Introduction

Following questions raised by the parliamentary opposition, the Minister of Finance earlier this month presented to the National Assembly what purported to be annual reports of the Financial Intelligence Unit headed by Mr. Paul Geer, Director. Such reports are required under the Anti-Money Laundering and the Combatting of Financing of Terrorism Act 2009 (AMLCFTA). The Act was passed on April 30 2009 but not assented to until August 14 of that year, close to three months beyond the twenty-one days allowed by the Constitution.

Let us look briefly at the requirements of the Act in respect of annual reports and accompanying audited financial statements. Section 9 requires the Director “to keep proper accounts and other records.” Sections 9 and 110 set out the timeline for preparing auditing, and tabling in the National Assembly the financial statements and report of the Financial Intelligence Unit (FIU) as follows:

| Deadline | Action required |

| By March 31 | Prepare the statement of accounts for the preceding year |

| None specified | Submit to Auditor General for audit |

| No later than June 30 | Director to submit to the Minister of Finance a report comprising information on the financial affairs, operations and performance of the Financial Intelligence Unit, including the amounts paid into the Consolidated Fund under the Act, along with the audited annual statements of accounts. |

| No later than one month following receipt | Minister of Finance to lay the documents in the National Assembly. |

No report, late reports and misleading reports

No later than July 31, the report and audited financial statements of the FIU should be laid in the National Assembly. Well, without any information or explanation no report was submitted for the part year of 2009 or for 2010 for which the National Assembly voted tens of millions of dollars. Under normal circumstances that would be considered unacceptable but then nothing about the FIU is normal. As we shall see, the FIU has failed to carry out its functions and duties, a combination of inadequate resources, incompetence, lack of effort and inadequate political supervision and direction. Only the most starry-eyed optimist would believe that it is capable of carrying out the rather extensive menu of powers and functions under the Act.

The reports for 2011 and 2012, submitted on November 7, 2013, are accompanied not by financial statements in the sense that accountants would understand those to be but by a one page Statement of Receipts and Expenditure. The reports of the Auditor General for the years 2011 and 2012 assert that the statements are prepared “in accordance with Generally Accepted Accounting Principles”, a rather meaningless term, and “in accordance with International Financial Reporting Standards (IFRS)”, respectively. As every accounting student knows, financial statements under IFRS comprise a statement of financial position (balance sheet), a statement of comprehensive income, a statement of changes in equity, a statement of cash flows, and accounting policies and explanatory notes. IFRS-compliant financial statements also include comparative figures for the preceding reporting period.

The legal status of the FIU is not particularly clear. It is described in the AMLCFTA as an agency and not a corporate body. Consequently, it is incapable of owning assets or incurring liabilities in its own name. It is therefore understandable that it cannot have a balance sheet and some of the other statements identified in the preceding paragraph. But not to have explanatory notes is simply mindboggling and starkly exposes the catastrophic cost and consequences of having an Auditor General responsible for the public accounts of the country who has no professional qualification and who does not understand the nature of IFRS’s or his own audit opinion. He is allowed to get away with this abomination because, except for the Finance Minister, there is no professional accountant in the National Assembly or in the Clerk’s Office to reject some of the absurdities that are submitted to the Assembly in the name of financial statements or annual reports.

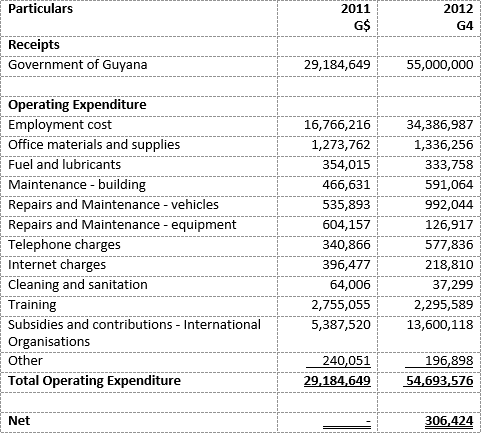

For what it is worth here is a summary prepared by me of the two Receipts and Payments Statements laid in the National Assembly.

Statement of Receipts and Expenditures

Source: Financial Intelligence Unit Annual Report

The item Government of Guyana receipts represent the amount voted by the National Assembly under the line item Subsidies and Contributions to Local Organisations. The two principal items of expenditure for both years were Employment Cost which accounted for 57% and 62% in 2011 and 2012 respectively, and Contributions to International Organisations accounting for 19% and 25% respectively for those years. Apart from the director, the FIU had only an Admin Assistant in 2010 and added a Financial Analyst, a database administrator and a Legal Advisor in 2011. It added another Financial Analyst in 2012. Interestingly, the half-baked Receipts and Payments Statements for 2011 and 2012 are signed off not by the Director and someone described as Accountant and not Financial Analyst. The Act required that the FIU be staffed by an attorney-at-law and an accountant appointed by the Minister and personnel trained in financial investigation or other employees as the Director considers necessary. In other words, the Director could choose between trained personnel or any other person!

Interestingly, there is no item accommodation and travelling despite the extensive travelling done by FIU Director who would qualify as a bronze medalist in the distinguished Government Frequent Flier Club.

It is clear that the statutory and professional obligations of the Director of FIU, the Minister of Finance and the Auditor General have not been met in relation to the preparation, audit and tabling of audited financial statements. That appears to have escaped their attention, unless they hoped that no one would notice.

In part two, I look at some of the requirements of the Act and the level of reporting of suspicious transactions.