This Article was Published on July 9, 2021

Introduction

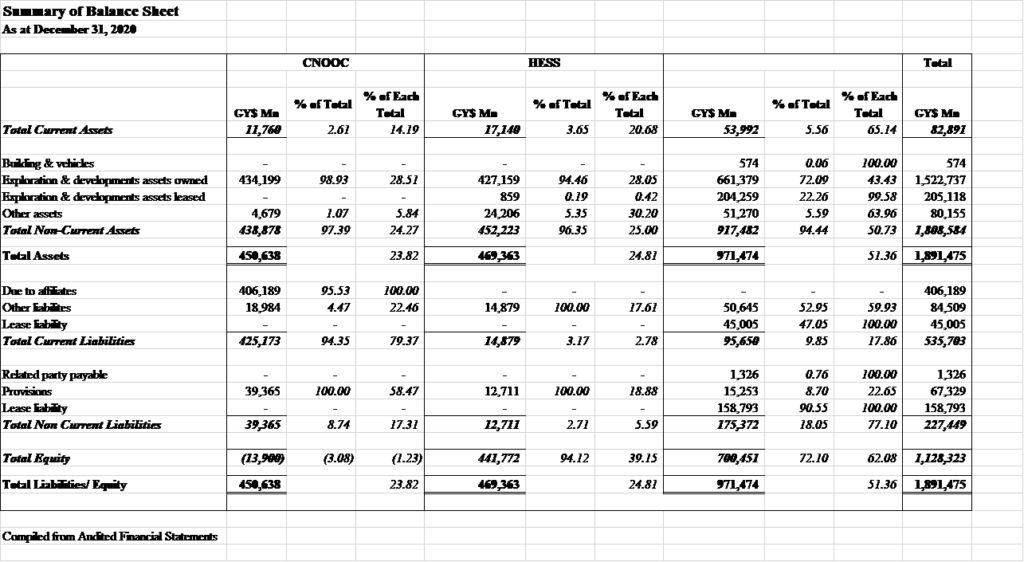

The issue of taxation of the oil companies has aroused particular interest ever since it became known that the Government has to find some $5.391 billion to pay the tax liability of the two partners of Esso in the Stabroek Block – CNOOC and Hess – which reported pre-tax profit of the equivalent of $16.175 billion in 2020. For reasons identified in column 90, Esso, the senior partner and Operator of the Stabroek Block, reported a loss to be carried forward for recoupment in future years. Despite the industry’s well-known proclivity for financial engineering and creative accounting, at some point, Esso too will report a profit and will demand that Guyana pay its taxes as well.

Guyanese are not unfamiliar with the gay abandon with which our governments hand out tax exemptions to the powerful, the favoured, and the influential – the latest group to be rewarded with such fortune are shareholders of private hospitals, some of which are known for extortionate charges and dangerously poor service. But what Guyanese find hard to accept is that an agreement can state, as the 2016 Agreement does, that an entity is subject to the income tax laws of Guyana, including the Corporation Tax Act, and yet two paragraphs later, imposes on the taxpayers the burden of paying those taxes. But that is exactly what the 2016 Agreement and similar agreements have done. And which the Fiscal Affairs Department of the IMF, in a 2018 Technical Assistance Report, in a peculiarly didactic style, both asks and answers the questions whether post-tax sharing is unique to Guyana, and whether it has advantages.

Noise and nonsense purveyors

The report’s authors – Thomas Baunsgaard, Honore Le Luche and Diego Mesa Puyo – are persons whose credentials cannot be summarily dismissed. At least two of them hold high office and would be the very opposite of noise and nonsense agents who according to our learned Professor “collude, connive and conspire to conceal the reality of today’s petroleum sector and pursues (sic) very outdated narratives.”

This column will examine what these distinguished and knowledgeable individuals wrote about “post tax sharing”, their description of the mechanism whereby the tax payable by the oil companies on their share of the profit under a production sharing agreement is paid by the Government out of its share. Here is their answer to their question about uniqueness and advantages:

“No, this system is used in many producing countries such as Trinidad and Tobago, Azerbaijan and Qatar, just to name a few. Some advantages of the pay-on-behalf-of system is that it provides more certainty on the expected government revenue from oil projects and mitigates tax planning, while offering physical stability for both the government and contractor against changes in corporate tax rates.”

This must rank as nonsensical a proposition as any that the IMF has published in its name for decades. How one might ask, does this giveaway bring certainty to Government revenue, or prevent tax planning, when the whole idea of pay-on-behalf-of (POB) is all about tax planning – to allow oil companies to receive a certificate issued by the tax authorities of a tax ostensibly but not actually paid by them so that they can claim a tax credit in their home country? And stability for Government? In fact, from all appearances, Budget 2021 does not acknowledge any awareness of this liability by the Government or make any provision for its payment. For the Government to meet this obligation to the oil companies outside of an Appropriation Act would be unlawful and may explain the silence of the authorities on this matter.

IMF examples

The practical examples given by the IMF Team are only marginally more sustainable than their conceptual logic. The authors are right about Trinidad and Tobago but fail to acknowledge that this is a decades-old legacy which is no longer widely practised, and has never applied in a post-discovery Agreement. With respect to Azerbaijan, the assertion is effectively disputed by one of that country’s academics and by Deloitte, a Big Four Accountancy Firm. In an article in the July 2015 edition of Journal of World Energy Law and Business, Nurlan Mustafayev states that Contractors and sub-contractors are subject to taxes under the country’s Production Sharing Agreements. There is no pre-contract cost, capital expenditure is limited to 50% of gross production and the cost recovery base and taxes are ring-fenced. Deloitte goes further and gives a range of tax rates of 20% to 32% which petroleum operations must pay. They both note that each Agreement is the subject of a separate Act of Parliament and neither mentions the Government of that country settling the oil companies’ tax obligations.

And for Qatar, here is how PWC, another of the Big Four accounting giants, sums up that country’s tax regimes in respect of petroleum operations: “Generally, corporate income tax rate at a minimum of 35% is applicable to companies carrying out petroleum operations…” In fact, Qatar has moved away from Exploration and Production Sharing Agreements (PSAs) to Development and Fiscal Agreements (DFAs).

The dangers of comparison

While comparisons can be useful benchmarks, they ignore the overall package and relevant local laws at their peril. In the case of Guyana, two such laws are particularly relevant: the Petroleum Exploration and Production Act Cap. 65:04 (PEPA) and the Financial Administration and Audit Act (FAA). Section 51 of the PEPA provides for the modification of four Acts in respect of licensees under a production sharing agreement. The Acts are the Income Tax Act, the Income Tax (In Aid of Industry) Act, the Corporation Tax Act and the Property Tax Act which extends to the Capital Gains Tax Act as well. In violation of section 10 of the PEPA which permits agreements not inconsistent with the Act, the minister went beyond his powers to extend concessions to persons who do not hold such licences, including persons not resident in or carrying on any operation or business in Guyana.

The Granger Administration which signed the 2016 Agreement, and the PPP/C Administrations before and after it, will have an enormous task of justifying whether and how a modification or inapplicability of a tax law can amount to a reversal of a statutory obligation whereby a tax liability payable to the State ends up with the Government paying that tax. The FAA in particular appears to raise an insurmountable hurdle. It requires any remission, concession or waiver to be expressly provided for in a tax Act or subsidiary legislation. Seems that the oil companies might have thought that the vaguely worded Order No. 10 of 2016 to give effect to the Petroleum Agreement would allow the pay-on-behalf-of trick. But the FAA deals with that as well. It provides that no Order (or other subsidiary legislation) will be valid unless the Act under which the subsidiary legislation is made expressly permits the remission, concession or waiver. The Order is made under the PEPA which does not, even by implication, let alone expressly, permit[s] the POB formula.

Conclusion It seems clear that the taxation Article of the Agreement contains several provisions which do not meet the test of “not inconsistent” with the Act. The Government must surely be aware of this. In the final analysis, it has to decide whether it stands on the side of the law or with Esso and its partners. The choice should be an easy one. But logic and the law never apply to politics in this country, even when it involves substantial revenues to the State.