Introduction

Section 25 of the Guyana Forestry Commission Act 2007 requires the Commission to submit, no later than six months after the end of the year, a report to the subject Minister (currently of Natural Resources and the Environment) containing an account of its activities in such details as the Minister directs together with a copy of its audited accounts for the year. The Minister is then required to lay these in the National Assembly as soon as possible but not later than eight months after the end of the financial year.

The pre-2007 law did not impose any time within which these two reports were to be tabled in the National Assembly. But surely no matter how grievous the failure to prescribe a date is, it could hardly have been expected that the annual report for 2005 would be tabled until eight years later. But that is just what happened when on November 7, 2013 Mr. Robert Persaud tabled the report and some accounts of the GFC for the eight years 2005-2012 inclusively.

But the late tabling is hardly the only problem in relation to the reports for 2005-2012 to which I will return shortly. The other is that no one seems concerned that there appears to be a black hole when it comes to reports prior to 2005. The official records of documents laid in the National Assembly for the eighteen years from 1996 to 2013 reveal that the first year for which any report or audited financial statements were laid in the National Assembly was in 2013!

What exactly have successive Ministers of Agriculture, including Mr. Robert Persaud, been doing that prevented them from tabling any reports for perhaps as long as two decades? The same question must be asked of the Public Accounts Committee which is responsible for the oversight of not only the government accounts but also “such other accounts laid before the Assembly as the Assembly may refer …”; and of the National Assembly and the shadow minister; and of the Parliamentary Sectoral Committee on Natural Resources chaired by the shadow minister; and of the clearly compromised Audit Office.

Statutory outline

The whose principal responsibility is the development and growth of forestry in Guyana on a sustainable basis functions under the Guyana Forestry Commission Act, 2007, a successor to an Act by the same name passed in 1979. The Act allows for a Board consisting of a Chairman, the Commissioner of Forests and as many as twelve other persons all of whom are appointed by the designated Minister for the Commission. The persons so appointed must have relevant knowledge and experience in defined areas.

The names of persons so appointed must be gazetted. My search of the Gazette for at least one year did not turn up any such notifications. One must wonder then whether the 2012 Chairperson Mr. Clinton Williams, a leading PSC operative, and others like Ms. Geeta Singh who is no longer on the Board, were ever properly appointed.

Constitutionally, responsibility for the audit falls on the Auditor General although the 2007 Act itself grants the Commission the right to appoint the auditor. As is the case with those entities which no auditor would give a passing grade, as NICIL, NCN and the Cheddi Jagan International Airport Corporation, the Auditor General Mr. Deodat Sharma chooses not to contract out the audit of the GFC but does it himself. This practice leads to the reasonable inference that the Audit Office is complicit in the illegalities and corruption taking place in Guyana to the extent that it fails to pursue and report on such matters.

Statutory failure

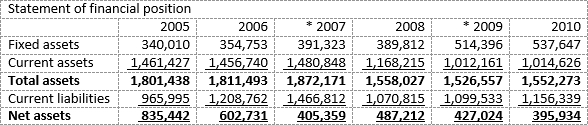

Now let us turn to the reports for the years 2005-2012. The first point to note is that the Minister has failed to table audited financial statements for the years 2010 – 2012. The 2010 report has a balance sheet for which not a single note is indicated, an income statement indicating notes 5, 6 and 7 but none of which is presented and a cash flow statement in draft without comparative figures. No audit report is presented.

For 2011 there are no audited financial statements or audit opinion. There is a Summary Revenue and Expenditure Account which is misleadingly referred to as DRAFT FINANCIAL STATEMENT. The 2012 Annual Report includes at page 9 what is described as Draft Financial Statement: Guyana Forestry Commission with an asterisk and a note “Awaiting Audited Financial Statement from Audit Office of Guyana.”

It should be noted too that all of the financial statements are incomplete, including those on which the Auditor General has issued an opinion: they do not include even the limited notes to the financial statements. I am not sure that Mr. Deodat Sharma, who is unqualified for the post of Auditor General, is aware that no proper auditor would allow his opinion to be published with accounts that are abridged by the client. But then he also fails to indicate whether the financial statements have been prepared in conformity with the Guyana Forestry Commission Act, a basic requirement in any audit opinion.

The financial statements

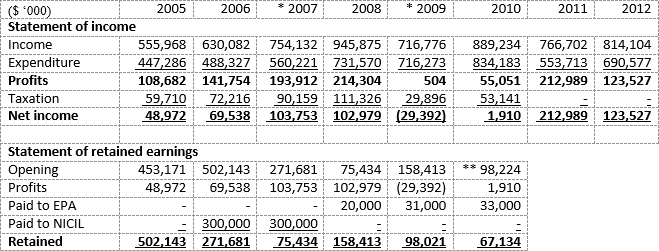

Let us look now at the Income Statement shown below and in a graph. In the interest of space, I have aggregated some of the insignificant line items in the Income Statement. Of course, because there are no audited statements for 2010-2012 these have to be dealt with cautiously in any analytical exercise.

* shown at restated amounts as per subsequent financial statements

** unexplained difference between 2009 closing and 2010 opening balances

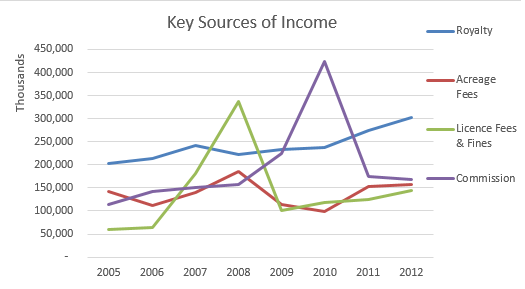

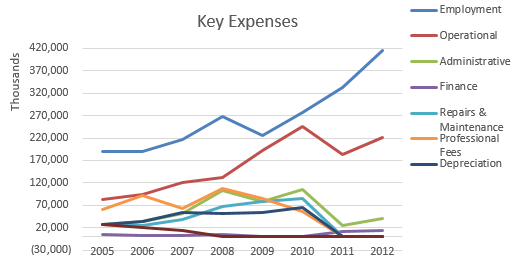

The following points stand out:

1. Except for Royalty, there are huge fluctuations in income over the years which are not explained in the narrative annual reports. Surely citizens, if not the unalert parliamentarians, would like to know why License Fees and Fines moved from $181 million in 2007 to $336 million in 2008 only to fall back to $102 million in 2009.

2. Similar variations in the expenses are also evident as is the case in operational expenses between 2009 and 2011, and Administrative Expenses which doubled between 2007 and 2008, fell 23% in 2009 and then witnessed a 32% increase the next year.

3. In the six years between 2005 and 2010 the GFC paid out nearly half a billion in professional fees! The persons to whom these payments were made should be identified and the purpose of the payments should be explained.

4. The GFC, recognising that it is not tax-exempt provides for tax charges in its financial statements for each of the years 2005 – 2010. Indeed it discloses that it owes $1,126 million in taxes but has made no effort to pay any of its tax liabilities to the Guyana Revenue Authority.

5. It is not as if the GFC cannot afford to pay the taxes it owes: it has around $1,000 million in the bank.

* shown at restated amounts as per subsequent financial statements

6. An even more objectionable and most offensive line item in the Income Statement are two payments to NICIL of $300 million in each of 2006 and 2007. These payments are unconstitutional and unlawful yet the Auditor General gave a clean audit opinion for these years! The qualified accountants in the Audit Office should hang their heads in shame to be associated with such blatant abuse of accounting and violation of the laws.

Paying NICIL

One expects Finance Ministers to be zealously vigilant and robustly protective of moneys payable into the country’s Consolidated Fund. Instead we have NICIL, under the successive chairmanship of two Finance Ministers, being used to siphon off hundreds of millions of dollars due to the Consolidated Fund. There can be no extenuating circumstances that could excuse let alone justify such unlawful and reckless conduct, fully aware of the nescient state of the Auditor Office.

As if the above are not bad enough, the Auditor General signs off on financial statements approved not by the Board which has the statutory duty for the financial statements but by Mr. James Singh, the Commissioner. For the $600 million alone that they have allowed to be paid over to NICIL all the GFC directors should be hauled before the courts while NICIL should be investigated and disbanded. The combination of NICIL/GFC is not only an insult to the intelligence of Guyanese but a challenge and an affront to our decency. Surely even the most docile Guyanese must have some breaking point at which they say enough is more than enough.

Conclusion

GFC is just another example of the perpetuation of Jagdeo’s legacy of financial lawlessness, a state that is as wide as it is deep. A state that allows incomplete and deceptive reports to be tabled and accepted by the National Assembly without any questions being asked or challenges raised. One in which the national accounting body the Institute of Chartered Accountants of Guyana remains silent even as basic rules of accounting are violated with impunity. One in which the parliamentary bodies are paralysed by their own mediocrity. One in which we even have a mini-parallel Consolidated Fund called NICIL and where the evidence of slush funds everywhere mounts.

The Government will not allow it and the weak opposition will not even ask for it but only a wide-ranging, independent investigation into the public financial management of this country generally and of NICIL specifically can stem the relentless decline in accounting and accountability. The people of Guyana must demand it.