s language when all is done in the name of opportunism. Regarding questions about electoral preferences, my answer is simple: NOTA – None of the Above. When choices are between persons who are seriously compromised, including a president who has diminished my country’s highest office for party and supporters’ profits, the principled position is rejection.

To another, your transformation from closet critic to fervent defender illustrates how lucrative appointments alter perspectives -a la Martin Carter. To anyone who thinks that embracing facts is engaging in extremities, and who possesses that rare and unprecedented wisdom to equate a simple accountant with billionaire and liberal democrat George Soros, I say, thanks but no thanks. To them both, I say, some knives cut three ways – toward enemy, friend and, ultimately, oneself. Their blade has found all three targets.

As for those respondents vying for bit parts (extras in the film business), they constitute the “et al” of the government dependency support cast whose feeble attacks are unworthy of any response, or respectability. Among these is one who substitutes fantasy and creativity – embellished with racist undertones – for truth and accuracy, qualities identified with the fiction shelves in the library.

But they all have one thing in common. Their very existence depends on the electoral success of their party, are probably otherwise unemployable, and therefore deserve some understanding, but not respect.

I reserve my final words for the President himself. As a practicing Muslim, he knows that the Prophet (peace be upon him) declared that “a word of truth before a ruler” is among the highest forms of jihad. Hurtful they might be, they are the unblemished truth while his defenders swear that the emperor’s clothes are made of the finest silk when honest men, women and children can see that he stands naked.

In October 2024, President Irfaan Ali announced to the Parliament of Guyana that a payment of a one-off Cash Grant would be introduced for National Insurance Scheme (NIS) contributors and that the full details of this allocation will be revealed in the 2025 National Budget. The additional information – that the money would facilitate the payment of a one-off sum to persons who have made between 500 and 749 contributions was so unhelpful that accountants Ram & McRae commented in their flagship Budget Focus that such sparseness was “not only disappointing but thoughtless”.

Then on 10 April 2025, the Department of Public Information issued a statement that with the injection, “more than $10 billion in disposable income will be placed into the pockets of some 25,000 pensioners nationwide.” Displaying an incredible lack of understanding of how the NIS works, the President urged “eligible pensioners who are not on the NIS database to swiftly register at the various NIS branches to benefit from this programme.” As if that was not bad enough, the President added that “the payout could even begin this Friday after some $10 billion is transferred to the NIS.” The calendar shows that the first Friday after the announcement was 11 April, which made any immediate payment impossible.

Reminiscent of his mis/announcement of the general cash grant of $200,000 per household in October 2024, the President’s advisers seem to provide him with poorly thought-out information that embarrass him. The fact is that the NIS cash grant is as muddled as the wider grant and plays on the poverty, the hopes and the lives of pensioners. The reality is that no one with the possible exception of the President himself knows how the disbursement will be made – and certainly not to persons on the “NIS database”.

The poor NIS is placed in a bind. It has published on its website a document with limited information setting out as the conditions of eligibility that persons must have between 500 to 749 contributions on record; be 60 years or older as of 31 December 2024; and “MUST NOT (emphasis the NIS) be receiving and/or do not qualify for any pension from NIS”. It invites persons to insert their NIS number or their personal data to determine their eligibility.

We tested the system for three persons who were paid an NIS Old Age Grant. The system came back promptly: Record Not Eligible. This runaround will be worse than the general cash grant and is further support of the view of the Attorney General that this “solution is not a solution.” See chrisram.net on 15 May 2025.

I anticipated the problem and wrote a WhatsApp message to the President on 21 April offering a solution. He is yet to respond while the confusion continues.

Anong the suggestions were:

Calculating payments as a percentage of what contributors would have received with full contributions, based on their last insurable earnings. For example, a contributor with 500 contributions would receive 500/750 of their potential pension for life. This maintains the core principle that benefits should reflect contribution history and earnings.

Amending the NIS Benefit Regulation to make the payment a permanent feature, thus avoiding the recurrence of the problem and the accompanying dissatisfaction.

I advised the President that the recommended approach is implementable within a similar fiscal framework while offering a more equitable distribution. As he is entitled to do, the President never responded to my message and the system is a total mess. The responses to my inquiries using real particulars suggest that the benefit applies to 2024 Old Age grants only. Not next year, not last year. So here is the rub. Using the most recent available NIS Annual Report, the one-off Cash Grant will cost approximately $750 million dollars, about 7.5% of the $10 Bn.

This raises questions about the seriousness of the entire process and the people involved. On this, the NIS is without blame. President Ali never consulted or instructed the Board. So was the Budget Office and the Ministry of Finance to negligent, so reckless, to just plug $10 Bn simply because the President told them to? And was the famous Cabinet asleep or too coward to ask any question when it gave the Minister approval to present the Budget with that big, beautiful sum included? Is there now no one, not even the Budget Office that we can trust with managing public money? Is this the resource curse in action? Will anyone listen, let alone answer?

There is precedent of Ali reversing himself on a cash grant. Then we can make something good out of this mess by establishing some proper solution, withdraw the appeal against the Zainul decision and show how much we care for our elderly. The money has already been voted on and is available. It can be put to good and constructive use.

Every Man, Woman and Child in Guyana Must Become Oil-Minded – Column 161 – 12 June 2024

Confusion over Oil profit

Last year, my summary column discussing the 2023 audited financial reports of Stabroek Block contractors had the caption “Oil companies have earned five times more from oil than Guyana. Modest investment, gargantuan returns.” If anything has changed, the money deluge has continued to flow upward and faster in the direction of those contractors. But before we look at those incredible numbers, maybe a word about Vice President Jagdeo’s exchange with a reporter of relevance to today’s column might be revealing.

Reporter to Jagdeo. “Can you explain Exxon and its partners reporting that their profits for 2024 being 10 billion US dollars, but Guyana only got 2.6 billion, despite it being a 50-50 profit sharing”.

Jagdeo’s response: “So I saw something about Exxon reporting a trillion dollars in profit over the three years and they said that the government got about 1.3 trillion dollars. So that’s about consistent with the formula which says that 14.5 percent of the 25 percent which is set out for as profit sharing would result in that configuration and they would have 10.5. So that’s consistent from what I saw. It can’t be any different.

“In these years they have to get less profits than we have received because of that formula. They have spoken about paying back the capital, which is a different matter about paying back the capital invested which comes out of the 75 percent of revenue allocated for that purpose. So, we can’t conflate the two.

“They’re very different and it’s consistent with the formula. And just to tell you that to give you an indication if they say 1.3 trillion dollars we got since the beginning of oil that’s less than this year’s budget. One year budget but that’s what we got from the beginning.

So that conforms what we have been saying because we passed five budgets so far. So entirely clear.”

The Vice President’s shutting down the question with the words “So entirely clear” suggests that he was confused by his own garbled logic for all the world to see. For Guyanese, it was embarrassing to see the Vice President with responsibility for the dominant petroleum sector display such a poor knowledge and understanding of the Petroleum Agreement which has been around in its present form for nine years, and in its earlier form for twenty-six years. What makes it regrettable is that his response – because of its egregiously flawed answer, might unfortunately be seen and used by the oil companies as a validation of the accounting methodology, content and form when it really is just the opposite. For readers’ benefit let us recap the correct formula for the allocation of profits between the Government as a one-half party and the oil companies as a collective, as the other.

Profit is arrived at taking after a) the payment of a royalty of 2% of all petroleum produced and sold, net of deduction of quantity used for fuel and transportation; and b) deduction of recoverable cost up to a maximum of 75% of total revenue. By an amendment to the Agreement, the government and the oil companies agreed that “royalties” are not a recoverable expense charged to the operations so that much is set aside for the government. The balance is shared between the Government and the Contractor for each Field in the following proportions: Contractor fifty percent (50%) and Minister fifty percent (50%).”

Applying the formula (100% – [2% + 75%]) ÷ 2 = 11.5% – the government receives a minimum of 13.5% (2% royalty plus 50% of profit) and the oil companies get 11.5%. Jagdeo’s 14.5 % and 10.5% are wrong. He also advances the novel proposition that there is a 75% allocation for the payback of capital invested. That too is incorrect. It is a cap on recoverable expenses for any year, whether for capital or operating expenses. And then he throws in the dead herring about Guyana’s share of profit oil without acknowledging that the government pays the taxes of the oil companies for which they are issued a Certificate of Taxes paid by someone or the other.

Back to the numbers

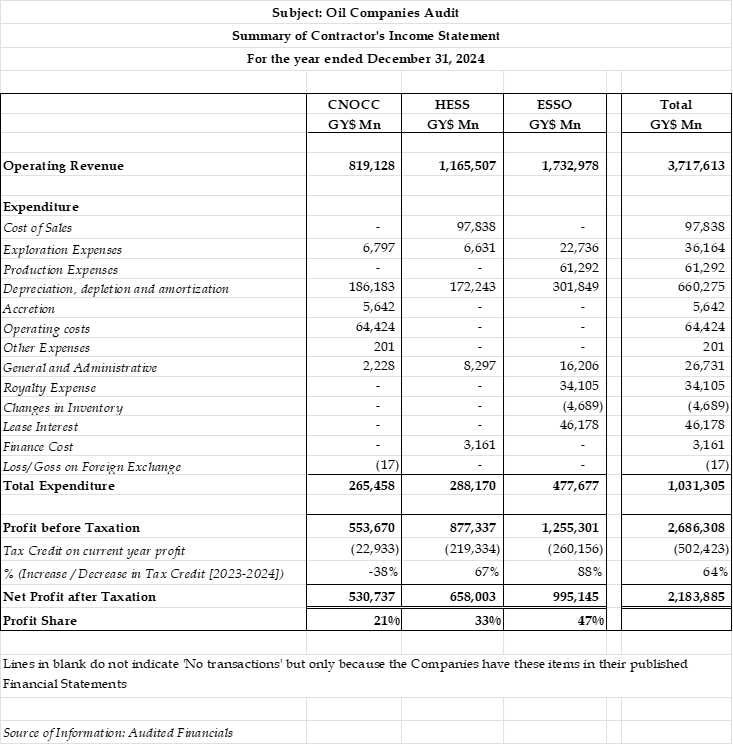

Table 1.

Source: Audited financial statements

The Table is constructed from the audited financial statements of the three companies for 2024. The total profit before the mythical tax for the three companies amounted to G$2,686,308 Mn of which Exxon’s share is 47% (2023 – 46%), Hess at G$526,236 Mn. or 33% (2023 – 32%) and CNOOC of 21% (2023 – 22%). These numbers are consistent with 2023. Readers can turn to Columns 157 – 159 for a review and commentary on the 2024 financial statements of each of the three oil companies, including both their income statement and balance sheet.

Having commented in the past years about the lack of comparability of the financial statements, I am amazed that the auditors appointed by the Government at a considerable cost, never seem to have recognised this self-evident fact. Because of what is stated in the introduction, this should surprise no one.

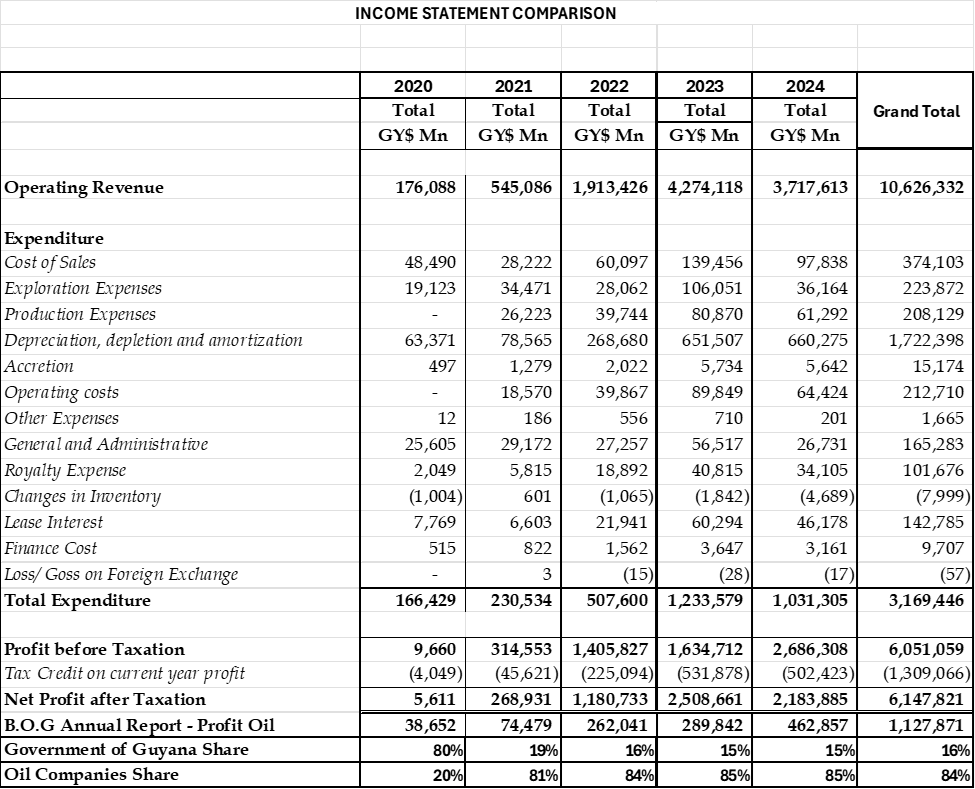

Before any discussion on these 2024 results, I share with readers the profits earned by the oil companies from 2020 – 2024, compared with the returns to the Government over the same period.

Table 2: Cumulative numbers

In Column 162 to be published next Friday, we will have a general discussion on these Tables.

Every Man, Woman and Child in Guyana Must Become Oil-Minded – Column 160 – 10 June 2025

Introduction

Today’s column addresses the audited financial statements of CNOOC Petroleum Guyana Limited, the third-ranking partner with a 25% interest in the Stabroek Block operating under the 2016 Petroleum Agreement. Like Exxon and Hess, CNOOC is also a branch of an external company, in this case, incorporated under the Companies Act of Barbados. Unlike Exxon and Hess, CNOOC maintains a very low profile in Guyana, leaving the heavy PR lifting to Exxon, the designated Operator under the Agreement. Its ultimate parent company is the China Offshore Oil Corporation, established in the People’s Republic of China (PRC).

But CNOOC’s annual report is not another corporate success story wrapped in glossy annual reports and feel-good community photos. This is cold, hard evidence of a foreign state-owned enterprise that systematically extracts wealth from non-renewal Guyanese resources while operating under the same controversial 2016 Petroleum Agreement that continues to benefit foreign businesses over the national interest.

Like its co-venturers, CNOOC shares in the 2024 bonanza, its income statement revealing profits that would make any multinational corporation green with envy, sweetened through a tax arrangement under which its taxes are paid by the Government of Guyana.

Financial Statements

The rest of this column examines the financial statements of the company’s participating interest in the Stabroek Block. All information sourced from the Branch’s financial statements.

Revenue

The company’s revenue for 2024 reached G$819.1 million – a 59.4% increase over 2023. That figure includes $22.9 Mn which the company describes as “Deferred income tax expense”, presumably the amount which the Government will pay on its behalf under Article 15.4 of the Agreement. The notes to the financial statements disclose that all the oil from its share of the operations is sold to China Offshore Oil (Singapore) International Pte Ltd, a member of its group.

While total expenses for 2024 amounted to G$265.5 million, up 68% from 2023, the largest portion was not actual cash expenditure but a book transaction following accounting convention. The largest single expense is Depreciation, depletion, and amortization of G$186.2 million, representing 70.1% of total expenses – in other words, more than twice as much all other expenses combined. Operating costs was G$64.4 million, or 7.9% of revenue, revealing the Stabroek operation’s efficiency: once wells are drilled and production units installed, the cost of extracting each additional barrel is minimal.

After all expenses and the Deferred Tax Expense, the company recorded net income of G$530.7 million – a 66.5% increase from 2023. Expressed another way, the net profit margin is a massive 64.8%.

The Balance Sheet

Total assets increased during the year by 28.9% to G$1.55 billion, or 28.9%. Of this, property, plant and equipment accounts for G$1.548 billion, or 99.9% of total assets. The company’s balance sheet shows that it held just G$60 million in cash, to meet any eventuality which may arise. The balance sheet indicates that the amount due to Affiliates reducing by $136 Mn, of which the bulk was “Financing” of $107 Mn, and the remainder was “Investing”. These items need explanation since the oil companies have repeatedly stated that no interest is charged on the operations.

The liability side shows how the assets are financed – by credits, equity and retained earnings. Let us look at these. Credits have decreased from $323 Mn. to $191 Mn, or roughly 40%. Then there are the tax liability and Deferred income tax liability which makes up 18.3% of the total assets. The balance of $1,074.9 Mn, or 70% is financed by retained profits, and that is after the payment of $104.3 Mn dividends in 2024.

The shareholder’s equity is entirely made up of retained earnings of G$1,075 Mn. having grown by GYD $426.5 million in profit after dividend in 2024. This represents profits retained in the business to finance capital injection.

Conclusion

CNOOC may not have the flair of Exxon or the drama of HESS but in its own quiet and discreet way its performance matches its American counterparts in another bumper year with its hosts Guyana – or rather its leaders – mesmerised into paralysis and content to do nothing.