STABROEK’S JUNIOR PARTNER CNOOC MAKES G$355.7 MN ON SHARE CAPITAL OF US200,000. YES, TWO HUNDRED THOUSAND US DOLLARS.

Introduction

Today’s column features the financial statements of the Chinese-owned CNOOC which holds a 25% working interest in the Stabroek Block, as a “non-operated joint venture partner”. CNOOC, like its other two partners, is a branch of a company incorporated outside of Guyana and traces its parent to the People’s Republic of China.

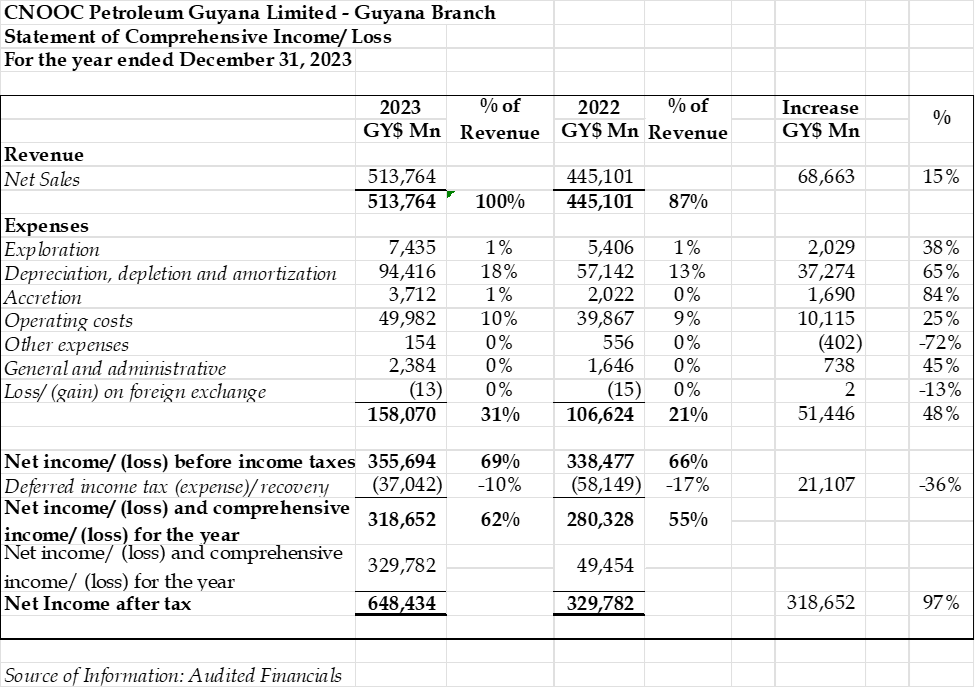

The Income Statement

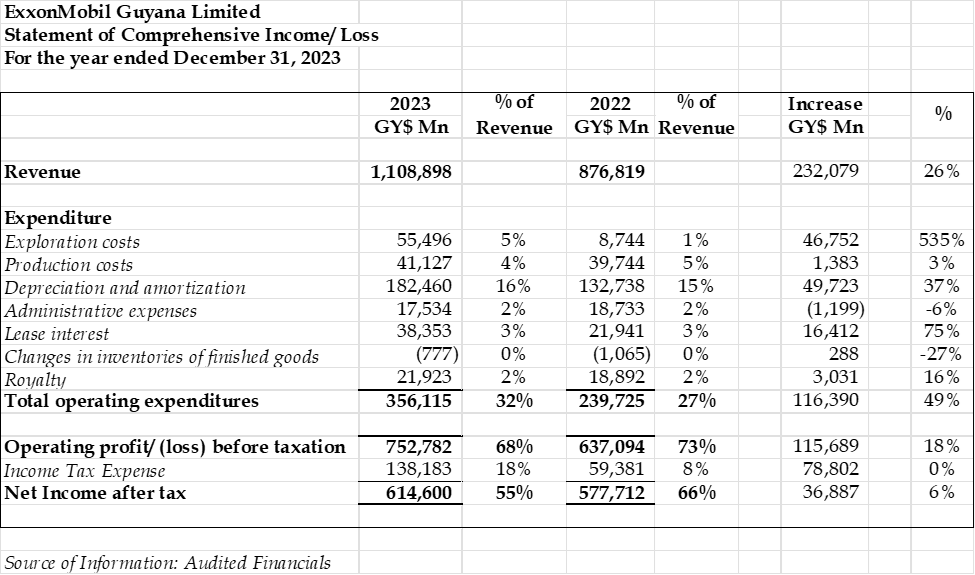

For the year 2023, the Branch reports net sales of $513 million, an increase of 15% over 2022, and net income before income taxes of $355,694 million, an increase of 5% over 2022.

Expenditure on exploration activities is shown at $7,435 million, an increase of 38% over 2022. Given the company’s status as a “non-operated joint venture partner,” it has to be assumed that that expenditure is merely a share of such expenditure of the entire project of which Exxon is the designated Operator. Operating costs of $49,982 million represent an increase of $10,115 million, or 25% more than 2022. Despite the significance of these amounts, there is no note or explanation of what these line items comprise. Depreciation, depletion and amortisation is reported as $94,416 million, an increase of $37,274 or 65%. This is a non-cash cost and represents 18% of revenue and 60% of total expenditure.

From the net income, there is a deduction of $37,042 million, described as Deferred income tax. Note 8 on Taxation explains that exploration and development costs are capitalised and written off over five years and that deferred tax asset as disclosed is in respect of tax losses, recognised only to the extent of future taxable profits. Of course, taxation for the three companies is a fiction since the Government pays the taxes for the companies. This is acknowledged by the same note and confirmed by the branch’s Cash Flow Statement which shows as an add-back the identical amount deducted in the income statement.

It does not appear that the branch transfers its net income for any year was transferred to the parent company. As a result, the after-tax profits are added to the opening net income of $329,782 million, bringing the total net income at the end of the year to $648,434 million, as shown in the Balance Sheet.

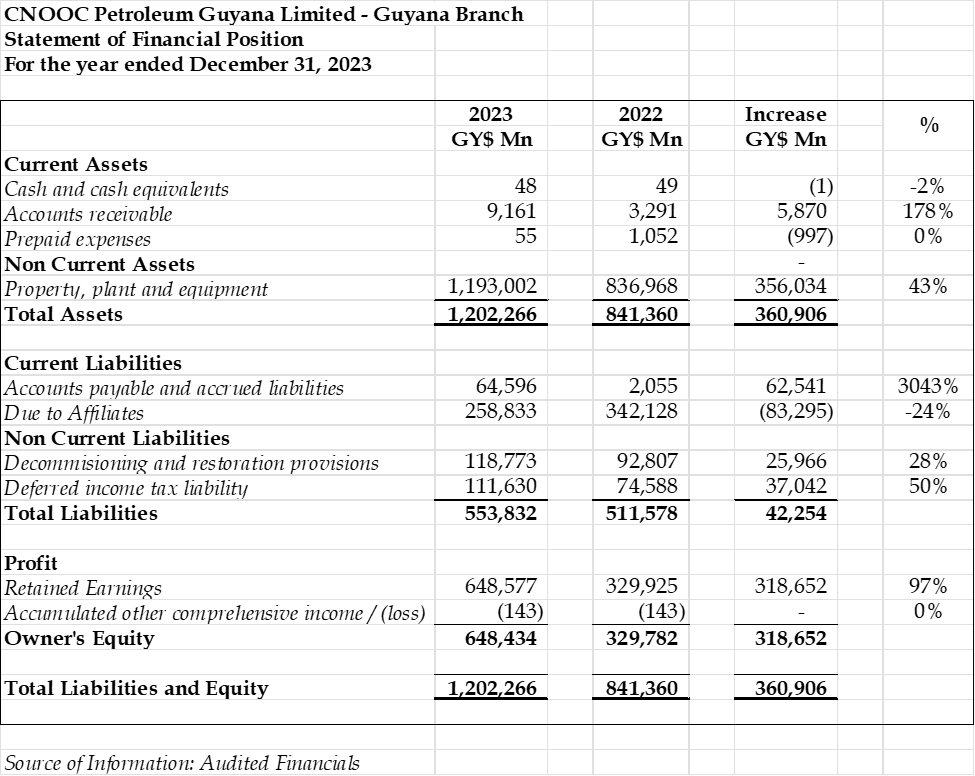

The Statement of Financial Position (Balance Sheet).

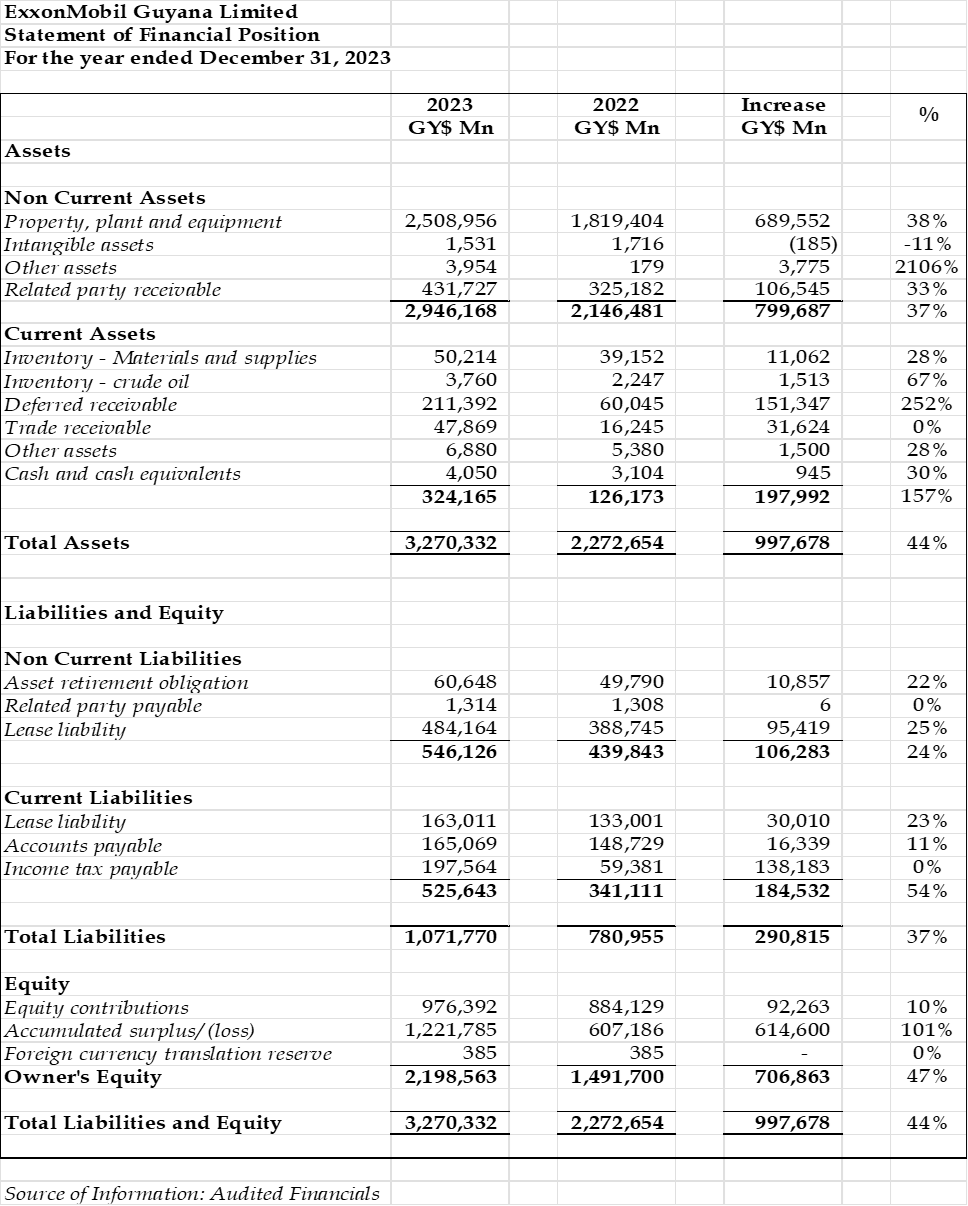

Turning to the Statement of Financial Position, total assets is made up mainly of Property, Plant and Equipment of $1,193,002 million, of which $1,176,600 million is invested in Development Assets, $204,022 million in Exploration and Evaluation Assets and $1,005 million is in Office Equipment and Others. Accumulated depreciation reduces the book value by $187,473 million, $771 million and $378 million, respectively. Accounts receivable reports a total of $9,161 million, an increase of $5,870 or 178%.

Current Liabilities mainly consist of Accounts payable and accrued liabilities of $64,596 million, an increase of $62,541million or 3043% over 2022.

Capital Expenditure in 2023 was $374,479 million, an increase of 42% over the amount expended in 2022. The provision for Decommissioning and restoration is shown at $118,773 million, an increase of $25,966 million which again is a strange item given that CNOOC self-describes as “non-operated joint venture partner”, since Guyana will have some legal barriers to holding a “non-operated joint venture partner” as a primary creditor for de-commissioning expenditure. As a practical matter, what if CNOOC pulls out of the venture before the end of the venture?

Unlike its two co-venturers, CNOOC maintains no inventory. It continues to sell its share of oil lifts to an affiliate in Singapore on a cargo-by-cargo basis. Despite this arrangement the company owes its related parties more than $258,000 million, the terms and conditions of which, including interest, are not stated. Unlike its co-venturers as well, the company’s financial statements do not disclose any royalty payment to the Government, which seems to violate the country’s Extractive Industry Transparency Initiative (EITI) obligations.

Conclusion

This columnist was able, by accident, to see the balance sheet of the company of which the Guyana operation is a branch. incredibly, that company has a share capital of US$200,000 or G$40,000,000. and for 2023 alone, it walks away with $355,694 million.

The column has stated in the past – that most ordinary companies in Guyana produce financial statements that are more informative and reader-friendly that CNOOC’s.

Next week’s column will feature a compilation of the financial statements of the three companies and compare these with the takings of the Government, AND THE REAL STORY BEHIND CNOOC’S PAYMENT TO EXXON.