Introduction

PLAINLY BUSINESS today looks at the recent reports published by the commercial banks under Supervision Guideline No. 10 – Public Disclosure of Information issued by the Bank of Guyana. Readers of the financial columns of the local media will recall that a predecessor Guideline which took effect on June 18, 2010 was revoked and replaced by a revised Guideline taking effect from the beginning of the second quarter of 2013. The new Guideline requires that quarterly calendar statements should be released within thirty days from the end of the quarter and forwarded to the Bank of Guyana. The Bank of Guyana resisted the protestations of the commercial banks that thirty days is too short a period to complete and publish reasonably accurate financial statements. Indeed, the fact that both Citizens’ Bank and Demerara Bank appear to have been unable to meet the deadline suggests that the concerns by the commercial banks may have had some merit. A consequence of this for purposes of this column is that a comparative analysis of all the commercial banks will have to wait on a later column.

Another issue on which the regulator and the regulated differed is the insistence by the Bank of Guyana that for each calendar quarter (March/June/September/December) the income statement should reflect the performance both for the quarter and cumulatively. This means that for the last quarter of any financial institution that entity will have to publish the Guideline 10 report within 30 days and then 110 days later it has to publish audited financial statements. For any institution whose year-end is not a calendar quarter – perhaps an October year-end – it will have to publish both September (calendar quarter) and October (year-end) financials. Since the average user of financial information may not be a seasoned specialist, such surfeit might cause confusion rather than provide meaningful information which is the objective of Guideline No 10.

In this first column to address the Guideline it seems useful to identify briefly the principles that have informed the publication. As the Bank of Guyana notes in introductory statements that would be appropriate in a more developed market, the Guideline is based on the premise that the reporting of comprehensive, meaningful and accurate qualitative and quantitative information in a timely manner provides strong market discipline on financial institutions to manage their activities and risk exposures prudently and consistently with their stated objectives.

The Guideline continues that the extent and level of disclosure is of fundamental importance to market participants in making accurate assessment of an institution’s financial position, financial performance, business activities, risk profile and risk management practices, corporate governance and accounting policies. Improved public disclosure also strengthens market participants’ ability to encourage safer and sound banking practices.

To avoid being too burdensome or over-prescriptive, the Guideline notes that the disclosure requirements it prescribes are not mandatory for every quarteror includes a generic format for the quarterly publication. Under the former exclusion, financial institutions need not disclose in their quarterly reports such matters as Formal disclosure policy, Performance against objectives, Revenue growth, Cost control, etc. The Guideline adds that where a financial institution does not prepare an annual report the disclosure requirements should be published on the institution’s website and transmitted along with the audited financial statements to the Bank of Guyana. Since the Companies Act requires all companies to issue an annual report, it is clear that the Bank of Guyana must be thinking of any matters not included in the annual report.

The Guideline does however require the publication of quarterly condensed – Statement of Financial Position, Statement of Cash Flows, Statement of Comprehensive Income, Statement of Changes in Equity, and selected explanatory notes.

Caveat: Because this is the first set of reporting under this new arrangement, comparable numbers are not available, the ratios are not perfect. For example, in measuring returns it is necessary to use, at a minimum, the loan balances at the beginning and end of the period to arrive at the average interest earned. The same applies to deposits and interest paid. As reports are published for later quarters, a more comprehensive and useful base will be available from which relevant ratios can be derived and analysed.

Additionally, the reader must bear in mind that by virtue of its small size in terms of assets, deposits or interest earned and interest paid, relatively modest changes in any of these variables in the Bank of Baroda can result in large percentage changes.

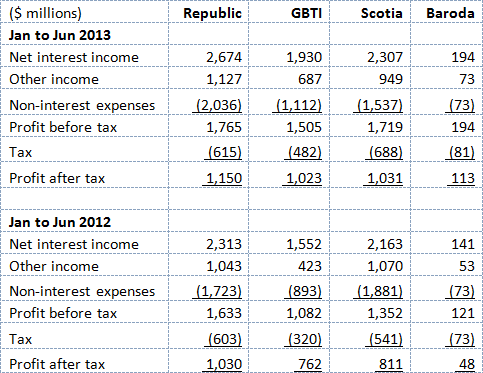

Statement of Income

Source: Published Quarterly reports

Significant income statement changes and ratios

Net interest income is the relationship between the interest income earned less interest paid out. The bank with the best growth in net interest income margin is the Bank of Baroda (37.6%) followed by GBTI (24.4%), Republic Bank (15.6%) and Scotia Bank 6.7%. Baroda reports growth in after-tax profits of 135.4% having increased from $48 million in half-year 2012 to $113 million for the same period in 2013. Increases in after-tax profits for the other banks were GBTI (34.3%), Scotia (27.1%) and Republic Bank (11.7%). The average tax rates paid by the banks were: Baroda (41.8%), Scotia (40%), Republic Bank (34.8%) and GBTI (32.0%).

One important line item is non-interest expenses which would include staff costs, other costs including administration, premises and equipment and loan loss provisions. None of the entities reported significant provisions or recoveries for the quarter and the period ending on June 30.

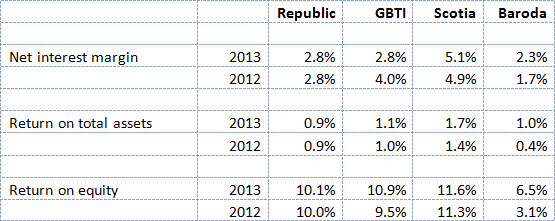

Source: Published Quarterly reports

Note that these are not annualised ratios and are based on the six months to June. The only significant change of note is in GBTI’s net interest margin which is the net interest income earned divided by the interest-earning assets. The movement may be due to the composition of the denominator which as noted earlier was not averaged out. Republic Bank is remarkably consistent for each of the three efficiency indicators while Baroda shows the most volatility. Measured by Return on Total Assets, Scotia reported the best performance while the big three report similar returns on equity. Let us not tell them the returns Sithe Global is demanding for their investment in the proposed Amaila Hydro-electricity project!

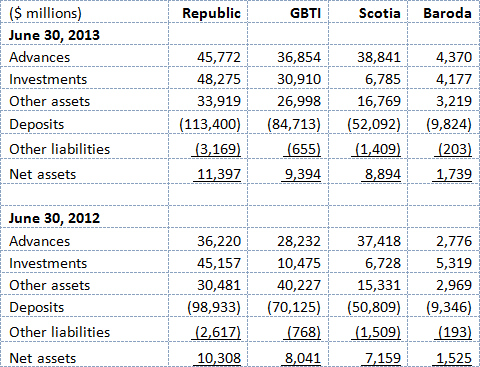

Balance Sheet

Source: Published Quarterly Reports

Republic Bank has the largest share of the market for deposits, accounting for 43.6% of the deposits reported by the four banks. Next come GBTI with a 32.4% share, with Scotia accounting for 20.1%. The picture in the share of the loans and advances by the reporting entities is more competitive. Scotia has only 20% of the deposits but has some 31% of the value of the loans while for Republic the share of loans is 36.3% and GBTI 29.3%. Measured by Loans and advances, Scotia is still some way behind Republic Bank but if the rate of growth in lendingby GBTI is maintained then it can leapfrog both Scotia in another year or two.

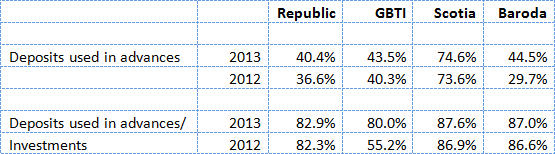

Here is how the four banks stack up with regard to growth in deposits and loans:

Source: Published Quarterly Reports

One strategy that works very much in favour of Scotia is the relationship between deposits and advances, currently the highest yielding asset of the commercial banks. In such a strategy the entity with the highest ratio of advances to deposits is likely to outperform those with lower ratios. For Scotia that ratio is 74.6% and while this could signal that the bank is maxing out, as a branch it may be able to call on its head office if attractive loan opportunities arise and there are no investment securities to be converted first to cash and then to loans. For RBL and GBTI Loans and Advances account for 40.4% and 43.5% of their deposits respectively, in both cases however some improvement over the preceding year.

Share performance

Finally, let us look at the share prices of Republic and GBTI, the only two of the four entities whose shares are traded on the local Stock Exchange. While the share price of GBTI has increased faster than Republic, the P/E ratio still favours Republic by a wide margin.

Source: GASCI.

Conclusion

The Bank of Guyana and the four entities must be commended for the effort to deliver financial information to the public in a timely manner. We do not know the extent of the co-operation among the Bank, the Securities Council and the Registrar of Companies. Bank of Guyana finds it easier to gain compliance from the financial institutions than the Securities Council receives from the public companies. It is probably close to ten years since the Securities Council issued a Draft Code of Corporate Governance which the public companies can confidently assume they can ignore. It would be so good for the development of the market in securities to have a better relationship with the regulator. Hopefully, that time will come soon.