Introduction

To avoid getting caught up in a backlog of annual reports, Business Page today reviews the annual reports of three of Guyana’s public companies – Sterling Products Limited which held its annual general meeting on April 19, Caribbean Container Incorporated (CCI) which held its annual general meeting on April 30 and Guyana Stockfeeds Limited whose AGM is scheduled for May 23. It is perhaps co-incidental that these companies have some striking similarities: they are all public companies but with a dominant shareholder, and none is among the big league of Guyana’s public companies. Indeed CCI accounts for 1.02% of the market capitalisation of the top ten public companies, Stockfeeds 1.07% and Sterling Products 1.12%. Cumulatively the three companies account for less than 3.25% of the market capitalisation of the top ten companies.

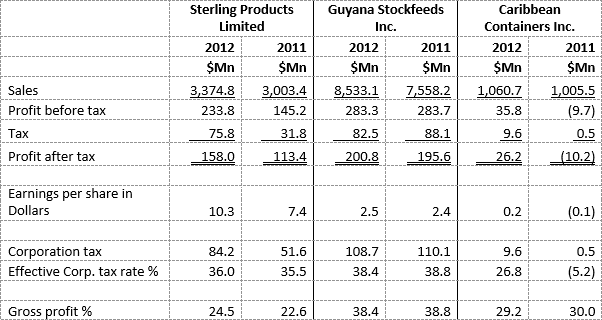

In their annual reports, each of the three companies reported better results in 2012 than in 2011, a trend among all public companies. Stockfeeds reported an increase in year-on-year profit after tax of 3.2% while Sterling declared an increase in after tax profit of 39.3%. CCI appears to have transformed a loss into a profit but this is almost entirely attributable to a reduction in book entry depreciation because of a change in the estimated useful life of assets.

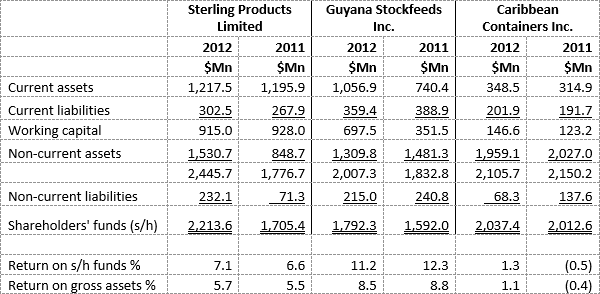

I have prepared summaries of the Income Statements and Balance Sheets of the three companies extracted from their audited financial statements. The income statements of Sterling and CCI present figures on cost of sales and gross profits which are helpful in financial statement analysis. This does not mean that across companies ratios like gross profit percentages are necessarily comparable, since different companies may allocate and treat expenses differently. We need look no further than the gross profit percentages of these two companies to show how these can be affected by different accounting treatment of particular line items. CCI does not include depreciation charges on plant and machinery to arrive at gross profit but Sterling Product does. As a result of the difference in treatment, CCI’s gross profit percentage of 29% is appreciably higher than Sterling’s.

Similarly, return on shareholders’ funds, a key performance measure, is not comparable across companies and industries since some companies periodically revalue their assets and correctly, treat the surplus as shareholders’ funds while others keep their assets at historical cost, as they are also allowed to do under accounting rules. The impact is fairly obvious in the case of Sterling Products Limited which, had it not revalued its fixed assets by hundreds of millions of dollars, would have had a return on shareholders’ funds of close to 9% instead of 7.1%.

The juxtaposition of the balance sheets and income statements is merely for purposes of convenience and is not intended as a comparison of the strength or performance of the companies. Having said that, it is clear that CCI has produced the weakest results in 2012, despite having at its disposal the highest value of fixed assets. What this means is that those assets are producing less in revenues than either Sterling or Stockfeeds.

Balance Sheets

Source: Audited financial statements

Income Statements

Source: Audited financial statements

Sterling Products Limited

Sales have increased by 12.4% while profit after tax increased by 44.6% on a gross margin of 24.5%. Chairman Dr Leslie Chin reported export sales of $210.4 million or 6.2%, a growth of 11% but from a very small base. Profit after taxes increased from $113.4 million to $158.0 million, a 39% increase over 2011, and reflecting a 7.1% return on shareholders’ funds.

This company has been a steady rather than an outstanding performer. Its results are reflected in the market price for the shares which increased year-on-year by 33.3%, no doubt encouraged by the company’s progressively increasing dividends. The payout ratio in 2012 measured by after-tax profits is 33.8% while as a percentage of profits available for distribution, dividends for the year amount to 13.9%. The effective rate of Corporation Tax payable by the company is 36.02% compared with a nominal rate of 30%.

The Balance Sheet has been strengthened by a revaluation of the company’s fixed assets amounting to $564.2 million. The new property tax values which become effective from this year will cause the company’s property tax liability to double in 2013.

Guyana Stockfeeds Inc

An increase in sales of 13.3% did not translate into income and profits as margins were squeezed with raw materials and consumables accounting for 91% of revenue, up from an already challenging 90%. The company continues to incur high professional fees of $71 million compared with $64.9 million in 2011. The notes to the financial statements indicate that Guyana Stockfeeds Limited, a wholly-owned company incorporated under the laws of Trinidad and Tobago undertook transactions amounting to $771 million on behalf of the Guyana company and also received $30 million as “Reimbursement of cost incurred”. It is unclear and perhaps unlikely that this sum is part of the $71 million in professional fees.

Despite only a modest increase in the value of net assets, property tax rose from $11 million to $15.2 million, the reason for which is not immediately apparent.

As a result of a challenge in the High Court of Guyana by the government company National Industrial and Commercial Investment Limited (NICIL), a shareholder of the company, the company is not permitted to issue any new shares until the outcome of this matter is fully settled. The regulator, GASCI has suspended trading of the company’s shares until the matter is settled. Apart from this issue the company is a defendant in two matters being addressed by the court but in both cases the company’s attorneys have assured it that the company has a good defence.

The shares in Guyana Stockfeeds Inc are owned 85.87% by Mr Robert Badal, Chairman and CEO of the company. I have heard complaints from shareholders that Mr Badal treats the company like a personal property and even is inaccessible to them. Perhaps Mr Badal prefers to have sole and exclusive control of the company. While that would be regrettable in the wider scheme of the participation of members of the public in the ownership of so-called public companies, it may not be a bad idea for some arrangement to be worked out with the minority shareholders.

CCI

The company has seen a turnaround in profits, recording a profit after tax of $26.2 million after a loss of $10.2 million in 2011. While Chairman Ron Webster has emphasised the company’s return to profitability, it is important to bear in mind that the turnaround of $36.4 million is due almost entirely to a reduction in depreciation charge of $35.8 million and not to better operating performance.

Sales during the year increased by 10.6% with cost of sales (before depreciation) accounting for 70.8% in 2012 compared with 70.0% in 2011. Export volumes increased by 10% over 2011 but from the Chairman’s report it seems that the margins are minimal, partly, according to him, because of the siltation of the Guyana port limiting tonnages. Approximately 29.0% of the company’s revenue in 2012 was derived from sales to Caricom countries, up from 28.4% in 2011. Maybe while the private sector continues its lobbying for the dredging of the port, the company may consider utilising smaller, regional vessels.

The company’s working capital has increased from $123.2 million to $146.6 million or 1.64:1 to 1.72:1. While inventory has increased from $164.6 million to $209.7 million, provision for obsolescence has remained unchanged at $29.1 million. As a result of losses from prior years, the effective rate of corporation tax payable by the company is 9.6%.

The return on shareholders’ funds in 2012 is 1.3%, from negative 5.1% in 2011 while the return on assets was 1.1% in 2012 compared with negative 0.4% in 2011.

Strange things happen

During the year the majority shareholder caused to be placed on the agenda of a shareholders’ meeting a motion for a bonus issue of one share for every fifty shares held. Yet after the passage of the resolution, the majority shareholder declined its allocation of the bonus shares. Even if we ignore the question whether a bonus share issue can be treated as a rights issue to be accepted or rejected, one has to wonder whether the company is simply playing games with the 10% minority shareholders hoping that they would think they received any benefit from the bonus issue.

That is not the only problem that bothers me. Mr Webster in the very second paragraph of his Report expressed pleasure that the market capitalisation of the company increased by 108% during the year. But how did this happen? Well, in the last two weeks of 2012, 1,000 shares were traded at $10 each, immediately increasing the market value of the company’s shares from $5.50 to $10 and its market capitalisation from $830,041,273 to $1,509,165,950. Now, which Stock Market would have the absurd situation where a trading in 1,000 of 150,916,595 shares representing 0.0004% of total shares can lead to an increase of 81.81% in the company’s market capitalisation? What is troubling is that Mr Webster did not question this absurdity but saw it “as a clear demonstration of investor confidence in the company and its management.”

This raises another more serious question. And this is how the shareholding of this company ended up in companies owned and controlled by Mr Ron Webster, a longstanding director of CCI. The common law and the Companies Act have strict rules and sanctions regulating gains from one’s office as a director.

This company is headed by the Chairman of the Private Sector Commission and it would be inappropriate and dangerous for market confidence if a company headed by such a prominent person does not seek to clear its name in the most open and transparent manner. The Securities Council must move quickly to have this addressed under section 506 of the Companies Act.