Introduction

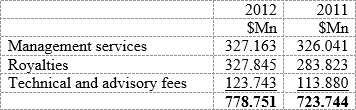

I closed last week by introducing a table which set out the transactions between Demtoco and other companies in the group. Of particular interest were the following charges:

These charges are not only unusual for an entity that buys a branded product and does nothing else but sell that product to a single customer; they are also unlikely. The charges have two financial and fiscal effects. First, they transfer income from Demtoco to its group companies not in the form of dividends available to all shareholders. Second, to the extent that they are charged against income for purposes of the computation of taxes, they reduce the company’s taxable profits, and hence the tax payable by the company.

Favouring the mother country

This is not to suggest that the payments are free of all taxes. They would be subject to withholding taxes, a form of income tax paid to non-residents on distributions and on certain specified charges. The benefit of having a payment subject to withholding taxes rather than corporation tax is that the rate(s) of withholding taxes are lower than the rates of corporation tax.

business page Guyana’s Corporation Tax rate is 40% for commercial companies and 30% for other companies except for telephone companies which pay what seems to be a penal rate of 45%. Compare this with withholding tax, the standard rate of which is 20%, but subject to reduction under any applicable Double Taxation Treaty. For example, the rate of withholding tax payable on royalties, technical fees and dividends under the Guyana-UK Double Taxation Treaty is 10%. Under the Caricom Treaty the rate of withholding tax on royalties and technical fees is 15% while dividends are subject to a zero per cent rate of withholding tax.

There is another point worth noting: there is a limit of 1% of sales on what is allowed as a deductible for group expenses. In tax parlance the excess is added back to the accounting profit for the purpose of calculating corporation tax.

The tax note in the financial statements for the year 2012 shows an amount of $75.205 M added back for the purpose of calculating corporation tax. The total turnover of the company for 2012 was $6,769 M of which 1% is $67.690 M. It is clear that the company has taken the full benefit of all but $75.205 M of the $778.751 M it paid to its related parties for various services. At best, this seems extremely aggressive if not unreasonable and unjustified.

But then the group no doubt can call on expertise which cannot be matched by the Guyana Revenue Authority. Its auditors, PricewaterhouseCoopers (PwC) in their 2011 publication unabashedly titled International Transfer Pricing boast of having a network of transfer pricing specialists with extensive experience of dealing with revenue authorities around the world. The local company’s auditors are Jack A Alli, Sons and Company, up to recently a correspondent firm of PwC and highly regarded for its tax expertise. Indeed, its Managing Partner was selected by President Ramotar as a member of the elite group to review Guyana’s tax laws.

Traditional arrogance

Since the company closed its operations and became no more than a shell company in Guyana I have had my own suspicions grounded in my familiarity with tax cases where slick transfer pricing arrangements are prevalent to move profits from one country to another. So I wrote the company’s Managing Director a letter asking for five bits of information to inform this week’s column. I wrote both as a shareholder and a columnist and asked for:

– The name of the supplying related party and whether the price charged for products from the entity is the same across the Caricom states;

– The bases and principles underlying the charges for Management Services, Royalties and Technical and Advisory Services and the names of the related parties providing the services or charging the royalties;

– The principal functions and activities of Demtoco;

– The percentage of products distributed through Edward B Beharry & Company; and

– Whether the company has any current estimate of the market for cigarettes served by smuggled products.

The Managing Director not only failed to provide the information but did not even think that my letter was worthy of an acknowledgment! Alas, it is not the first time that this company has demonstrated bad manners, arrogance, contempt for shareholders and disrespect for the media. But it is likely to be much more than this. The company’s London Head Office might have reckoned that providing the information would be too revealing, damaging even. The possibility is that it simply could not justify the $778 million which the group imposes on its subsidiary Demtoco, a prime candidate for examination under section 74 of the Income Tax Act.

Anti-avoidance legislation

Section 74 is a general anti-avoidance provision which permits the GRA to ignore or modify, as appropriate, any artificial or fictitious transaction designed or executed wholly or substantially for the purposes of avoidance of tax by legal means; for example by relying upon loopholes in, or advantageous interpretations of, the law.

Despite its emotive and negative connotation, there is nothing illegal per se about transfer pricing if it is done as part of proper tax planning. But where highly questionable transactions are entered into under the guise of genuine business relations there is a line that needs to be drawn, one that borders on tax evasion. The Financial Times of the UK, the home of Demtoco’s parent, recently carried an article that referred to multinationals ranging from General Electric in the US, Amazon in France and Starbucks in the UK being attacked for tax avoidance. The authors of the article accused multinationals of enjoying a free ride on tax-funded benefits – roads, educated workforces, reliable courts – provided by the countries where they do business, while their employees and the taxpayers of the host countries paid for those benefits.

It is often forgotten that in addition to allowing the GRA to set aside artificial or fictitious transactions under section 74, the tax laws, in spite of their general increasingly obvious antiquity, do contain two clear anti-transfer pricing rules. The first deals with the export of produce and allows the GRA to replace the value at which the export is booked by the taxable entity in Guyana with a deemed value. The second, quite modern, is akin to the unitary rule which provides for a minimum tax rate equivalent to the effective rate of tax paid by the group.

I am not aware of whether and the extent to which the GRA has ever applied any of the three sections despite their obvious applicability to those companies engaged in forest products, bauxite, gold, rice and of course Demtoco. As we argue about whether or not the country can afford to reduce the rate of VAT we should think of the taxes we lose on artificial transactions and fictitious transactions including management charges for services that are never really provided, or are sometimes charged more than once. One thing accountants have in common with New Thriving – we can cook.

Money or life?

Readers will recall that last week I referred to the harm which cigarettes and other tobacco products do to smokers and non-smokers alike. I recall attending a workshop some time ago to discuss a draft bill on tobacco control legislation. That legislation would have advanced Guyana’s compliance with the Framework Convention on Tobacco Control (FCTC) which we signed on to in 2006. Four years ago Health Minister Dr Leslie Ramsammy lamented the fact that he required standards were not yet in place and promised that the “fight for tobacco control will be more robust in 2010.”

Well except for the fact that Dr Ramsammy is no longer the Health Minister the situation with regard to tobacco control is the same. What is then the problem? Apart from the usual bureaucratic hurdles and snafus, there is more than a hint of tension and conflict between money into the Consolidated Fund and the health of the nation. That is a false choice. Tobacco is supposed to garner for the treasury what is considered to be lots of revenue to the country. Excise tax on tobacco products in 2013 is projected at $1.421 billion with VAT bringing in at least another $1.4 billion. If we assume generously that tax revenues from cigarettes derived from taxes other than excise taxes and VAT, such as corporation and withholding taxes and income taxes by shopkeepers, etc, are equal to the VAT and Excise Tax, the sector is projected to contribute $5.7 billion or 4% of total revenues per annum.

But that would be as much one-sided economics as it is one-sided accounting. We must look at the cost side of the coin. Estimates of the economic cost of tobacco range widely depending on whether the country is a producing country, which Guyana is not, and the prevalence of smoking in the population. In the absence of relevant statistics we have to rely entirely on the sales revenue of the monopoly supplier and taxes collected by the state. In both cases it appears that the quantity of cigarettes consumed in Guyana is increasing and therefore that either existing smokers are indulging themselves more or that more persons are taking up the habit.

Even in tobacco producing countries, the cost is estimated to outweigh the benefits although by how much is a matter for pure speculation. It is estimated that the economic, health and social costs of tobacco to a country range between 1% and 2% of GDP per annum. Even if in the case of Guyana it is one quarter of one per cent, it means that tobacco costs Guyana in excess of $6 billion per annum.

There is therefore a clear case for a substantial increase in the taxes on tobacco and strong measures to discourage smoking. The annual mantra of no new taxes, so far as alcohol and tobacco are concerned, is dangerous for the nation’s health.

Conclusion

This column has gone beyond the normal financial analysis of an annual report into what Judge Gladys Kessler, a US judge described as an “industry…that survives, and profits, from selling a highly addictive product which causes diseases that lead to a staggering number of deaths per year, an immeasurable amount of human suffering and economic loss, and a profound burden on our national health care system.”

Will we permit a similar situation continue in Guyana or will we now take serious action, including legislation to deal with the deathly consequences of tobacco and the practices of greed, manipulation, improprieties and illegalities so embedded in the tobacco industry?

Next week we turn to the other side of the coin and look at the annual report of Demerara Distillers Limited which holds its Annual General Meeting on April 22.